It is a known fact that Central Banks around the world are shading and twisting their economic data. The main reason being to hid from us the truth about the health of our economy. If you can remember during May 2010, Minister Idris Jala announced that Malaysia is going to be bankrupt by 2019, if nothing is being done. He blamed it on the subsidy system and recommends that the government should remove the subsidies gradually. Subsidy is a very sensitive economic tool and has been in used for more than a century especially in the agriculture sector in Western Economies. Farmers are subsidized so that their produce remained competitive in world markets and at the same time also helped to provide employment back home. The effectiveness of subsidies can be viewed from different angles, some argued that it leads to an inefficient allocation of resources while others viewed it as essential in providing some protection to certain sectors of the economy so that it will ensure the constant supply of strategic resources like food and also provides full employment.

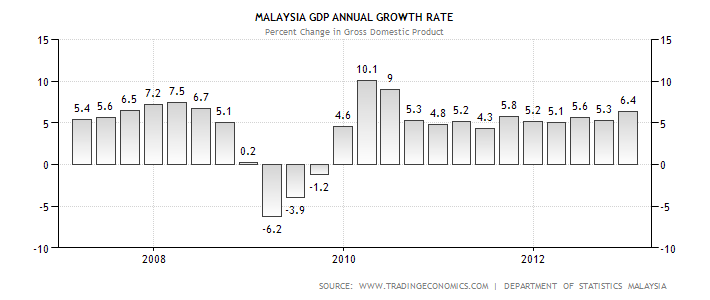

The question is whether our removal of the subsidies done at the right time? Remember during that time our economy was just recovering from the 2008 Global Financial Crisis which affected much of the population. Would it be the right decision for policy makers to curtail the spending of the public when it was during the very crucial time where curtailing or restricting consumer spending is the last thing the economy needs. The following chart shows the Malaysian GDP annual growth rate as of 2007.

Notice that during the second quarter of 2010 the GDP growth rate was at 9% which can be considered very high and in fact is the second highest quarter since 2000 after the 10.1% achieved earlier. With such a good performance why not the government just let the economy to continue with this growth story by not interfering? You have to understand that in order to sustain such a high growth rate, Government expenditure will also need to be increased. Where will the extra funds be coming from? How can Idris Jala announced (May 2010) that our country is going bankrupt at the very moment when our economy was recovering with such spectacular growth rate. Isn’t it strange or do they have other hidden agendas behind all these?

Let take a look at our Government Debt to GDP ratio in the following chart. Did you notice that our Government Debt/GDP suddenly surged from 42.8% in 2009 to 55.4% in 2010? This represents an increase of 29.4% YOY increase in our government debt. One explanation for his will be the massive borrowing by our government to finance its increased expenditure on both the fiscal and monetary policies. Or what is also known as the stimulus package to fence off a recession.

How does our Government finances its expenditure?

For any recovery to be sustainable, initially the government will have to lead the way by increasing its own spending in the fiscal and monetary framework. Once this gets underway and with the improved expectations of better days ahead then the next wave is to encourage the private sector which consists of the business and consumers to spend more so as to increase the level of economic activity. Before we go further let us take a look at the pattern of our Government spending for the past 6 years in the following chart.

As you can see from the above our Government spending has always been on the uptrend even before the Global Financial Crisis in 2008. It peaked during the last quarter in 2012 which is recorded at 32624 MYR millions. So how do our Government finance its expenditure?

In normal market conditions any Government will finance its expenditure either through increase borrowing or taxes. Increasing taxes at this moment of time will be politically suicidal for our government due to the coming General Elections as nobody likes to pay more taxes. If it proceeds then it will certainly be the last nail in the coffin for the government.

The other alternative is to increase borrowing which is also going to be suicidal because in the Constitution the ‘ceiling’ for our Government Debt/GDP is stated at 55%. As you can see during the year of 2010 it is has already breached the 55% threshold although by only 0.4%. In other words the Government cannot afford to borrow more from external sources as this will surely bring the ratio above the 55% mark very soon. So where can it get more funds to finance its ever increasing expenditure without increasing taxes and borrowings? The answer is by reducing the subsidies.

Why reduce subsidies?

During his speech in May 2010, Idris Jala threatened that without any reduction in the subsidies our Government will surely go bankrupt by 2019. The question : Is there any difference between Idris Jala and Henry Paulson (U.S Secretary of Treasury) when he pushed through legislation authorizing the Treasury to approve the US$700 billion TARP to bail out the financial system? According to him without the approval it will not only undermine the U.S financial system but the whole world as a result of the domino effect. The answer is NO bloody difference. They are both using scare tactics so that the public will be bowed to their demands.

Our Government controlled parrots (mainstream media) claimed that by reducing subsidies it will helped unlock inefficient resources so that it can be used for other purposes such as building infrastructures, schools, public transport and so on which in the end will benefit the public. During any economic recovery the last thing any Government need to do is to dampen consumer spending.

Why subsidy reduction will not affect Government Debts?

When a Government overshoots its expenditure it needs to borrow or increase taxes in order to finance this activity. As we already stated increasing taxes is not a popular option and most Government will try to avoid. This leaves us with borrowing as the other option. Again when we borrow from foreign creditors then our Government Debt to GDP will increase and since our level is capped at 55%, there is not much option right? The last alternative will be to source from domestic. Again sourcing funds from the domestic sector will further increase the debt burden. So the last solution is by soaking up money from the public. The question is how the authorities going to do it?

According to the French Economist Jean Baptiste Say (1767-1832) who said that the spending for production simultaneously generates income for the people to buy all the goods produced. In the end the buying power will help clear the inventory and hence provide full employment. In short it means that the demand for goods will be equal to the supply of goods. But our problem is how do we quantify the demand and supply in the equation. Fortunately the solution to this problem can be found in Dr Irving Fisher’s equation of exchange. In Dr Fisher’s equation the demand is represented by MV and the supply is PT which is equal to GNP. GNP (Gross National Product) is the dollar value of all the goods and services currently produced in the economy. Or it can be express in the following algebraic equation.

MV = PT = GNP where,

M = Money Supply

V = Velocity of Money

P = Average price of current production

T = Total volume of current production

Through the Keynesian model we also know that,

GNP = C + I + G where,

C = Private consumption

I = Investment

G = Government spending

So how do we connect all this mumbo jumbo? To illustrate we use an example where the total GNP for country A is $100 million and the breakdown of the GNP is as below.

Consumption

|

50

|

Investment

|

20

|

Government

|

30

|

Total RM

|

100

|

However Government spending can be further breakdown into education, defence, subsidy and etc. So by diverting resources from subsidy to other sectors such as defence or infrastructure there will be no change in the final amount which is $30 million. The only change is the composition of the spending and in this case a reduction in subsidy and an increase in defence and infrastructure expenditure.

So what we can deduce from here is that whenever the Government borrows or divert resources from other sources where the source of money is already in existence it will not add to existing money supply. This is what economists called non-monetized borrowing or non-monetized deficit financing. This is mainly paper shuffling and hence will not affect the Government Debt level.

Our next question is what will be the immediate effect of a subsidy reduction?

Will the reduction in subsidies cause price inflation?

The amount of subsidy is expected to drop to RM37.61 billion in 2013 from RM42.4 billion in 2012 which represents about 4% of GDP. As you know the bulk of the subsidy went to fuel which accounted for about RM25 billion or 23% of the total. So what will happen to the price of fuel when the Government reduces its fuel subsidy over the next few years? Needless to say it will go up and as we know fuel is used in almost all industries from transport to the manufacturing of plastic materials. With its ‘trickle down’ effect needless to say it will push up the prices of most products or what is called a ‘cost push inflation’. In layman terms this is called price inflation. The following chart shows the CPI (Consumer Price Index) which tracks the prices of certain essential goods paid by consumers.

As you can see from above as of January 2013 our Malaysian CPI increased to 106.20 index points from 99.3 index points in 2010. The level recorded in 2010 is actually the mean for the last 5 years. So as you can see after the implementation of the subsidy reduction the prices of our goods really went up. So, in the end who will end up paying the cost for the price inflation? It will be ordinary folks that is most affected and where did the excess money gained from reduced subsidy went to? Public projects such related to ETP such as the MRT, new Highways, oil and gas and etc, soaked up all of that. And who are the people that got the contracts? Not me and you for sure. So what are we witnessing is actually a redistribution of income from the poor to the rich. If left uncheck the income gap between the poor and rich will be wider.