There is always an assurance from our Government that the economy is doing fine, jobs are recovering, wages are going up and prices are under control. We are never been told what actually happened behind the scene or problems our economy is facing. Through propaganda by the media we are persuaded that everything is in the safe hands of the Government.

Even when economies around us are collapsing we are led to believe that our economy is the strongest, our share market is the best performing, our economic fundamentals are the best or in short we are the best managed economy. We are given the impression that our economy is ‘invincible and different from others’. But the problem is whether our economy is living up to what was preached by our Government. Is there a way to gauge the real performance of our economy other than relying on figures published by them?

To find out we need to know what make up the GDP and how much it has produced, traded, invested and consumed. The accumulation of all these numbers can be found in an economic indicator known as GDP or Gross Domestic Product. GDP can be defined simply as the total monetary value of all domestically produced goods and services in a given year.

The following is the chart of our country’s GDP growth from 2007 till 2013.

It can be seen that the GDP Growth rate in the latest quarter declined to 4.1% from 6.5% in the previous quarter. But by looking at the GDP figure in total doesn’t tell us anything. Other than 2009 during the Global Financial Crisis our country has recorded continuous positive GDP growth figures. Does this means that our economy is on the right track and our economic growth will go on perpetually? To find what causes the drop in the GDP Growth rate we need to look into the different components of the GDP.

Mathematically, the GDP can be defined with the following equation.

GDP = C + I + G + (X – M) where,

C = Private Consumption

I = Private Business Investment

G = Public or Government Expenditure

X = Exports

M = Imports

The GDP is made up of 5 components and hence our 1st Quarter GDP growth of 4.1% is a result of the combination of the above. To determine what causes our GDP growth to decline we need to look into each component separately. Below we present to you the five different components that make up the GDP.

Consumer Spending or C

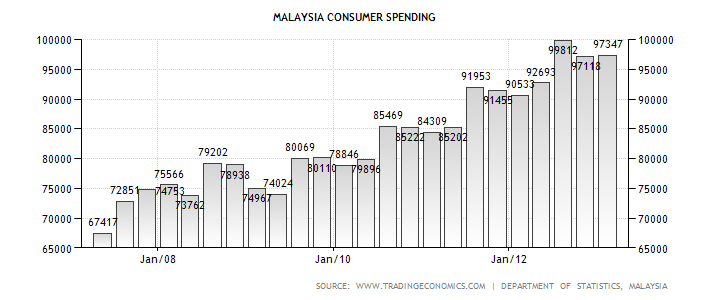

The first component is the consumer spending which can be defined as the total amount of money consumer spends on everyday goods and services. Being an economic indicator it helps provide a gauge on the financial health of consumers. Increased consumer spending indicates not only higher disposable income but also better expectation and confidence in the economy. The following chart displays the pattern of the Malaysian Consumer spending since 2007.

The consumer spending pattern seems to be on the rise since 2007. From the 2nd quarter of 2007 total consumer spending was indicated as RM 67.4 billion which then increased to RM 97.3 billion in the 1st quarter of 2013. This represents an increase of nearly 50% since 2007. Hence increased spending by consumers helped driving up the GDP value.

Private Business Investment or I

Private business investment is the second component of the GDP. From 2011 to 2012, Malaysia’s private business investments grew from RM 111.8 billion to RM 139.5 billion. This represents a 24.8% increase. The services sector commands the lion’s share with 72.4% of the total investments followed by the manufacturing sector at 25.3% while the remaining 2.3% went to the primary sector. In 2010 total private investment totaled RM 101.2 billion. The following chart displays the total private investments (domestic + foreign) as of 2009 to 2012.

Growth has been impressive since 2010 and last year grew the most. As of any indication of better times to come, Datuk Mustapha Mohd the Minister of International Trade states that in 2012 total approved investments was RM 162.4 billion. This was the highest amount as compared to RM 154.6 billion in 2011 and RM 105.6 billion in 2010.

Government Spending or G

The third component of the GDP is Government Spending. Government spending records the total spending of Federal, State and Municipal on goods and services. It covers the areas of education, defense, judiciary and other things that are related to the operation of the Government machinery. Government spending normally relates to the health of the economy. An increase in Government spending can be viewed as a positive sign for the economy because this is considered as expansionary policy.

From the above it can be seen that our Government embarked on an expansionary policy since 2005. Spending was relatively rising gradually until it went overdrive in year 2010 which we suspect coincides with the Government’s ETP (Economic Transformation Program).

Exports or X

Malaysia’s Exports seems to constrict for the month of April. It recorded a total of RM 55.8 billion in April as compared to RM 60 billion in March. On a Month to Month basis this represents a decline of almost 8%.

Imports or M

Malaysia’s import has been steadily on the rise since 2003 only to be interrupted by the Global Financial Crisis in 2008. From about RM 23 billion for the month of June 2003 it went up to about RM 55 billion for the month of April 2013. The mean for this period is RM 40 billion.

Our Finding

In summary we know that we have rising C, I and G and a declining X and is relatively unchanged M. On top of that we also have 14 quarters of non-stop GDP growth which gave an impression that this trend may last many more years. Even our politicians are very excited over the figures. The following are some quotes taken from a few politicians and reported by the local media.

“As a result of Malaysia's solid investment performance last year, the country exceeded the private investments target of RM127.9bil for 2012 by 9.1%,” International Trade and Industry Minister Datuk Seri Mustapa Mohamed said at the Investment Performance 2012 conference yesterday as reported by the Star, 28th February 2013

The government expects private investment in the Malaysian economy to expand from 22.2% in the first half of 2012 and likely grow 30% next year, says Minister in the Prime Minister's Department.

Tan Sri Nor Mohamed Yakcop said on Tuesday that sustaining higher growth in investment and consumption would be the main factors in consolidating the transition from externally driven to domestically driven growth. As reported in the Star, December 4, 2012

Seriously, I don’t know why they are so excited. Those are just collective numbers that are used to superficially describe the performance of the economy. To have a better idea on how the economy is doing you have to look deeper into the breakdown of the GDP figures.

Why need the breakdown?

Firstly, as you noticed out of the RM 139.5 billion in private investments 72.5 % went to the service sector and only 25.3% to the manufacturing sector. What it is telling us is that more investments are going into the services sector and less to the manufacturing sector. This also means that we are consuming more than we produce and hence structurally we are moving towards ‘a consumer economy’. The following chart by the World Bank on manufacturing as a percentage of GDP clearly shows the trend.

n

The importance of the manufacturing sector in our economy had been on the decline since 2002. This decline means that our economy is moving more towards the consumer side and less on the manufacturing side. This gain in the consumer sector is also mainly due to the current housing and consumer credit bubble which led to the boom in the construction, commercial banking and real estate sector. All of which are consumer related.

Secondly, moving from production to consumption means that there will be a rebalancing of wages. Since the manufacturing sector pays one of the highest salaries and when an economy moves toward services (healthcare, hospitality and retail for example) then obviously wages earned by workers will be lower. As a result it will have the effect of lowering the ratio of wages to Gross National Income.

In time their salary growth will not be able to catch up with inflation. And this will be one of the sources of consumer complaint on their salaries not being able to meet their daily expenses. More importantly Malaysia is going through a fundamental shift and that is moving from higher paying manufacturing jobs to lower paying services jobs.

Thirdly, the manufacturing sector is one avenue where our country earns foreign exchange which also helps to pay its imports. A drop in manufacturing activity means a drop in exports and hence less foreign exchange will be earned. The following chart shows Malaysia’s Balance of Trade figures as from 2011. The Balance of Trade records Malaysia’s monetary value of exports over imports over a period of time. A trade surplus means exports exceeds imports while a deficit means exports lagged imports.

Malaysia recorded a trade surplus of only RM 943 million in April 2013. This represents the lowest trade surplus in 18 years since 1995. Deterioration in the trade balance means that we are now consuming more than before. This will become serious when our trade surplus becomes deficits because by then we will be spending more than we receive.

The sooner we address this problem the better because when our trade balance finally turned negative then it will have a negative effect on the Ringgit as well. On top of this our Government is also concurrently running a budget deficit as shown by the following chart.

When we have two economic problems at the same time (Budget Deficit + Balance of Trade Deficit) we have a situation known as the ‘Twin Deficits’. Twin deficits are known to create havoc in an economy by accelerating the decline of a country’s currency and in this case Ringgit. This is because to finance our deficits we either have to increase taxes or borrow and if we borrow from overseas (normally denominated in US$) then the repayment of the principle and interest will be in foreign currency.

Lastly, to finance our consumption we can either borrow or finance it through savings or retained earnings. If our source of funds is derived from savings or retained earnings then it is not a problem because we are using resources from money earned from productivity. The problem is when we borrow to finance our private and public expenditure. As a result we are getting deeper and deeper into debt. The following is the chart for the total debts by the private and Government sector as of 2011.

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

438

|

18

|

456

|

Private

|

749

|

239

|

988

|

Given the GDP of RM 860 billion we can then proceed to calculate the Debt/GDP ratio of both the public and private sector. The table below summarizes the ratio of domestic and foreign debts held by the public and private sector.

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

51%

|

2%

|

53%

|

Private

|

87%

|

28%

|

115%

|

From the above we can conclude that at the present moment the private sector poses a greater risk to financial default than the public sector. The private sector is more exposed to any downside risk arising not only due to the size of the debt (87%) but also its exposure to foreign debt (28%). Large exposure to foreign debt is risk because it is subjected to movements in the foreign currency (US$ in this case).

The movement of the US dollar creates currency risk or what we called ‘Foreign Exchange Exposure’ in Treasury terms. Foreign Exchange Exposure refers to the risk associated to a decline in a country’s currency. Currency depreciation can have the effect of reducing a company’s profits due to increased cost in imports or loss due to the higher repayments of loans denominated in US dollar.

In Conclusion

From the above we can conclude that the reason for the GDP growth of 4.1% is the result of increased Consumer, Private Investment and Government spending. With declining exports, to maintain the GDP growth rate spending in Consumer, Private Investment or Government will have to increase. Since our GDP growth is fuelled by debt we will have to borrow more in the future. This is where the problem comes in.

Currently our public debt stands at 53% and almost near the debt ceiling (55%), any further borrowing will be capped. To facilitate further borrowing our Government will have to push the debt ceiling above the 55% threshold. How can this be done with the approval of Parliament?

A Black Swan Event?

One method is to create a ‘Black Swan’ event that is so mission critical that our Parliament will have no choice but to approve it. Similar approach can be seen during the implementation of the US$ 700 billion TARP program in the U.S during the Financial Crisis in 2008. Due to the artificially created sense of urgency, Congress is led to believe that by not approving the TARP program, the domino effect resulted from the meltdown of the U.S financial market will be disastrous. It will not only affect the financial markets in the U.S and Europe but the entire world. Hence Congress has no choice but to approve it even though the entire proposal is only a three page document.

No comments:

Post a Comment