Our exports are now consists of electrical and electronics – 35%, palm oil – 15%, petroleum products – 9%, LNG – 7% and the rest are made up of timber, various manufactured goods and etc. Our imports are mainly made up of machinery and transport equipment – 60%, manufactured goods – 12%, fuel - 10% and chemical - 9 %. The interesting thing to note about Malaysia’s imports is that the bulk of it are made up of ‘Capital Goods’ and not consumer items such as food, beverages and etc. When a country imports more capital goods than anything else it shows that this country is on the right track to a ‘sustainable developing’ economy because these capital goods such as machineries and transport equipment will be used to furthered the production of manufactured goods and hence helped promote economic growth.

Government watering our wages?

Below we present to you several development and income metrics of the Malaysian Economy which we hope to help you understand where our money gone and also why our ‘income distribution’ is not catching up with the system. We hope you can bear with us as it is quite statistical and boring.

The macroeconomic metrics we used are the following:

- Wages in Manufacturing

- Malaysia GDP

- Wage/GDP index

- Malaysia Government Debt/GDP

- Malaysia Money Supply M3

- Malaysia GDP per capita

- Malaysia Government Spending

- Malaysia Consumer Spending

- Malaysia Consumer Price Index

- Malaysia Government Budget

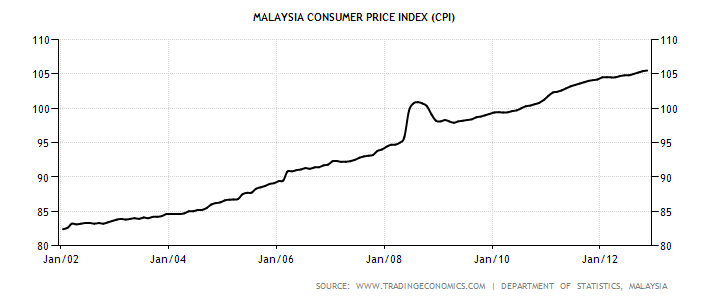

Later we will also show the inability of income to catch up with general price level of goods and services or inflation which is measured by the CPI. Hopefully it will also help us to answer the following question on whether the authorities are watering our worker’s wages?

Why our Income lagged GDP Growth?

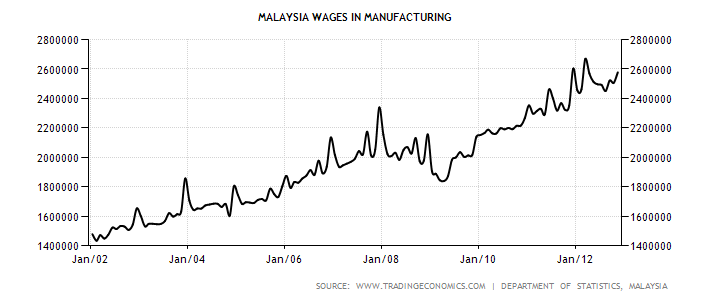

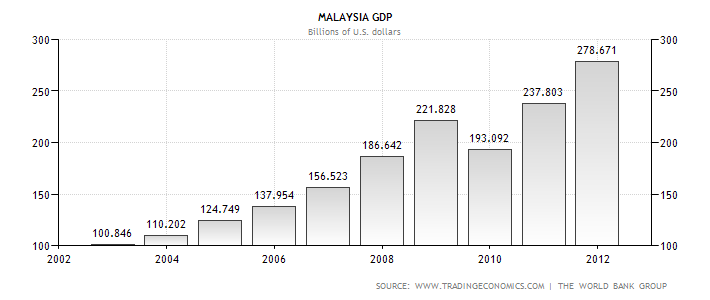

As far as we know there are not many papers written on this subject and reasons being the lack of interest or simply not reported in the mainstream media to avoid any troubles with the power to be. Anyway we present to you 2 charts on the wages in manufacturing and also the GDP growth of Malaysia as a basis for our comparison. Wages in manufacturing is selected because the manufacturing sector employs the most people in Malaysia.

The following is a chart on the Manufacturing wages to GDP that we plot using data from the above wage and GDP charts. It clearly shows that the worker’s share of the GDP has certainly been dropping since 1999. So where have the bulk of the remaining GDP went?

Certainly not us and you folks! The main culprits are the Government and its unscrupulous cronies and capitalists. With the projected FBMKLCI earnings growth of 8.0 and 8.4% for 2013 and 2014 respectively, obviously things are looking good for the corporates ahead. With an average earnings growth rate of 8% for the past couple of years while the ratio of Wages/GDP declining it is obvious that those bastard capitalists have been capping the increase in wages so as to maximise their profits. Since Malaysia’s competitive level has been declining, the question is how those companies are able to keep recording increasing profits?

Green Belt help creates scarcity

One explanation will be the effects of inflation and the other being the existence of so called ‘Green Belt’ industries. The term Green Belt originated in London during the 1930s where the periphery of land surrounding the city was accorded this status. Property developments are discouraged in this area by tough regulations so as to create what we call ‘scarcity’ in economics. The main reason is to control the amount of housing in this area so that property prices and rents will always be high because there are not many choices or alternatives to choose from. Another reason is to control the amount of people living in the city so that the city will be free from congestion, pollution and other social problems that are associated with increased population. In Malaysia we have our version of the Green Belt in Kuala Lumpur. It is located in the Bukit Bintang area and also known as The Golden Triangle. Rentals in this area are able to match those in other major cities around the world like Singapore, Taiwan, New York and so on.

Coming back to our discussion on Green Belt companies that are able to capitalize their strengths from scarcities that arises within their Industries. Due to the nature of granting licenses in Malaysia, it enable many companies virtually operate in a monopolistic manner. Economists call this type of behaviour ‘Rent Seeking’ which is common in Malaysia. Due to their Green Belt status like which commands scarcity, there are able to charge higher price to consumers at their whims and fancy. Take the Cable TV business as an example, there is only ONE company that has the license to operate this business. Due to scarcity and being the monopoly, consumers are left with one choice – take it or leave it. When they raised their prices last year subscribers have no choice but to succumb to their whims.

Similarly in the power generation business licenses are given to the so called IPPs (independent power producers) to generate electricity which in turn sold back at a much higher price to our national utility company (TNB). These IPPs are able to enjoy Green Belt status as there are ensured that the barriers of entry are high and TNB will have to buy whatever amount of electricity that are generated. As a result these companies are assured of big profits every year. Other companies that enjoyed Green Belt status are PLUS Highway, Petronas, Indah Water, Bernas, FOMEMA and many more. These companies are able to raise prices without attracting much competition from competitors due to their strength from scarcity.

Malaysia’s Government Debt/GDP had been stabilizing around the mean of 43 % up till 2009. However since the year 2010 it had shot up to 55.4 % and had been remaining above the 50 % since then. This is attributed to the RM 67 billion that is raised during the 2009 period in respond to the 2008 Global Financial crisis which was used as a stimulus package.

This sudden upsurge coincides with the increased in the Government spending which is reflected by the record deficit of -7.4 % of GDP in 2010. The following chart shows the gradual increase in the Government spending which only accelerates in recent years. Having a Debt/GDP of 52 % doesn’t mean we are in a comfort zone because when Ireland and Portugal defaulted their Debt/GDP is less than 70%. Further to this we cannot compare to Japan whose Debt/GDP is 211 % as of Nov 2012. We will explain shortly why Japan’s economy will not default even with such high level of debts.

Government Pump Priming the Economy

Pump priming refers to efforts by the Government to inflate the economy by initiating policies that will help expand the economy and hence its activity. It is no secret that most Governments in the world today are artificially boosting their economy either by depreciating their currencies, creating trade barriers or simply embark on an expansionary monetary policy in order to achieve full employment. The world economy is currently facing an extremely challenging time ahead as most Western economies are contracting and what will happen next will be the inevitable ‘Currency Wars’. By this we mean sooner or later each and every country will have to compete with each other by devaluating their currencies so as to make their exports cheaper which will help create jobs. Side effects of currency wars are Global Central Banks will increase their efforts to protect their economies by printing more money, create tensions among nations, beggar thy neighbour and lowering of bond yields due to currency interventions will also help increase interest rate sensitive consumption.

To begin with Malaysia’s money supply had been steadily increased for the past few years. The following chart shows Malaysia’s Money Supply as of 2002 till 2012.

Malaysia’s total Money Supply consists of M0+M1+M2+M3 which can be divided into the following,

- M0 which is the most liquid of all. This includes notes and coins in circulation and also assets that are easily convertible to cash.

- M1 is the second group of the total money supply and this also includes M0. As of Nov 2012 it stands at RM 270.48 billion.

- M2 refers to the short term time or fixed deposits in banks plus M1. As of Nov 2012 the total is RM 1.32 trillion.

- M3 is the long term time or fixed deposits in banks plus M1 + M2. The total figure for M3 as of Nov 2012 stands at RM 1.34 trillion.

How much has our Money Supply Grown?

From the records above, our total Money Supply in January 2002 was RM 475 billion but it somehow managed to explode upwards to RM 1.34 trillion in November 2012. This represents an increase of about 268% for the period of 10 years. Whereas in the U.S during the same period from 2002 to 2012, the total Money Supply as measured by M2, grown from $ 5426.2 billion to $ 10408 billion. Period to period in percentage terms their Money Supply had only grown by 91.8% (10408-5426/5426). This can be shown by the following graph.

How indebted are our consumers?

Due to the improving economic conditions since the Global Financial Crisis in 2008, Malaysia’s GDP per capita has also been improving. Since 2002 the GDP/Capita has been rising from the low of US 3933.94 to US 5364.50. This can be shown by the following chart.

The rise in income has altered the consumer spending pattern. There is a macro shift in consumer spending from the traditional ‘needs based’ to a ‘wants based’. This means consumers are splurging on luxuries rather than necessities. Consumers are more willing to splurge on the latest hand phones, luxury handbags, ipads, fine dining, overseas travel and so on without ever giving it a thought. As a result of their addiction to spending they began to look for more avenues to raise cash like credit cards and personal loans and hence lead to an explosion in the consumer debt level. The following two charts shows the upward trend in their spending habits and also helped to explained the explosion of both the public and private sector debts.

The trend in consumer spending in Malaysia seems to be edging higher and higher with no end in sight. Thanks to the our Government’s earlier effort in promoting a consumer spending economy and at the same time relaxing the requirements to obtain loans so as to create a ‘loose money’ economy albeit there have been efforts to curb such practices recently . From the above chart consumer spending rose from RM 59300 million in January 2005 to RM 99812 million in September 2012 which represents a 68 % increase during this period. Government controlled medias have been telling folks that the economy is recovering and we are moving forward to better times. In reality our private sector is one of the most indebted in the region and their debt level can be considered ‘up to the eyeballs’.

The following chart is the household debt/ Disposable income of several countries and Malaysia is no doubt the leader among them.

Deteriorating External Sector

Malaysia’s receipts from exports are also down especially from the plantation sector following the decline of Global Commodity prices. As a result Malaysia’s external sector has also been affected. Palm oil price is at RM 2400 down from the high of RM 3820 in 2011 and similarly rubber prices remain low trading at less than RM 1000 compared to the high of RM 2160 in 2011. Hence there are less funds available for the Government to spend as a result it incurs deficits in its budget.

A budget deficit is a situation where the Government spends more than it received. From the above it seems that our Government had been running budget deficits since 1999 till today. To finance budget deficits normally there are three options available to the government and they are reducing public spending, increase taxation or borrowing. Given the current depressed economic scenario, increase taxation in the form of income and sales tax may place further burden to the already over stretched consumers in Malaysia.

Reducing public expenditure will be out of the question because it will entail slower economic growth and will be suicidal politically in the upcoming elections. The last option will be to borrow from abroad through issuing sovereign bonds to foreigners or to local institutions like EPF and so on. Thus this will further increase our debt burden and eventually will also increase our Government’s Debt/GDP. The problem with higher Debt/GDP is that interest will have to be paid and in this case to foreigners although their share represents about 25% of the total. This will represent a leakage in the economy and hence there will be less money circulating around our economy and will certainly affects the level of economic activity.

Nevertheless the main threat to the Malaysian economy is its debts although our Debt/GDP ratio has yet reached critical level. The lesson we must learn from the Global Financial Crisis during 2008 is that the majority of the countries that went bust had their Debt/GDP below 70%. Below is the Debt/GDP table of those countries that fell during the Crisis.

Table 1. Eurozone Countries Government Debt/GDP

| Column1 | Column2 | Column3 | Column4 | Column5 | Column6 |

| Country |

2008

|

2009

|

2010

|

2011

|

2012

|

| Cyprus |

58.8

|

48.9

|

58.5

|

61.3

|

71.1

|

| Iceland |

28.5

|

70.5

|

87.8

|

92.8

|

99.2

|

| Ireland |

25.1

|

44.5

|

64.9

|

92.2

|

106.4

|

| Portugal |

68.3

|

71.7

|

83.2

|

93.5

|

108.1

|

| Spain |

36.1

|

40.2

|

53.9

|

61.5

|

69.3

|

| Italy |

103.6

|

106.1

|

116.4

|

119.2

|

120.7

|

| Greece |

105.4

|

112.9

|

129.7

|

148.3

|

170.6

|

Source : Trading Economics

Any Risk in Defaulting?

As can be seen from the above, Malaysia cannot rest on its laurel that its Debt/GDP (52.6 %) is within manageable level. We must know that in normal market conditions risk and reward follows a linear path and that means higher risk will be compensated by higher return. However during extreme market movements (during a crash) risk and reward will follow a non-linear path meaning higher risk will not be compensated with higher return. In a Micro level an individual investor’s perfectly diversified portfolio that consists of many stocks and other derivatives will not be able to withstand extreme market movements. Say for example a 10 % drop in the FBMKLCI will normally result in a bigger decline in his portfolio and hence the P&L. Similarly on a Macro level Malaysia’s well diversified economy will not be spared either if one or two of its crucial macroeconomic metrics such as exchange rates (drop susceptibly) or interest rates (sky rocketing) reacted negatively to big market moves.

Further to that even if they try to pre-empt any extreme market movements by stress testing their portfolio or economy will not work. Evidence during the 2008 crisis proved that even though the banking industry tried to stress test their robustness with Quantitative Finance Risk Management tools such as VaR (Value at Risk) and CrashMetrics, it proved that is not sufficient to overcome to severity of the Crisis. Without bailouts from the authorities many of them will not be around by now.

In Summary

The other day I was reading some articles written by some of our local analysts saying that Malaysia will not face any risk of defaulting because of our strong fundamentals. Further to that they argued that we cannot compare Malaysia with Greece or Spain because they had a history of defaulting and Malaysia has never defaulted before. What denial !! But there is always the ‘first time’ and we must remember that the first cut is the deepest. Malaysia is able to escape much destruction on its economy during the Asian Financial Crisis back in 1998 because that Crisis was mostly confined within the South East Asian region albeit causing a few mini crashes here and there in Russia and South America. But what is coming soon is a different animal and it is on a Global scale. The fuse has already been lit by the recent Currency Wars.

No comments:

Post a Comment