Why Unemployment Rates Matter to Your Retirement

My biological clock is ticking—as is yours and everyone else's. With each passing day, you are either moving closer to or further past the day you quit working full time. Baby boomers are retiring at a rate of 10,000 per day and will continue to do so for the next 17 years. Whether you count yourself among that group or not, understanding where economic data—such as unemployment rates and inflation—come from will make you a better investor and savvier retiree.

The Federal Reserve has some laudable goals. Its current mission includes inflation control and employment promotion, and it uses data from the Bureau of Labor Statistics (BLS) and the Departments of Labor and Commerce to formulate policy. Investors look at those same numbers, try to anticipate what the Federal Reserve might do, and invest accordingly.

On unemployment, the Fed notes:

"(I)n the most recent projections, FOMC participants' estimates of the longer-run normal rate of unemployment had a central tendency of 5.2 percent to 5.8 percent. Though a variety of factors influence the level of unemployment in the economy, the Federal Reserve makes monetary policy decisions that aim to foster the lowest level of unemployment that is consistent with stable prices."

And on inflation:

"The Federal Open Market Committee (FOMC) judges that inflation at the rate of 2 percent (as measured by the annual change in the price index for personal consumption expenditures, or PCE) is most consistent over the longer run with the Federal Reserve's mandate for price stability and maximum employment. … The FOMC implements monetary policy to help maintain an inflation rate of 2 percent over the medium term."

And here is how the Fed evaluates inflation when making policy decisions:

"(P)olicymakers examine a variety of 'core' inflation measures to help identify inflation trends. The most common type of core inflation measures excludes items that tend to go up and down in price dramatically or often, like food and energy items. … Although food and energy make up an important part of the budget for most households—and policymakers ultimately seek to stabilize overall consumer prices—core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends."

Hmm. There are many fallacies in that approach. Sometimes the premise or data is incorrect. Many times the Fed has made predictions that were totally incorrect and then had to jump in to try to clean up the mess when unforeseen bubbles have burst.

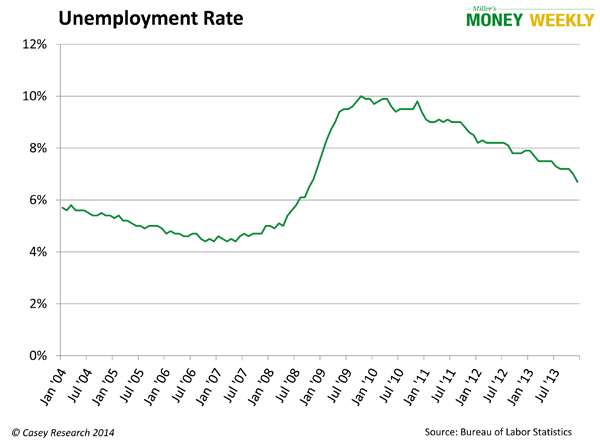

Debunking the statistics. The graph below shows the official BLS unemployment statistics. In December 2004 the unemployment rate was 5.4%. Since then it has gone from a low of 4.4% to a high of 10% in October 2009. The current reported rate is 6.7%.

The Federal Reserve committed to holding interest rates down until the official unemployment rate hit 6.5%. Mike Meyer, vice president at EverBank, weighed in via the Daily Pfennig:

"Based on this official number, the job market is getting a lot better. There's only one big problem: the official number doesn't really reflect the health of the labor market.

That probably explains why the Fed has moved away from the 6.5% target. Last November, former Fed chief Ben Bernanke said that short-term interest rates might stay near zero 'well after' the jobless rate falls below 6.5%. ... It seems even the Fed has realized the official unemployment rate is flawed."

Meyer also notes that many believe the reason unemployment numbers are dropping is because baby boomers are now rapidly retiring; however, the number of workers over age 55 has actually increased over the last five years.

The key to understanding unemployment rates is the Labor Force Participation Rate—meaning the percentage of the population that's employed. When the BLS calculates the unemployment rate, it doesn't consider a person whose unemployment benefits have run out and is no longer looking for a job to be unemployed. I guess that means if everyone quit looking for a job, the unemployment rate would be zero?

Meyers went on to write:

"The drop in the number of people who are looking for a job has helped bring the unemployment rate down. In fact, some economists estimate that if the LFPR was at the same level where it was before the recession (66.4% in January 2007), the unemployment rate would be 11.75%."

Other think tanks like Shadow Government Statistics publish their own unemployment statistics:

"The decline in the headline U.3 unemployment rate, from 7.0% to 6.7%, was not good news. The large drop in the number of unemployed mostly reflected people becoming 'discouraged' and being statistically removed from the headline labor force, instead of finding jobs and returning to work. The increasing flow of discouraged workers through the broader U.6 measure, into the ShadowStats-Alternate Unemployment measure, boosted the ShadowStats unemployment rate to 23.3% from a revised 23.1%."

We know the Federal Reserve was committed to holding interest rates low until the official unemployment rate dropped to 6.5%. That would tend to indicate people were back at work, the economy was improving, and the market could absorb higher interest rates without putting us back into a recession. Now the Fed has backed off on that commitment and is signaling it will hold interest rates down well after unemployment falls below 6.5%.

What difference does it make? For those who are investing their life savings—which they can ill afford to lose—it makes a lot of difference. There's no point in arguing about whether unemployment is 6.7% or 23.3% or anywhere in between. What matters is how those numbers affect our investments decisions—and the decisions of others.

If the economy is doing well, that means companies are hiring and profits are increasing. It's a good time to be heavily invested in the stock market. If the economy is not thriving and people are not working, then businesses will suffer, and many will fold. Retirees can ill afford to put a major portion of their nest eggs into the market based on a false premise. The risk is much too great.

How many of our favorite restaurants have shut down since the 2008 crash? In a down economy, business suffers and so do investors—eventually. The Federal Reserve, with its various stimulus programs, is just kicking the can down the road.

If data from the government or the private sector are unreliable—or suspected of being so—we're investing in the unknown. Investors will move cautiously and spend less freely because they're worried about an uncertain future.

What about inflation? The Federal Reserve has deemed a 2% inflation rate good for the economy. Inflation is a hidden tax that hurts seniors and savers immensely. If you invest in a Treasury bond paying 2% and inflation is 3%, when your bond matures you have more money in the bank but less buying power. Keep it up and you can kiss your lifestyle goodbye a lot quicker than most folks realize. Go to any potluck dinner in a 55-plus community and you will hear folks complaining about how expensive things are getting.

The Consumer Price Index is used to calculate inflation. Many people think the CPI is based on a constant basket of commonly purchased goods, with the current prices adjusted from year to year. That is inaccurate; the BLS has changed its formula many times.

Why does that matter? For one, the CPI is the basis for Social Security increases every year. Many Social Security recipients have noticed their Medicare premiums increase faster than their Social Security checks. The government has a great financial incentive to keep the official CPI number as low as possible: the lower the number, the less it has to pay.

The Federal Reserve uses many measures to calculate the impact of inflation; they just happen to exclude food and fuel, for example. That makes it hard for investors who happen to eat and drive to grasp the relevance of the numbers.

This is damn important for investors! Why? Interest rates rise during times of high inflation, which dramatically impacts the yield on government-backed securities and top-quality bonds. It's because of inflation—and inflation fears—that savvy investors have backed off from safe, fixed-income investments. Right now, they're a surefire way to make sure your money does not last forever.

The Fed's zero-interest-rate policy (ZIRP) means that if you invest in US Treasuries, you will likely lose ground to inflation. That's good for the government and bad for investors.

The BLS website has a handy inflation calculator. Most people are told to plan for 30 years of retirement. If you retire at age 65, make sure you have enough to make it to 95—and probably much longer.

According to the BLS calculator, something that cost $10,000 in 1983 will now cost $23,389.26. That presents quite an investment challenge—considering the Federal Reserve has been printing a trillion dollars a year for the last several years. Who knows what the inflation calculator will look like 30 years from now?

The market is currently trading in anticipation of what the Federal Reserve is doing (called "sentiment") as opposed to the true growth of the economy and success of the individual businesses (called "fundamentals"). That, coupled with a great level of distrust in our government, our currency, and the role of the Federal Reserve, affects each and every investment we make.

In the meantime, the biological clocks of baby boomers continue to tick. The headline numbers for unemployment and inflation are for the benefit of the politicians, not investors. That's why we're dedicated to showing investors how to safely invest in today's market. We have no choice but to put our money into investments that are riskier than the previous generation did. Still, there are safety belts available to minimize risk.

An educated investor who reads more than the headlines, understands what is really going on, and does not invest emotionally can still enjoy retirement.

Our Bulletproof Income strategy is designed to give conservative investors the best possible returns with minimal risk. Our Bulletproof Income portfolio is designed to provide safe income—well ahead of inflation—with good diversification and safety belts to protect you and your money. If you haven't done so, I would urge you to sign up for a no-risk subscription ($99/year). Sign up and receive a copy of my book, Retirement Reboot, all of our special reports, and our monthly issues. If you decide we're not for you, cancel within the first 90 days and receive a full refund, no questions asked. Feel free to keep the material you've downloaded as our thank you for taking the time to look us over. Click here to learn more and get started today.

The article Why Unemployment Rates Matter to Your Retirement was originally published at millersmoney.com.

No comments:

Post a Comment