The Asian Financial Crisis in 1997 came as a surprise and caught most people off guard not only by the speed but also the severity of the crisis. At that time the Asian Economic Miracle was the buzzword. The Asian Tiger economies are at their peak not only in the performance of their export oriented economies but also their stocks and properties market. To counter the shortage of funds needed to boost their economies, they embark on a ‘loose money’ monetary policies regime.

Loose Money Policy

To expand credit, rules governing the inflow and outflow of foreign funds are relaxed and so does the terms of borrowing by banks and corporations. Instead of the traditional ‘borrow long lend short’, banks did the opposite where they ‘borrow short lend long’. Such practice will put bank in an awkward position because if they borrow short say 3 years and lend long for 10 years then there will exist a ‘window of interest rate risk of 7 years’, from fourth year to the 10th year. Banks is in a risky position because during a financial crisis, a country’s currency is most vulnerable to currency speculators and hence its interest rates.

Currency devaluation

Traditionally there are two tools available for authorities to fend off currency speculators. One is to use Monetary Policy tool to raise the domestic interest rates and the other is the Exchange Rate Policy of Open Market Operations to defend the exchange rate by selling its foreign reserves (in US$) to artificially prop up the local currencies. However such policy will always fail due to the size of the foreign exchange market that is just too big for any government to manipulate. The foreign exchange market currently trades more than US$ 5 trillion a day. Hence intervening in the foreign exchange market will only buy more time for the authorities and not solving the problem.

If authorities choose to raise interest rates then it will increase the ‘cost of funds’ for the banks and corporations. As a result, it will be very prohibitive for them not only to do business but also to service their debts. If left unchecked, it will send many of them into financial difficulties.

During the height of the Financial Crisis in 1998, the interest rates in Malaysia went up to as high as 18%. Coupled with the currency devaluation (USD/MYR 1 to 4.80) it provided a double whammy to many individuals and businesses in Malaysia. Doing business in Malaysia then was very difficult then due to the volatility of the Ringgit and many businesses lost money due to the fluctuation of the Ringgit and hence misquoted their customers. As for the individuals they suddenly found that their mortgage repayments have doubled due to the interest rate hike.

Below is a write-up on the Asian Financial Crisis in 1997 and also the various solutions implemented by our Government. It also highlights some of the similarities between then and the current Global Financial Crisis. Again this is a long article (28 pages) and I hope that by the time you finish this article you will learn the following.

- What is a Financial Crisis and how it started?

- How it affects laymen like us?

- How Governments attempt to solve it?

- How to spot a crisis?

- Why current efforts will not provide a solution?

- How Quantitative Easing works?

- What is Fractional Reserve Banking?

- How to cripple our Banking System?

Initiation of the Crisis.

Below, I present to you below a table that chronicles of events leading up to the crisis.

Column1

|

The 1997 Asian Financial Crisis

|

Date

|

Chronicle of Events during the Asian Financial Crisis

|

2nd July 1997

|

After exhausted of funds defending the Baht. Thailand decides to float it

|

18th July

|

Philippine and Indonesia devalues their currencies

|

18th July

|

IMF extends $1.1 billion loan to Philippines

|

24th July

|

Asian currencies under severe pressure especially the rupiah

|

20th August

|

IMF extends $17 billion loan to Thailand

|

28th August

|

Asian Stock Markets plunging to multi year lows

|

23rd October

|

Hong Kong dollar and stocks under heavy selling pressure. Hang Seng lost 10%

|

28th October

|

Currency Speculators moving to Korea. Korean won hits new low

|

5th November

|

Indonesia seeks IMF assistance with $40 billion approved

|

24th November

|

Collapse of Sanyo and Yamaici Securities and Hokkaido Takushoku Bank

|

3th December

|

Korea seeks IMF assistance. A total of $57 billion approved

|

5th December

|

Malaysia imposes tough market reforms in order to stem foreign funds outflow

|

There are many factors caused the Asian Financial Crisis of 1997-98. Listed below are some of the most debated reasons for the onset of the Asian Financial Crisis.

- Deteriorating economic conditions

- Moral Hazards by banks and corporations

- Too much inflow of foreign funds

- Stock market and Real Estate Bubble

- Lack of regulatory control on funds

- Massive disinvestment by the Japanese during the early 1990s due to their misadventure in the U.S coupled with their stock market crash. This resulted in the recalling of funds in the region by Japanese banks.

In the following, I shall provide an account on the few most likely factors that caused the 1997 crisis.

- Liberalization of the Financial Sector

The credit boom in the international market coupled with the relaxation on foreign capital inflows by authorities has led to an increase in the foreign capital inflow. Normally the FDIs will find its way into either the real economy in terms of loans to businesses or the unproductive stock and property market. However during that time the FDIs are going into the stock and property market. The following table shows the percentages of the loans given to the property sector and also the NPL during 1997.

Bank Lending to Property Sector as % in 1997. Source BIS

|

Column1

|

Column2

|

Country

|

% of loan to property

|

NPL - Non Performing Loan

|

Hong Kong

|

40-55

|

1%

|

Singapore

|

30-40

|

4%

|

Thailand

|

30-40

|

36%

|

Malaysia

|

30-40

|

15%

|

Indonesia

|

25-30

|

15%

|

South Korea

|

15-26

|

30%

|

Philippines

|

15-20

|

7%

|

Source : Bank of International Settlement

As can be seen from the above the four countries (Thailand, Malaysia, Indonesia and South Korea) that are most affected by the crisis, coincidently also with having the highest NPLs in their respected banking sector.

The following chart is the effect of the Financial Crisis on the respective GDP growth of those countries.

Asian GDP growth

| ||||

from 1996-97 (%),IMF

| ||||

Country

|

1996

|

May-97

|

May-98

|

Change

|

Indonesia

|

9

|

7.4

|

-5.3

|

-12.4

|

Thailand

|

5.5

|

7

|

-3.1

|

-10.1

|

South Korea

|

7.1

|

6.3

|

-0.8

|

-7.1

|

Malaysia

|

8.6

|

7.9

|

2.5

|

-5.4

|

Philippines

|

5.7

|

6.4

|

2.5

|

-3.9

|

Singapore

|

6.9

|

6.1

|

3.5

|

-2.6

|

Hong Kong

|

4.9

|

5

|

3

|

-2

|

China

|

9.7

|

8.8

|

7

|

-1.8

|

Source : International Monetary Fund (IMF)

As indicated from the above table, the GDP growth rates that dropped the most between 1997 to 1998, are from the four most affected countries. First we have Indonesia -12% (from 7.1% to – 5.3%), Thailand -10.1% (from 7% to -3.1%), South Korea -7.1% (from 6.3% to -0.8%) and Malaysia -5.4% (from 7.9% to 2.5%). Hence the number one causality is that over-liberalize economies tend to have deeper repercussions from capital flight.

- Fiscal Imbalances

Fiscal imbalance refers to the difference between the negative balance of payment and the ability of a country to pay its debts.

Column1

|

Column2

|

Column3

|

Column4

|

Column5

|

Column6

|

Country

|

Current A/C

|

Balance

|

Exports

|

Annual (%)

| |

1995

|

1996

|

1995

|

1996

| ||

Thailand

|

-7.9

|

-7.9

|

23.1

|

0.5

| |

Indonesia

|

-3.3

|

-3.3

|

13.4

|

9.7

| |

Malaysia

|

-10

|

-4.9

|

20.3

|

6.5

| |

Philippines

|

-4.4

|

-4.7

|

28.7

|

18.7

| |

Singapore

|

16.8

|

15.7

|

13.7

|

5.3

| |

South Korea

|

-2

|

-4.9

|

30.3

|

3.7

|

Source : IMF

The above table shows the relationship between the deterioration of the Exports and Current accounts. The Current account can be defined as follows,

Current Account = (X-Y) + NY + NCT

Where X = exports, Y = imports, NY = net investment income from abroad and NCT = net cash transfer. Since the X and Y constitute the largest component in the equation, they are the most important components in determining the Current Account situation. If Y>X then a country is said to be in Current Account deficit and vice versa.

While the current account deficit remains high but at the same time these countries are experiencing a big downturn in their export receipts. For example in 1996, South Korea and Thailand experienced a sharp fall in their exports, dropping from 30.3% and 23.1% to 3.7 and 0.5% respectively from a year earlier. Hence this represents what is called a fiscal imbalance where countries experiencing reducing exports with current account deficits. With such a big drop in exports, eventually is receipts will not be enough to pay for its current account deficits.

During periods of boom in exports there is a need for funds to finance its exports industry and other increase economic activity. At that time the liberalization of the Global Financial market provided a perfect avenue to source for external funds. However, eventually such borrowing will widen the current account deficits.

When a country’s current account deficits widened coupled with the drop in exports and an overvaluation of the currency due to the inflow of foreign funds, it will attract the attention of currency speculators. Currency speculators will eventually short the domestic currency and will cause the currency to depreciate.

Eventually there will be a ‘reverse flow of funds’ from an inflow to outflow of foreign funds. This outflow of funds will result in a ‘credit crunch’ and coupled with the high interest rate will eventually bring down the real estate and banking sector.

The relationship between the balance of payment crisis and the banking crisis is much more evident nowadays due to the globalization of the financial industry. The following table shows the frequency of the crisis between banking and balance of payments.

Column1

|

Column2

|

Column3

|

Column4

|

Column5

|

Frequency of Crisis

| ||||

Types of Crisis

|

1970-79

|

Avg/year

|

1980-95

|

Avg/year

|

Balance of payments

|

26

|

2.6

|

50

|

3.13

|

Banking

|

3

|

0.3

|

23

|

1.44

|

As can be seen from the above table, before the year 1980, the occurrence of crisis is more biased towards the Balance of Payments. Out of the total of 29 Crisis only 3 are banking crisis. However since the 1980s the total banking crisis rose to 23 out of 73. So we can deduce that somehow the modern day financial crisis may be caused by the relationship of both balance of payments and banking.

In other words a Banking crisis may predate a Balance of payment crisis and vice versa.

- Deterioration of Bank Balance Sheets

Since the factors affecting the Crisis are inter-related and when currency speculators found there is a weak link between the various components of the economy like an over-valued currency, persistent high negative balance of payments and falling exports then there will be an opportunity to make big money by betting on a depreciation of the currency.

During the 1990s era most of the Central Banks in ASEAN pegged their currencies against the dollar. The short term benefits of such a move are creating a stable environment for the inflow of foreign investments and also less headaches on daily fluctuation of exchange rates. The disadvantage is that Central Banks will have to maintain the peg even at the expense of over-valuing their currencies.

Again when currency speculators found that central banks are maintaining an over-valued currency then they will likely be subjected to a speculative attack. Soon they will flood the market with massive sales of the currency and this will create a condition where supply outstrips demand and finally lead to the collapse of the currency.

To counter this move, the Central Bank will first try selling the Dollar to purchase the local currency. However due to the massive sales of the local currencies by the speculators, central banks will soon use up the holdings of their foreign reserves. Once their foreign reserve is exhausted then the local currency will be devalued.

Another avenue is to raise the domestic interest rates. By increasing the interest rates it not only helped to prevent further capital outflow but also encourage capital inflow. However such a move will have an effect on the bank’s balance sheet because of the higher cost of funds to obtain funds. If left unchecked it will eventually lead to the collapse of the weakened banking sector. If they don’t increase the interest rates then they will not be able to maintain the currency peg which will eventually collapse. In other words the Government and Central Banks are in between a rock and a hard place.

So how do Central Banks counter such a situation?

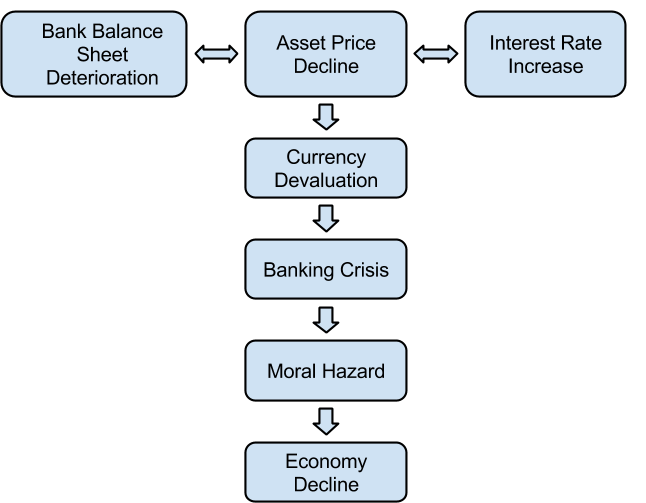

Before we proceed further, let me present below a flowchart that will illustrate the dynamics of the Asian Financial Crisis.

Vicious Cycle of a Financial Crisis

Why no alarm Bells before the crisis?

What surprises everybody is that there are no warning signs on the impending crisis because economic indicators show no signs of rapid deterioration. The only signs are falling stocks and property prices. In January 1996, Thailand’s stock market felled 40% as with Korea’s bourse which also felled sharply at the end of 1996. Malaysia’s stock market also dived during the early 1997. I present to you below the timeline of events occur in Malaysia’s during the 1997 Financial Crisis.

Column1

|

Timeline of Malaysia's response to the 1997 Financial Crisis

|

Date

|

Chronicle of Events during the Asian Financial Crisis

|

2nd July 1997

|

After exhausted of funds defending the Baht. Thailand decides to float it

|

10th July

|

Bank Negara Malaysia intervene in the Forex market to defend the Ringgit

|

13th August

|

Mahathir attack rouge speculators and point finger at Soros

|

27th August

|

Malaysia designate the 100 Index linked counters and banned Short Selling

|

4th Sept

|

Malaysian Ringgit continue to plunge

|

20th Sept

|

Mahathir called for currency trading immoral and be banned in HK

|

21st Sept 1997

|

Soros calling Mahathir 'a menace to his country'

|

2nd Oct 1997

|

Meeting in Argentina. Mahathir and Nor Yaakop finalising the Capital Control

|

5th Dec 1997

|

Malaysia impose tough market measures by Anwar Ibrahim

|

7th Jan 1998

|

NEAC was formed

|

16th Feb 1998

|

BNM reduce SRR from 13.5% to 10% in banks. Boosting liquidity in banks.

|

20th May 1998

|

Asian currencies continue to plunge

|

20th June 1998

|

Formation of Danaharta as an asset management company to handle NPLs

|

10th August 1998

|

Danamodal was formed to recapitalise the Banking Sector

|

16th August 1998

|

KLCI plunge to the lowest at 260 points

|

1st Sept 1998

|

Imposition of Capital Control

|

In view of the deterioration of Malaysia’s internal and external sectors, time is of essence. To tackle the problem Malaysia established the NEAC (National Economic Action Council) in 7th January 1998, which was based on ideas and policies of NOC (national Operation Council). NOC was formed as a result of the 1969 racial riots. The NOC was given executive power so it can override all the red tapes and jurisdiction of different ministries to ensure the smooth implementation of policies.

The main objectives of the NEAC are as follow:

- Restoring both public and investor confidence.

- Make sure it will be a soft landing for the economy.

- Reposition and revive the economy to enhance competitiveness and also its attractiveness to foreign investors again.

- Strengthen the economic fundamentals to ensure vision 2020 will be achieved.

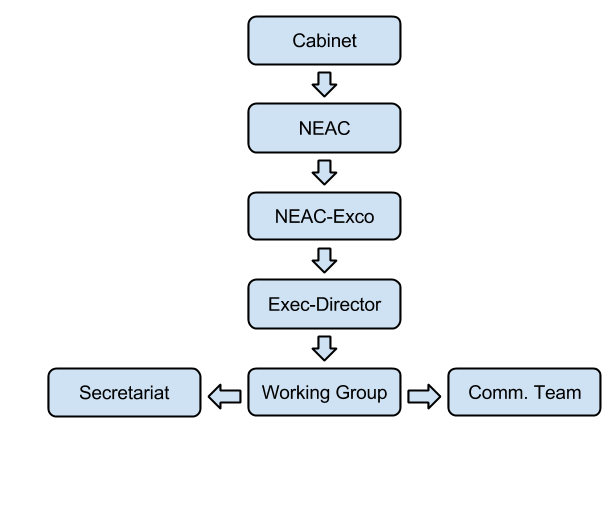

Below, I present to you the flowchart of the NEAC Committee.

The NEAC consist of 26 members with the Prime Minister (Dr Mahathir) and Deputy Prime Minister (Anwar Ibrahim) as the Chairman and Deputy Chairman respectively. While the remaining consists of representatives from various Ministries , Governor of Bank Negara Malaysia, EPU, NEAC EXCO, Executive Director, Secretariat, Working Group and the NEAC Communications Team. The NEAC EXCO was chaired by the Prime Minister while the Executive Director was chaired by ex-Finance Minister Tun Daim Zainuddin. The Secretariat was staff by EPU officials and the Working Group members consist of Tan Sri Wan Azmi (Land and General), Datuk Dr Zainal Aznam Yusof (ISIS), Tan Sri Thong Yaw Hong (Public Bank Chairman) and Professor Mahani Zainal. From the above timeline it is clear that even after a series of measures adopted, the Ringgit and stock market is still plunging. Hence as a result, desperate situations needed desperate measures and capital control follows next.

It seems that the idea of capital control was originated during Mahathir’s trip to Argentina. The Chief architect of Malaysia’s capital control was Nor Yakcop. Formerly he was running the foreign exchange trading desk in Bank Negara and the same bloke that caused Bank Negara Malaysia to lose about RM 30 billion about 20 years ago. Later he became the Finance Minister of Malaysia. Other members of the group that caused the forex scandal includes ex-Prime Minister Dr Mahathir, ex-Finance Minister Daim Zainuddin and ex-Bank Negara Governer Datuk Jaffar Hussein. According to ex-Bank Negara Deputy Manager, Dr Rosli Yaakop the main culprits are Nor Yakcop and Datuk Jaffar who are responsible in speculating and gambling away Bank Negara funds. To create an impression that Bank Negara had ‘a team of forex traders’ Nor Yackop used both his and the staff’s computer to do the buying and selling.

The reason for the RM30 billion losses from foreign exchange trading is mainly due to Nor Mohamed Yackop’s bet that the Bank of England would float the Sterling during the 1992 European Financial Crisis. Mahathir ordered Bank Negara to purchase large amount of the Sterling in the hope that it will appreciate once it is floated. Meanwhile his rival, George Soros through his Quantum Fund established short positions using currency forward contracts and options to the tune of US10 billion. Other currency speculators sensed the kill and soon join in the fray and together they drove the pound down. Soros walked away with US1 billion for a day’s work while leaving Mahathir with more than RM30 billion losses. Later Soros is known as ‘the man who broke The Bank of England’. This was the main reason why Soros was so unpopular with the Malaysian media. He and Mahathir have gone into many heated arguments and name calling later on during the Asian Financial Crisis.

While in Argentina Mahathir called upon Nor Mohamed Yackop (since he was the only dude that has the most experience with foreign exchange) to enlighten him on the inner workings of the foreign exchange market.

At the same time Mahathir also asked Nor Mohamed to design the country’s capital control policy. Practically what he (Nor Mohamed) did was he went through the Country’s Balance of Payments report line by line looking for any leakages to prevent any capital outflow from the country.

Needless to say this strategy proved to be too complicated to comprehend and also caused a lot of confusion later on. The border control forms and other forms that designed to track the movement of the ringgit proved to be very confusing. Due to the lack of time and to fast track the process these forms are copied from other countries, presumably from Argentina and other Latin American countries since they are the experts in capital control. For example one of the conditions for funds that are raised from the sale of equities and other investments had to be remained in the country for a minimum of 12 months. However it is not specified whether the residents and the locals are required to do so and consequently it created a lot of confusion. As a result the NEAC Communications Team was formed to deal with the problem and also in educating the people.

Capital Control implementation

The NEAC had been toying with the idea of Capital control many times in the past. Bank Negara Malaysia has been the most ardent opposition to the use of capital control knowing its repercussions or after effects. From empirical analysis of other countries that have adopted capital control, any future capital fund raising in the international markets will be shunned by investors and hence the costs of funds will be high.

Before we go further into Malaysia’s foray into implementing its capital control, I think it’s best for us to understand what is Capital Control. When a country exhausts itself of Monetary and other Policy tools to stabilize the economy, then the last resort will be to implement capital control. Normally it will only be implemented when funds are leaving the country in a big manner.

Capital control is an attempt by a Government to introduce policies to control the free flow of funds not only in and out of the country but also within its borders. Below are some of the more common types of capital control.

- Controlling the foreign exchange transactions.

- Controlling the international bank transfers

- Confiscation of Precious metals like gold and silver

- Fixing the Exchange rate

- Controlling the amount for bank withdrawals

On the 1st day of September 1998, Prime Minister Dr Mahathir Mohammad announced the capital control. Malaysia's capital control is a mix of the above measures and nothing new despite the press claimed it was unique because Malaysia did not embrace the IMF. The following measures are taken to ensure that the objectives of stabilizing the Ringgit and control the capital flows are accomplish.

- Overseas bound Local travellers are only allowed to take up to RM1,000.

- Remittance of funds by residents to overseas are capped at RM10,000.

- Ringgit is pegged to the dollar at the rate of RM3.80 to US1 to facilitate trade in the domestic sector.

- Any ringgit remains outside of Malaysia considered not legal tender. This is to prevent speculators from borrowing the ringgit offshore to sell it in the domestic market for dollars. In other words to perform short selling on the ringgit and when the ringgit depreciates they will buy it back to repay their offshore ringgit loan.

- Any credit facilities obtained overseas need to seek approval first and only companies that earn foreign exchange are allowed to obtain offshore credit.

- Funds raised from the sale of equities or other forms of investments need to be remain in the country for 12 months. This is to prevent short-term capital flight.

- Clearing of Stocks listed on the KLSE can only be done on the KLSE or its approved exchanges.

- RM500 and RM1000 currency notes are made non legal tender to prevent smuggling of Ringgit to neighboring countries.

- Dealing of shares in CLOB was made illegal to prevent the flow of funds to Singapore and also discourage the arbitraging of shares between the two exchanges.

Reasons for Malaysia’s success

The capital control does bring some stability into the economy because it helped not only stabilize the Ringgit but also prevent a black market for it. The following are some of the reasons that may help explain Malaysia’s success in its Capital Control.

- Its Authoritarian Government.

Asian values such as maintaining good relationships, respect the elders, upholding harmony and family closeness are some of the reasons that enabled the existence of an Authoritarian Government. Authoritarian Government is one of the main elements for the rapid economic growth in ASEAN. Singapore’s government under Lee Kuan Yew is often criticized for being too authoritarian and so did Dr Mahathir Mohammad and Indonesia’s Suharto.

Being an authoritarian government, it enabled Mahathir to push both state-led and private corporations into cohesion so as to achieve its objective. The pursuit of autonomy on its economy started since the May 13th 1969 racial riots. It was agreed that the main reason for the racial riots is due to the inequality of income distribution between and Chinese and the Malays. The Chinese seems to be predominantly controlling most businesses and hence at the expense of the Malays. In order to ensure more equitable distribution of income The New Economic Policy was born in 1971. To close the gap between the Malays and the Chinese business licenses, monetary assistance, employment in public enterprises, property purchase discount (10%), ownership quota (minimum 30%), universities intake (more than 90%) and a myriad of other discriminatory policies are enacted.

It would be a dream for Western politicians to exert such autonomy on their economy and its people. So the 1997-1998 Crisis provided another platform for Mahathir to seek autonomy and this time from the international investors. At that time (end of June 1998), the Ringgit was plunging towards the RM4.80 mark, capital flight is increasing and interest rate is sky rocketing.

- The Crisis is Urban confined

Due to the structural transformation of the Malaysian economy since the 1980s after the Crash of the tin price which was brought about by Mahathir’s effort to corner the tin market in 1980 which caused the Malaysian taxpayers more than RM 1.6 billion. In December 1980, Malaysian Mining Corporation through its subsidiary Maminco (short form for Malaysian Mining Corp) secretly made large purchases of tin futures in the LME to the tune of 50,000 tones. As expected the tin price went up furiously. It not only attracted the attention of other tin producers from Brazil and Indonesia to increase their capacity by 69% but also the US to release its strategic stockpile.

Needless to say eventually the tin price crashed. The crash not only left Malaysia with more than RM 1 billion in losses but also devastated many mining towns in Malaysia. It not only cost Malaysia another source of income from tin mining but also its reputation as ‘The largest tin producer in the world’. I was from Ipoh and during the 1970s it was the most prosperous town in Malaysia and it is also known as the ‘Tin City’. Eventually most tine miners closed shop and went into other business and Ipoh had now been transformed into ‘Eat City’ with specialty such as bean sprouts chicken, salted steam chicken, char kueh teow, white coffee, beef noodles, fish ball noodles and many more.

Malaysia has since been more diversified by transforming itself from an agrarian economy to a manufacturing economy. Import substitution and export-led industries such as electronics are the main activities and contributed much as the engine of growth.

At the same time the high price of agricultural commodities such as palm oil and rubber also helped cushion the impact of the crisis in the rural areas. This is because the rural economy depended much on rubber and palm oil plantations and helped not only insulated it from the onslaught of the crisis but also contributed to the vibrancy of the rural economy. Hence, Malaysia had one less problem to tackle and can concentrate its fight in the urban economy.

- Malaysia’s Debt/GDP was smaller

Due to Bank Negara Malaysia’s stringent control on offshore borrowing by local corporations, Malaysia’s external debt did not pose any danger to its Debt/GDP ratio. This was in response to its earlier experience during the 1987-1988 Crisis. Only Malaysian companies that are earning foreign receipts are only allowed to raise capital overseas. Hence this helped it to control its external debts especially the short-term ones. The following table shows the Debt/GDP of the most affected countries during the crisis.

Debt/GDP

| |||

Country

|

1996

|

1997

|

1998

|

Malaysia

|

37.5

|

42.1

|

52.6

|

Korea

|

27.5

|

33.3

|

45.3

|

Thailand

|

67.4

|

68.2

|

76.1

|

Indonesia

|

48.8

|

52.3

|

122.5

|

Hence with a relatively lower than its neighbours Debt/GDP, it helped Malaysia to escape much of the brunt of the crisis.

- Delayed response to the crisis.

There are many arguments on why Malaysia is slow in responding to the crisis or ‘kicking the can down the road’. Below are some of the reasons.

By the time Malaysia imposed the capital control (1st September 1998), the crisis had already devastated other countries by more than a year. Much of the foreign capital that had already left is now coming back to ‘bottom fish’ since much of the equities and asset prices are offering at rock bottom prices. Further to that those IMF-3 economies that embrace IMF aid are on their way to recovery. Hence, this provided a less risky approach to implement capital control then and spared Malaysia’s on much of the catastrophic effects of capital control such as currency black market.

- Absence of black market currencies

One of the associated side effects of capital control is the creation of a black market for currencies. Due to the increased demand for US$ more people will be willing to pay more Ringgit for the dollar. Hence in the black market instead of the stipulated US$1 to RM 3.80 people are willing to pay more say RM 4.00.

This did not happen in Malaysia because due to the authoritarian nature of our government, Bank Negara Malaysia is able exert full control on commercial bank operations. Commercial banks then are warned not to mess around with the currency black market. The government through the NEAC also liaise Bank Negara with the Customs Department so as to control the smuggling of the Ringgit and dollars between its border with Singapore and Thailand.

Since capital control meant that the dollar’s movement in and out of Malaysia will be curtailed and this will create an impression that the supply is limited. Hence this will lead people to hoard the currency. Added to this people are afraid when the Ringgit devalues again so they are willing to pay more for the dollar to stash it in their vaults or under the pillow. Such a move will also means that the value of the Ringgit has gone down and hence if not curbed will lead to inflation. Another effect will be the loss of confidence on the Ringgit and traders will refuse to accept Ringgit being afraid that it will lose its value soon. During the crisis I still remember there was a ‘capital flight to safety’ of deposits from local banks to foreign banks. People are withdrawing their savings desperately from local banks because they are afraid they will collapse. It went to the extent where Maybank was offering free Astro installations for every RM 50,000 term deposits.

Why took so long?

Why it took so long for the capital control to be implemented? It took more than one year since the crisis started on 2nd July in Thailand. The following may be the reasons for the delay.

- Running out of options. The authorities have tried many selective capital controls and unorthodox economic approach to stabilize the Ringgit. This also served as a STOP GO measure for it to buy more time so that when other countries starts recovering, Malaysia will then participate in the recovery to turn around its economy.

One of moves involves the selling of dollars by Malaysian exporters with large Dollar receipts. The idea is to use the Malaysian companies to sell their Dollars for Ringgit which in turn will push up the value of the Ringgit. This will give more pressure for currency speculators to cover their shorts and at the same time make it more expensive. However due to the overwhelming sales of the Ringgit by the speculators the local companies are unable to cope and finally gave up their attempt. Since time is of essence and if capital control is not implemented then Malaysia will be in deep trouble and has to seek IMF aid.

- Timing of the execution. A different approach between Dr Mahathir and his Deputy Anwar Ibrahim who is also the Finance Minister then. Anwar was the blue eye boy of Washington and even the Wall Street Journal called him the ‘calm voice of economic reason’ during the crisis. Anwar prefers the orthodox approach of free market enterprise policies like increasing the interest rate to protect the ringgit and also a contractionary fiscal policy to balance the budget following the lines of the IMF austerity program. Their difference led to the sacking of Anwar on 2nd September, a day after the imposition of the Capital control.

Another main reason for the delayed response is the internal bickering between Mahathir and his deputy (Anwar Ibrahim – Finance Minister then). The imposition of the capital control is ‘purposely timed on the 1st September 1998’ because they know that Anwar is going to be sacked the next day. If capital control is imposed after Anwar is sacked, then heck there will be another round of capital flight not only from Malaysia but also from the IMF-3. The situation will turned worse and might further undermine the recovery efforts of their economies. And this time Malaysia might not be able to survive and thus turning to the IMF is the next option.

Mahathir knows that if the IMF is allowed to come in then his legacy as well as the NEP’s (New Economic Policy) one-sided policies implemented for the past 20 over years will be dismantled. Not only public enterprises and private corporations that are not competitive will either be sold or merged as seen in Thailand, Indonesia and South Korea. Looking at what has been implemented in the IMF-3 since the Crisis, we may see the following changes in Malaysia.

Malaysia’s bloated civil service will also need to be trimmed. Loss making banks and other financial institutions will either be closed down or sold to foreign banks. Foreign banks will be allowed to own up to 100% equity in local banks like those in Indonesia. Malaysia’s national car project PROTON, Perwaja Steel, all the IPPs (Independent Power Producers), Light Rail Transport, PLUS, Indah Water, AMMB, RHB, Bank Bumiputra, Renong Group, Time Engineering, Bakun Dam and other remnants of crony capitalism will have to go. There will be no more ‘Bumiputra status’ because IMF believes in equal opportunity policies. In other words, Joseph Schumpeter’s ‘creative destruction’ where survival of the fittest will prevails.

Coming back to present

Fast forward to present in 2013, we should ask ourselves what is the difference between the Asian Financial Crisis in 1997 and the Global Financial Crisis in 2008? To begin with both crisis are caused by too much money in the economy which led to both companies and individuals to be over leveraged. Unable to withstand a credit crunch, over leveraged companies and individuals finally will have to succumb to the crisis. Below, I present to you a graph on the full cycle of the current financial crisis and the various measures adopted to overcome it. I will go through each of the following Stages (1-4) to explain why current policies is not working and getting us nowhere.

- Money Supply (1)

After the Asian Financial crisis we became complacent and forgot how it affected us all. We are again back to our old habits of getting into debts, consume more and saving less. We forgot how the stock market crash wiped out our portfolio and high interest rates are causing havoc in our mortgage payments. We thought that the good times are back and got ourselves into debts again. In part we also have to thank our Government for relaxing the rules governing consumer and corporate debts. As a result we got ourselves highly geared and when Lehman Brothers collapsed in 2008, it took the world economy down with it. Hence here we are again back to square one as it is in 1997.

So to stimulate the economy out of the doldrums again the Fed and the Central Banks around the globe embark on a credit expansion program known as Quantitative Easing. What is Quantitative Easing and how it works?

A simple explanation of the Quantitative Easing will be credit expansion by the Central Banks. Through its Open Market Operations a Central Bank can increase the Money Supply in the economy by buying bonds or securities from banks, corporations or the public. For the banks, funds will be deposited into the accounts held by the banks in the Central Bank or issue cheques in the names of the corporations or the public. At the end of the day the Central Bank will flood the banks with excess liquidity which will promote lending. Hence it will put more money into people’s hands which they will then spend.

Another thing I reckon most people don’t realise is that Bank Negara does not print the money physically and it does not operate a printing press. Instead the money is created by digital entries in the computer screen. Banks will be credited by credit entries in their accounts held in Bank Negara. And this is why Quantitative Easing is also known as ‘printing money out of thin air.’

How successful the Quantitative Easing depends on the basis of the Keynesian Multiplier. To see how the Keynesian Multiplier works I shall illustrate with the following. As from above as a result of Quantitative Easing, people have more money to spend. This represents the first round of money from the Government to the people. When people received the money in the form of loans or refinancing they do not spend everything. Instead they will only spend a portion of it and in economics it is known as the Marginal Propensity to Consume (MPC) or MPC dollar. This MPC dollar spent will then trickle down into the system to more people. Thus this will create a second round of spending by the people (fraction of the MPC dollar) and not the Government. As then there will be the third, fourth and many more rounds of spending. The sum of these effects as a result of the initial funds injected by the Government can be quantified with the following formula.

Keynesian Multiplier = 1/(1-MPC)

Remember earlier, the MPC is the fraction of the money people spend on the amount of income they receive. Hence say if someone receives a loan of $1000 and spends $800 then the MPC = 0.8 ($800/$1000). If the MPC is 0.8 then the multiplier effect generated from the expenditure can be calculated with the Keynesian Multiplier.

Multiplier = 1/(1-0.8) = 5 times

Also be noted that if people are willing to spend more from their income or their MPC = 0.9 then the Multiplier will be 10 times.

Another thing to be noted is that this Multiplier effect works two ways. In times of recession there will be a decline in consumption based on the fact that people are more cautious due to the uncertainty going forward. For every dollar cut in expenditure in round one, it will result in further cuts in expenditure in round two then round three and round four and so on. As a result there will be a much larger decline in the overall consumer expenditure and this will lead to a recession later. Businesses will also going deeper into the red due to the negative multiplier effects of consumer spending. So now you know why Governments prefer spending and increasing debts than saving and reducing debts.

- (-) Interest Rates

With the huge influx of money generated as a result of the Central Bank purchase of financial assets from the banking sector (in Stage 1), it will put pressure on the interest rate in the banking system. Interest rates will have to decline in the short in order to get rid of this excess liquidity or what can be term as ‘Liquidity Effect’. The profitability of a bank depends on Bank Negara’s Monetary Policy and in this case easing the Money Supply will certainly affects a bank’s balance sheet. The more liquidity or money it has then the more loans it can make and hence more profit. In a way bank’s balance sheets depend on a lot on Government Policy. Hence the banks will have to find ways to lend out the excess money by offering better terms or relaxing lending rules.

- Inflation

With the excess liquidity created in Stage 2, consumers will have more money to spend and hence the demand for goods and services. Economic activity will be sizzling at this moment. Due to this short term excess demand over supply it will create what known as a ‘Demand-Pull’ inflation. This lag or deferred impact of excess liquidity on the increase in prices (inflation) is also known as the Fisher Effect. This is what we are experiencing for the last couple of years as a result of Bank Negara’s Monetary Easing after the Global Financial Crisis in 2008.

- (+) Interest Rates

Due to the increased economic activity, businesses and consumer will be demanding for more loans. Coupled with inflation created in Stage 3, the excess demand for loans will automatically push up the interest rates. Once lenders sensed an increase in the inflation rate, they will have to cover their backs by increasing the interest or lending rates. If not the expected future increase in inflation rate will erode their profits. Hence an ‘inflationary premium’ has to be priced into the interest rates.

So how will our Government or Bank Negara going to address the problem of increasing interest rates? Well, you don’t need to be a rocket scientist to figure it out. Yes, the solution is to prevent the interest rate of getting higher. One method is to reduce the demand of money by way of ‘Credit Crunch’ as we have already experienced since July this year. Bank Negara ‘shortened the maturities’ of both housing and personal loans then. However this method will have the effect of collapsing the consumption and certainly it won’t bodes well for the economy in the short term.

Another method is to increase the money supply. So, Bank Negara will do another round of Quantitative Easing and inject more money into the system again, so as to remove some pressure off the interest rates.

HOLD ON FOLKS !! By increasing the Money Supply, are we going back to Stage 1 again or where we started in 2009? Damn it !! We haven’t solved a single problem. You see by injecting more money into the system, it will not solve our problem. No doubt, it will help revive and sizzle the economy while preventing further hikes in interest rates. But on the other side of the coin it creates a situation where inflation begets inflation and the final outcome will be a more inflationary situation.

Wrapping Up

In wrapping up, I reckon that we have yet solve a tiny bit of the current Global Financial Crisis as indicated by the multiple Quantitative Easing implemented by the various Central Banks around the world. The latest evidence of the inability of Central Banks to quit Quantitative Easing is the Fed’s decision to delay its tapering activity. Anyhow if the Fed does go ahead with the tapering of $10 billion a month, it will not make much difference. This is because the Fed currently pumps in about $85 billion a month into the economy so a $10 billion reduction per month doesn’t seem to be much.

What is interesting about the effects of past Quantitative Easing is that it not only helped build up the debt load of the public sector but also the private sector.

Below I present to you the debt load of High Grade U.S Corporations that have been built up since 2006.

As can be seen above from the CITI charts, currently there is a resurgence or what is also known as ‘re-leveraging’ of corporate loans to record levels in the U.S. The bad news is that most of the loans are used for funding dividends and share buybacks instead of capital spending or hiring. This will not help much towards building a sustainable economy.

Below is the chart of Malaysia’s private sector debts which I reckon is not much better off than our counterpart.

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

438

|

18

|

456

|

Private

|

749

|

239

|

988

|

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

51%

|

2%

|

53%

|

Private

|

87%

|

28%

|

115%

|

From the above we can conclude that at the present moment, the private sector poses a greater risk to financial default than the public sector. Our private sector debt/GDP has reached 115%. Hence the net effect of Quantitative Easing is not only causing a run-up of private sector debts but also produces a highly inflationary situation. If Bank Negara proceeds with further Quantitative Easing then we shall expect more inflation and private sector debts in the future. However, if Bank Negara stops credit creation completely then our economy will plunge into deep recession because economic activity will come to a standstill.

In short, there is no easy EXIT strategy available. That also meant that all Central Banks including Bank Negara have fallen into the ‘merry go round’ credit creation circus. It is not easy for them to reverse course. Their predicament also meant an opportunity presented upon us. How can we capitalize on this?

Crippling our Banking System

You see banks operate on a system known as ‘Fractional Reserve Banking.’ The concept of fractional reserve banking operates in a similar manner as the Keynesian multiplier effect on consumption. To illustrate how Fractional Reserve Banking works, I will use the following example. In the banking industry there is a statutory requirement or SDR (statutory deposit ratio) that banks must adhere to. It is the amount of money banks sets aside as a percentage of the deposits (normally 10%) as an insurance against rainy days.

When a bank receives RM100 deposit, it can lend out RM90 after deducting $10 for the SDR. The RM90 will eventually make it’s way back to the bank and then the bank will again lend out RM81 after deducting RM9 (10% for SDR)). This process will go on until it finally reached RM1000 (RM100+RM90+RM81+ … = RM1000) or 10 times leverage. To calculate the total leverage or multiplier we can use the following formula.

Multiplier = 100/SDR

Hence, in our case the SDR is 10% then the multiplier = 100/10 or 10 times.

Since our banking industry operates on the premise that not everyone will withdraw their money simultaneously. This is because during a normal day-to-day operation, one person’s deposit will cover another person’s withdrawal also known as the ‘netting effect’. What happens if all the depositors withdraw 15% of their deposits simultaneously? It will immediately cause a bank run because there is not enough cash (only 10% of deposits) in all bank vaults to meet the 15% withdrawal.

Hence this presents us a potent tool to get even with our Government. If our Government continues to push us against the wall then we can use this tool to bring our Government down to its knees. How can we do it?

All we need to do is to set a date say November the 15th 2013, and we gather as many people as possible (email, facebook, twitter, linkedin and etc) to withdraw 50% of their deposits from their banks. If we can manage to get 20% of the depositors to withdraw 50% of their deposits (total = 10% of all deposits) then a bank run will be assured. By that time our economy will be crippled and our Government will either have to bow to our demands or implement capital controls to limit withdrawals.

Before I pen off, thinking out of the box, there is one problem that I have been figuring for the past year. As a democratic country our Government is elected by us the Rakyat. Does this mean that whatever resources we have in this country also belongs to the Rakyat? Does that include the money supply or the M1 and M2 since Bank Negara can expand and contracts it? If this is the case then why should we the Rakyat need to pay interest rate when we borrow from the Government (also the Rakyat)?

Since Bank Negara (also belongs to the Rakyat) have the ability to create money out of thin air, why not it lend direct to the Rakyat at a very low or even free interest rates? Why give money to the bloodsucking middle men banks that charges us exorbitantly high interest rates? In the end the Rakyat suffers and be slaves to the banks while they are making obscene amount of profits. At the end of the day it only benefits the small group of elite shareholders at the expense of the Rakyat.

Can some experts in political science or law out there enlighten us on this matter?

If a solution can be worked out, I reckon this will be a good tool for Pakatan Rakyat in its next GE manifesto to push for lower interest rates as one of its agenda. This will surely benefit us in reduced mortgage payments and thus at the same time also helping to reduce the number of bankruptcy (especially credit cards) cases in our country. Besides, Pakatan Rakyat will surely garner more votes.

Samcheekong.blogspot.com

No comments:

Post a Comment