No thanks to the usual rhetoric by our authorities in assuring us that our economy is resilient thus able to shield ourselves from the ongoing global economic crisis. Unfortunately most Malaysians tend to believe this and hence “things are in safe hands”. When our government started to rationalize the subsidy of fuel and other essential goods, things started to fall apart. Since then our economy’s health started to deteriorate and people realizing that our economy is not performing as expected. The worst thing is they could no longer able to maintain their current lifestyle as salaries are not keeping up with the ever increasing inflation rate.

Realising the mistakes in their policy implementation our Government started to appeased the people by ditching out cash to the less fortunate. Hence, a social aid scheme known as BR1M was born. However, such Band-Aid measure will not get us anywhere because it is only a short term solution and will not be sustainable in the long run. What needed are policies that will create jobs and increase productivity which eventually leads to sustainable higher salary for the people.

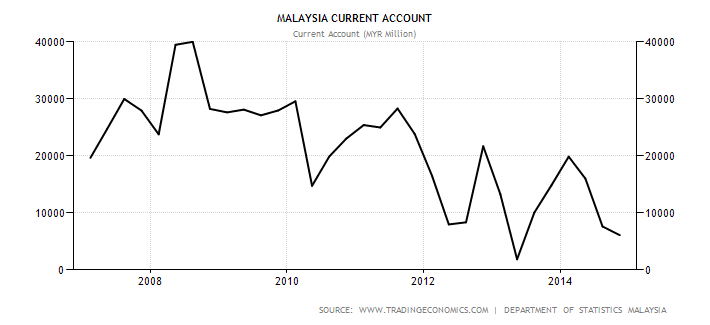

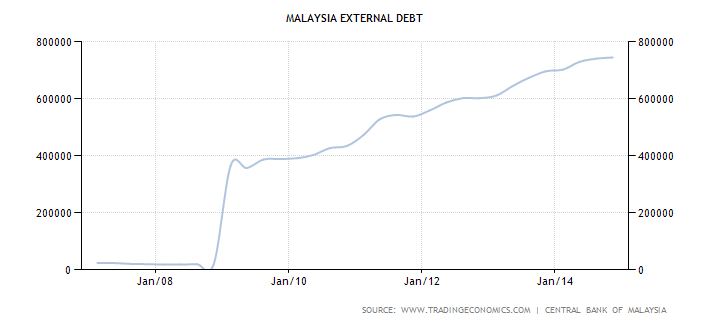

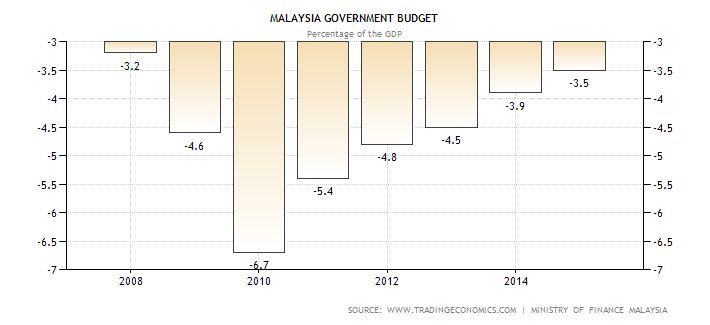

At the meantime our economy is bleeding red ink. Our GDP growth stalled at around 5% since 2010 when it reached its peak of 10.3%. Moreover since 2010, our other economic fundamentals have also started to deteriorate. Our Current Account balance is declining due to our declining exports. To pump-prime our economy out of the recession during the Great Recession in 2008, both the private and public sector are encouraged to spend. This has resulted in the swelling of our external debt from about RM 400 billion in 2009 to RM 744 billion in 2014. Spending more than the revenue it received from taxes, our Government resorted to running budget deficits. The series of event can be summarized in the following charts.

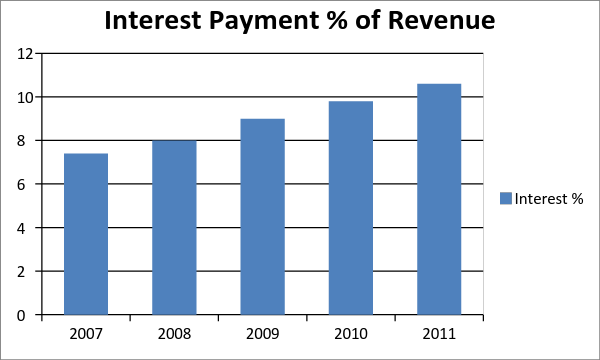

Faced with economic uncertainty and lavish spending habits, Fitch Ratings Agency started to caution our government to find a cure for our imbalances or risk a sovereign downgrade. When a nation is downgraded its cost of borrowing will increase as the perceive risk of lending has increased and lenders wants a higher compensation.

This is last thing our government wants as an increase in interest rate means more resources will be committed to interest payment on its debt. The following chart shows the interest payment as a percentage of revenue collected by our government. It has been on the uptrend since 2007.

Hence, on order to address this imbalance our Government started its austerity drive. Then in 2010, Minister Idris Jala, announced that without addressing our debt problem, Malaysia will then be bankrupt by 2019. Everybody was taken by surprise. As a result measures were taken which includes rationalizing of subsidies for certain essential goods such as sugar and fuel. When we are still in a state of shock our government swiftly implemented those austerity measures. Thus with this ‘shock and awe’ tactic, ordinary Malaysians which does not even have the time to react succumbed to it.

The ‘shock and awe’ tactic also known as the shock doctrine was first developed by an economist by the name of Milton Friedman from the University of Chicago. Milton Friedman believes in using bitter medicine and painful shocks inflicted upon the masses so that they can be controlled psychologically. The basis of their techniques can be found in Friedman’s book Capitalism and Freedom and it has since been adopted by the IMF’s bitter medicine for their austerity measures. The very same template of policy is applied to all recipient countries of IMF bailout.

Unfortunately these measures did not produce the results as anticipated. Our Debts seems to be increasing because our Government’s lavish spending habits. To finance further expenditure our Government will either need to borrow more, grow our economy out of its problems or increase taxes. Given that it is unable to borrow more due to the constraint in capping the debt to GDP at 55% and knowing there is no way to grow the economy without spending more, it is left with one choice, increasing taxes. But our income tax has reached its limits due to narrow tax base so the only solution left is to increase the tax base where more people will be ‘inflicted the pain’. Thus GST has to be introduced because of the following reasons.

- It helps to widen the tax base that will include virtually every Malaysian instead of relying on the traditional income and corporate taxes.

- Government Deficits has to be finance from a source that will not contribute to the existing debt level.

By introducing GST, our Government hope it will help reduce the debt and also its budget deficit. At the same time it can avoid another Sovereign rating downgrade. Voila !! killing three birds with one stone it seems. All problems solved with a stroke of the pen? But wait a minute, I wonder whether have they evaluated the side effects of this policy?

In implementing any economic policy there is always a cause and an effect. So when our Government implements a policy that improves the finances of the public sector then obviously other sectors of the economy will be affected. If our public sector’s (Government) finance improves then there will be repercussions on the other two sectors of the economy namely the private and external sector. They think that by improving one sector then the rest of the economy will follow suit. In actual fact this is not going to happen and I will be explaining it in the following.

To bring this analysis into another level let me introduce you an economic model known as ‘Sectoral Balances’ analysis. With this model I hope demonstrate to you why our Government’s attempt to slashed budget deficit will work against its wish to cure our economy.

Sectoral Balances Approach

Sectoral Balances is a framework for macroeconomic analysis of the economy developed by British economist, Wynne Godley. The basis of the Sectoral Balance model lie in the analysis of fund flows between the three sectors of the economy namely the public, private and foreign sector. The relationship between them can be derived from the balance of payment and national income accounting.

National Income or GDP or Y = C + I + G + (X – M)

Where

C = Consumption

I = Investment

G = Government Spending

X = Exports

M = Imports

Savings can be described as the amount left after income minus consumption and tax. Thus,

Savings or S = Y – C – T

Substituting Y from above,

S = C + I + G + (X - M) – C – T

Netting off the C and rearrange we get,

(S - I) = (G – T) + (X – M) or,

Private Sector = Public Sector (Budget Deficit) + Foreign Sector

Thus, by definition from the Sectoral Balances analysis our economy consists of three sectors which are the Private Sector, Public Sector (Budget Deficit) and the Foreign Sector. The sum of all three sectors whether they are in deficits or surpluses will theoretically equal to zero. But normally it doesn’t due to leakages. So, when our Government runs a Budget Deficit it is obvious the other two sectors cannot be running deficits also. One or both of them should be running surpluses.

Currently, our Government is running a Budget Deficit while both the Private and Foreign Sectors are running surpluses. Since our Government has rationalizing subsidies and implementing GST the net effect will be a reduction in its Budget Deficit? What are the net effects of such policy?

Effects of Reducing Budget Deficit

From above we know that when a Government is running Budget Deficit either one or both of the other two sectors will be in surplus. Malaysia is committed to reducing its budget deficit as per recommended by Fitch. What is going to happen soon will be an increase in government revenue through GST and hence will improve the public sector (G – T). As the public sector improves we know that either the private or foreign sector or both will worsen. This following table is a compilation of data that I gather from several sources.

Year

|

(G - T)/GDP %

|

(X - M)/GDP %

|

S/GDP %

|

I/GDP %

|

(S-I)/GDP %

|

2004

|

-4.1

|

12.1

|

35.1

|

23.1

|

12

|

2005

|

-3.6

|

14.1

|

36.8

|

22.3

|

14.5

|

2006

|

-3.3

|

16.1

|

38.8

|

22.7

|

16.1

|

2007

|

-3.2

|

15.3

|

38.8

|

23.4

|

15.4

|

2008

|

-4.6

|

17.1

|

38.5

|

21.4

|

17.1

|

2009

|

-6.7

|

15.5

|

33.3

|

17.8

|

15.5

|

2010

|

-5.4

|

10.9

|

34.2

|

23.2

|

11

|

2011

|

-4.8

|

11.5

|

34.8

|

23.2

|

11.6

|

2012

|

-4.5

|

5.7

|

31.7

|

25.9

|

5.8

|

2013

|

-3.9

|

3.9

|

30.1

|

26.1

|

4

|

2014

|

-3.5

|

4.3

|

31.1

|

26.7

|

4.4

|

Source : BNM, Department of Statistics and World Bank

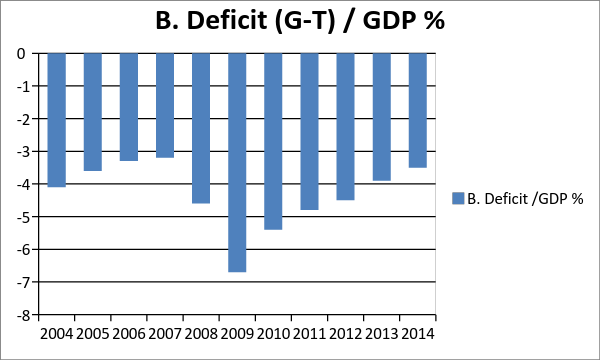

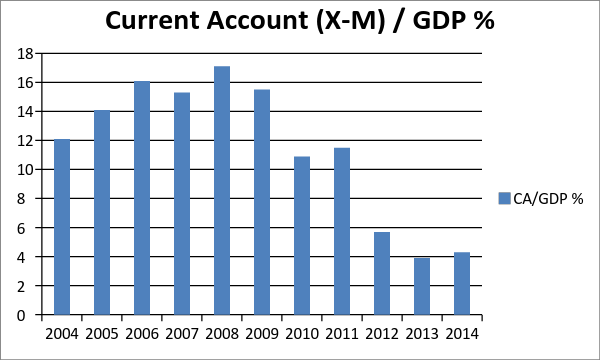

The above table shows the performance of the three sectors from 2004 to 2014. With this data and for easier visualization, I plotted the three sectors into different charts as shown below.

Source : BNM, Department of Statistics and World Bank

From above we know that our Budget deficit currently runs at -3.5% to GDP while both the private and foreign sector are at a surplus of about 4% to GDP. As can be seen from above when our Government increased its budget deficit from 4.1% in 2004 to 6.7% in 2009, both the private sector (S - I) and foreign sector (X - M) improves. When happens when our Government starts reducing its budget deficit in 2010? Both the private and foreign sector started to deteriorate from about 15% to 4% to GDP currently. So what is going to happen when our government starts Balancing its Budget or (G – T = 0)?

Yes, from the sectoral balances approach we know either one or both of the private and foreign sectors will be affected. Our current model that is relying on the private sector (S – I) to boost the economy has stopped working. This is because although investment may be increasing savings rate is not catching up either due to the following

- Depletion of their savings in financing the consumption either local or imported products

- Increase in quit rent, assessment, taxes esp. GST

- Inflation or rising price level due to subsidy rationalization

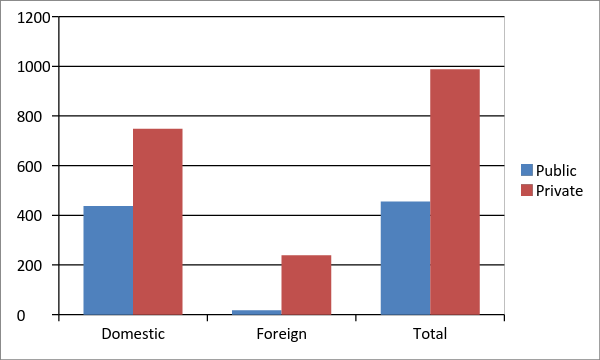

As a result in order to maintain their current standard of living, households will have to deplete their savings or borrow more which lead to further indebtedness. This is the reason why our private sector’s debt has ballooned to about RM 980 billion in 2012 as shown by the following chart.

Source : BNM, Department of Statistics and World Bank

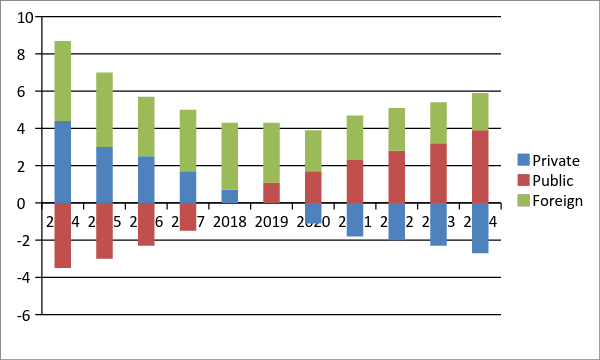

In short our past policy depending on the private sector for growth has come to an end and it is time for the public sector to take over the job. In order to achieve a more stable and sustainable model of economic growth instead of trying to balance the budget we should expand the public sector in the form of higher fiscal spending. Policies implemented to expand the public sector must ensure that there will be spill over effects into the private and foreign sector so that they will continue to be in surpluses. Graphically our current state of the economy can best be illustrated with the following graph.

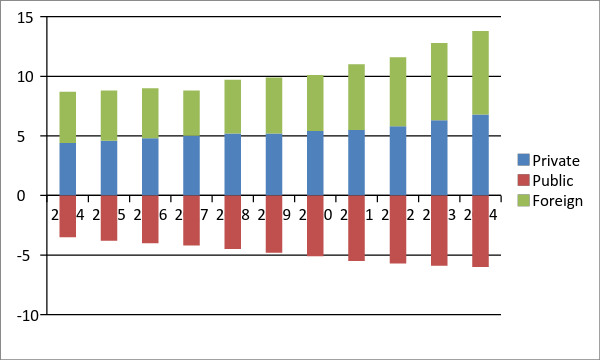

When Government Balances Budget (G – T = 0)

The above chart best describes our economy in the next few years if our Government continues its current policy on reducing the budget deficit. The red colour bar represents the public sector, green for foreign sector and blue for the private sector. As can be seen when our government balances its budget from this year onwards the red bar moves from negative to positive zone and will soon become the dominant sector. The foreign sector will remain in positive territory because our exports have become competitive due to the sluggish Ringgit. Thus it can be seen that the private sector (S – I) will be the worst hit due to the depletion in savings and the increase in investment to cater for the export industry. Therefor I expect the private sector to feel more desperate, pain and frustrated due to increasing debts and stagnating salaries.

What if our Government increases the budget deficit?

It will be another story, when our government increases the budget deficit then the other two sectors will benefit. To increase the budget deficit or (G – T) our Government either have to increase its fiscal spending G or reduce its taxes which will boost the income of the people. Thus it will help increase savings and spending which will eventually boost the economy. The scenario is best described by the chart below.

When Government increase Budget Deficits (G – T > 0)

But some people argued that high budget deficit is not sustainable to our economy. This is not necessary so as I shall demonstrate in the following table.

Government Budget with GDP Growth and Debt/GDP %

Country

|

Govt. Budget %

|

GDP Growth %

|

Debt/GDP %

|

Venezuela

|

-11.5

|

-2.3

|

49.8

|

Egypt

|

-9.1

|

4.3

|

97.1

|

Pakistan

|

-8

|

4.14

|

63.3

|

Japan

|

-7.6

|

-0.8

|

227.2

|

Spain

|

-5.8

|

2.6

|

97.7

|

U.K

|

-5.7

|

2.4

|

89.4

|

India

|

-4.5

|

7.5

|

67.7

|

Portugal

|

-4.5

|

0.7

|

130.2

|

France

|

-4

|

0.24

|

95

|

Mexico

|

-4

|

2.6

|

36.9

|

South A.

|

-3.8

|

1.3

|

46.1

|

Malaysia

|

-3.5

|

5.8

|

54.8

|

Greece

|

-3.5

|

1.2

|

177.1

|

Poland

|

-3.2

|

3.3

|

50.1

|

The chart above shows the 15 countries that are running the highest budget deficit in the world. As can be seen out of the 15 biggest spenders 13 countries still manage to record positive GDP growth. Look at India it is running a deficit of 4.5% and yet its economy grew by 7.5%. And so does Pakistan, 8% budget deficit but 4.14% economic growth? How about their Debt/GDP? Only three out of the 15 countries record triple digit Debt/GDP figures. So what say those folks who have preaching running huge deficits is bad for the country.

Summary

In summary, I like to congratulate our Government on their implementation of austerity measures in order to strengthen the public sector. But I also wish to caution that such measure will eventually backfire as our private sector is most indebted in recent time and thus most vulnerable. This is because when our Government engage in fiscal contraction it will further reduce demand which will reduce output and eventually employment. This tends to weaken the private sector and that leaves the foreign sector to inspire demand. The problem is we cannot rely on our exports to pull us out of the slump in demand. The reasons are as follows.

At the moment everybody is trying to export the way out of trouble by weakening their currencies. At the moment there is a fierce currency war going on out there. Every exporting nation is trying to devalue their currency to cheapen their exports. Since one country’s export is another country’s imports, how are we going to export our way out of trouble.

So our current approach to grow our economy through fiscal austerity will not work because it will weaken the private sector further as there will be further built up of private debts. As mentioned above our household debts is already reaching close to 90% of GDP and any further accumulation of debts will make debt servicing almost impossible. This will end up in a massive repayment defaults What follows are further credit crunch as banks will be more selective in their lending and will lead to stock market, real estate and mortgage crashes.

The right policy is to find a cure for this sector and not weaken it. Our Government will have to continue its deficit expenditure so as to create demand which will add to income and hence savings. When revenue increases so will income and corporate taxes and this process will feed on itself and in time will help turn around the economy. In short, I will confidently say that if Malaysia going to be hit by another Financial Crisis it will erupt from the private sector.

The author is the Economic Advisor to the National Union of Bank Employees