The international capital flows from advanced Western Economies to Emerging Markets is not a new phenomenon. Since the abandonment of the Bretton Woods, there has been an upward trend in international capital movements. Reasons are being the growth of international trade and the liberalization of the trade and current accounts in the industrial economies, from the 1940s till the 1970s. Such capital flows are recorded in the Capital Account in the Balance of Payment of a country.

Emerging economies from Latin America such as Brazil, Mexico and Argentina are some of the pioneers in opening up their economies to international capital flows in the late 1970s. Latin America recorded about $8 billion in capital inflow in the late1980s surged to $24 billion in 1991. With the expansion of international trade, emerging market countries are beginning to open up their semi-open economies. Semi-open economies are characterized by artificial restrictions or barriers created to restrict the freedom of capital movement. Examples include the creation of taxes, quotas, licenses and so on.

The success of the Latin American countries in attracting capital inflows from Western countries also prompted many Asian Countries to follow suit. The first wave of capital inflow from the West occurred during 1988-1989. During this period the capital inflows, many Asian countries recorded capital account surplus and some to the tune of 2.5% to GDP. As a result of this, there is a marked increase in the international reserves held by those countries. To capitalize on the growth of international trade, many emerging market countries began to liberalize both their trade and capital markets. Tariffs and quotas are either reduced or eliminated; licenses are relaxed so as to promote a more open economy.

Thus, this also led to many of them abandoning their traditional protectionist model for economic growth and embracing a more open economy by liberalizing their trade or current account. Instead of promoting the import substitution and infant industry development strategy they now encourage Foreign Direct Investment inflow as their next growth strategy. Other reasons for opening up their economy are to facilitate capital inflows of cheap funds to fast track their economic development and also the urge to compete with their neighbors to attract more funds.

What causes capital inflow?

There are many reasons associated with the recent international capital flows and most are attributed to both push and pull factors. Since the last Global Financial crisis in 2008, it left many economies especially from the West in tatters. Their economies plunged into recessions and as a result there is a constriction of credit. To prevent their economies from plunging into a severe recession, funds are injected into the economy through quantitative easing. Further to that, interest rates are lowered to almost zero percent so as to promote borrowing to revive economic activity.

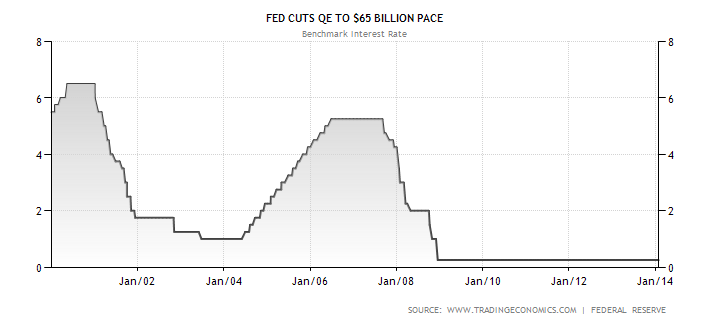

The above chart shows the movement of the U.S interest rate and as can be seen rates are lowered twice. The first downward move of the interest occurred in the year 2000 to counter the recession caused by the Y2K. The second and most recent one was during the financial crisis in 2009 where the interest rate was lowered from more than 5% to 0.25% and prevailed till now.

This drop in interest rate provided an impetus for the Emerging Markets to repatriate some of their funds from Western countries and at the same time increased their borrowings. Further to that the sharp drop in the interest rate also helped improve the solvency of many Emerging Market debtors. This is due to the lower debt service obligation on external debts held by emerging market economies.

Another determinant for the increased capital inflow into Emerging Markets is the eroding trade balance positions of many Emerging Economies. Thus a deteriorating trade balance will eventually lead to a worsening current account deficit. This process or linkage is known as the Harberger-Laursen-Metzler effect. Hence, the need to finance this deficit through capital inflows also contributed to the relaxation of rules governing capital inflows.

This effect can be shown by the following terms of trade and current account graphs in the U.S from 1990 to 2014. As can be seen the U.S Current Account worsens as the terms of trade deteriorates.

This also correspond to the increased of private capital outflow from the U.S Capital Account due to the deteriorating Balance of Payment in the U.S. There has been an increase in the amount of investments by U.S mutual and institutional funds in overseas securities. This may be due to the need for diversification to reduce risk and also to take advantage of higher yields in Emerging Markets. The following is the net long term flows chart in the U.S as from 1990 to 2013. This chart tracks the Treasury, securities, Corporate bonds and equities flow in and out of the United States. As can be seen there has been a steady outflow of funds since the 1990s except for the year 2008 and as recently as 2013.

Among the pull factors that encourage capital inflows into recipient countries are the availability of cheap funds to fast-track their economic development cycle and financing their current account deficits. Nations that are experiencing shortage of capital to invest can take advantage of borrowed money from capital inflow to speed up their economic development.

This can be explained using the Harrod-Domar growth model which was developed in the late 1940s by two economists namely Roy Harrod and Evsey Domar. According to the growth model, the key ingredients are the national savings ratio (or S) and capital output ratio or ICOR (Incremental Capital Output Ratio or K). For example, to calculate the rate of growth of an economy with a savings rate of 30% and a capital output ratio of 5, we then apply the following formula.

Economic Growth = S/K or 30/5 = 6% per annum.

Thus, a country’s economic growth can be enhanced by either increasing its savings from National Income which will be redirected towards investment or decreasing the Capital to Output ratio by way of increasing investment in technology to reduce the K ratio. This is because by applying technology, less capital will be needed to produce one unit of output. As a result, it gained popularity and country like China and India has incorporated it into their 5 year Economic Plan.

As can be seen, capital deficient countries can enhance their Investments through borrowed funds by way of liberalizing their capital account. By removing barriers to capital inflows, these countries will be able to achieve higher economic growth in a shorter time span through higher investment.

This objective is only achievable if the debtor countries spend their borrowed capital wisely. Investing wisely can increase their productive capacity and hence will generate future returns to pay off the loans. Another condition to justify capital inflow is to make sure that the funds are not directed towards portfolio or personal consumption so as to prevent future complications in debt servicing. Thus, this can explain why some developing countries like China, South Korea, Taiwan and Singapore has done relatively well and able to pay the higher cost of increasing interest rates. Other countries especially from the South America and African nations could not and thus consistently plunge into financial crisis.

Problems of Capital Inflow

In theory, capital inflow can be viewed as having a positive effect on an economy like helping it to fast track its economic growth. However along the way, it also helped create some unwanted externalities. Some of them include the following.

First, if the capital inflow goes to finance consumption and not investment then it is not going to generate any additional future output to service the debts. The increased in private consumption also led to a spend thrift culture where everyone tends to live beyond their means. I shall present Malaysia as a case study. The following is the graph of Malaysia’s Consumer Spending.

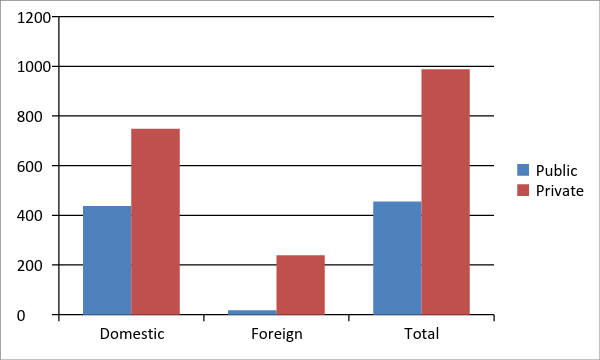

Malaysia’s Consumer spending increased to RM108046 million in the 3rd Quarter of 2013 as compared to RM99171 million in the 2nd Quarter or a 8.95% rise. As a result many are resorted to borrowed funds either through personal loans or credit cards to finance their consumption. As a result the debts held by the private sector ballooned to 115% to GDP. The following is the graph for Malaysia’s private and public debt as of 2012.

Total Private and Public Debts

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

438

|

18

|

456

|

Private

|

749

|

239

|

988

|

Private and Public Debts to GDP

Debt

|

Domestic

|

Foreign

|

Total

|

Public

|

51%

|

2%

|

53%

|

Private

|

87%

|

28%

|

115%

|

As can be seen from above, our private debts to GDP has reached an unsustainable level of 115% to GDP. It must be understood that although most of our debts are in private hands, if it is defaulted then our Government will be compelled to transform those defaulted debts into sovereign debts to prevent any systemic collapse in our banking system. As observed during the 1997-1998 Financial Crisis, our Government has created special entities like the Danaharta and Danamodal to absorb the non-performing loans from the banking sector. At the end of the day the losers are the tax payers.

Second, it will lead to ASSET speculation. It should be understood that most of the capital inflow into emerging markets are short term in nature also known as ‘hot money’. That means they are mostly portfolio investment rather than foreign direct investments. As a result more and more money are poured into the stock market and real estate sector. In time as a result of continuous money flowing into these sectors, it became increasingly speculative and resulted in sky-rocketing prices. Below is the chart for Malaysia’s stock market performance before and after the 2008 Crisis.

Third, the influx of capital from abroad also helped to increase the domestic money supply and also appreciates the Ringgit. Appreciation of the Ringgit reduces our exports as it made them uncompetitive and raises our imports as the same time. This will result in the deterioration of our Current Account and thus a fall in our GDP growth. The following graphs are the Exchange rate (USD/MYR) and Current Account of Malaysia.

The rise of the Ringgit coupled with our increase in our domestic prices has the effect of deteriorating our terms of trade. As a result our Current Account surplus began to deteriorate because our exports are falling while our imports are rising and at the same time our GDP growth fell from 10% in 2009 to about 5% in 2013. It is clearly shown that as from 2008, our Current Account deteriorates sharply from about RM 40 billion to less than RM 10 billion. Thus it can be argued that sustained capital inflow only promote economic growth in the short term. The short term gain will be cancel off in the long run by the increased inflation rate and Current Account deterioration.

Fourth, during the Latin American crisis in the 1980s and the Asian Financial Crisis in 1997, it demonstrated that capital inflow can reverse course at terrifying speed. This is because the expected rate of return on assets across countries is the main determinant on whether investors will move their capital overseas. If they expect the future return on their capital to deteriorate they will not hesitate to pull off their funds and invest elsewhere. Unknown to many investors, those who perform cross border investments are confronted by a myriad amount of risk. The following are the different type of risks an international investor will face.

- Inflation Risk

- Re-Investment Risk

- Liquidity Risk

- Loss of Capital Risk

- Credit Risk

- Marketability Risk

- Interest Rate Risk

- Call Risk

- Event Risk

- Pre-payment Risk

- Foreign Exchange Exposure Risk

Take the Foreign Exchange Exposure risk for instance. The current Currency meltdown in the Emerging Markets is causing large losses to foreign investors. Whatever they have made for the past years are not enough to cover their foreign exchange losses. The capital flight from emerging markets is further heightened after the Fed is considering extending its tapering activity. It might reduce the purchase of bonds by a further $10 billion to $65 billion a month, which will result in interest rates hike soon.

Dollar Carry Trade

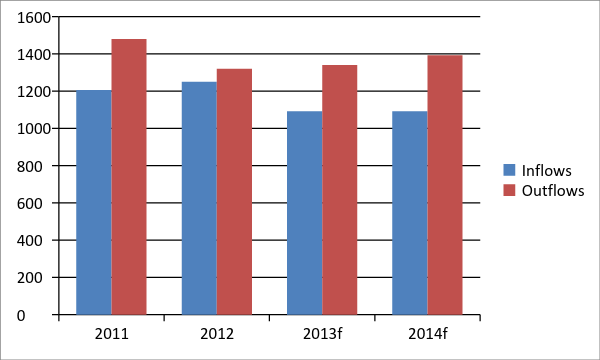

It is of knowledge that a large percentage of the recent capital inflows are carry trade in nature. A Carry trade is a strategy where investors make their money by arbitraging yield differentials between countries. In the case of Dollar Carry trade, investors borrowed money from the U.S where the interest rate is at 0.25% and invest in say Malaysia where its 10 year bond yields 4.17%. Hence the investor will be able to pocket the difference as long as the U.S interest rate doesn’t rise or the Malaysian Ringgit doesn’t depreciate. Such a trade is very risky as they are highly leveraged meaning a small downturn in the exchange rate will wipe out the investor if he is not hedged. In fact there has been a steady net outflow of funds from emerging markets since 2011 as shown by the graph below.

Source : IIF (institute of international finance) f = forecast

However in recent months, the capital flight from emerging markets has heightened tremendously due to the collapse of their currencies. Hence the larger the carry trade the larger will be the capital flight and the bigger will be the depreciation of the receiving country currency. To insulate against further capital flight, some countries like Turkey, India, South Africa, Brazil and India resorted to raising their interest rates.

However, Interest Rate targeting will not work in this instance because firstly, it will create distortions in the demand and supply of funds. Artificially varying the interest rates will create wrong signals to the flow of funds. For example Central Bankers will constrict the money supply in times of weakness as in the case currently and expand when economic conditions are booming. As for an example, from the graph above we know that there is a net capital outflow from emerging markets since 2011. But how come the interest rates stayed low during that period and not increased to counter the outflow?

Secondly, it will increase the future debt obligation. Both the public and private will be subjected to higher interest payments in future. What happen when interest rates soared to unsustainable level as what is happening in Turkey. The Turkish Central Bank has recently raised the interest rate by 425 basis points (4.25%) to 12%. What will be the repercussions?

It will immediately cause a steep fall in the demand for credit assuming all things equal. A steep fall in the demand for credit will also cause a steep fall in economic activity which eventually will result in a steep recession. Other things being equal, will a fall in the demand in credit help push the interest rates downward again?

But wouldn’t a drop in interest rates cause another round of capital flight? Unwillingly, the authorities will have no choice but to maintain a high interest rate regime, but for long? Domestic private consumers and businesses will be suffering and find it very difficult to meet increasing interest payments. If the Turkish Central Bank decides to lower interest rates sometime later, aren’t it getting back to where it started (with low interest rates)? This linkage can be illustrated below.

(↓interest rate) → (+ Credit Demand) → (↑ interest rate) → (- Credit Demand)

In other words, the Turkish Central Bank is stuck in the Credit Demand vicious cycle and is unable to find its way out. It will have to look for an alternative solution such as implementing capital controls or maybe develop a stabilization strategy such as a pseudo currency revaluation.

Alternatively another strategy can be conceived by applying the game theory to economics which might help it see through and anticipate the opponent’s (foreign investors) next move. If the situation calls for a zero sum game then there will be losers (actors in the domestic economy) and winners (foreign investors). Next the Central Bank will need to look for dominant strategies. If it is not available then the next option will be to look for dominated strategies. If neither is available then the final option will be to look for an equilibrium strategy also known as the Nash equilibrium. To out-manoeuvre the opponents (foreign investors) the authorities have to look at the different aspects of cooperative and non-cooperative game theory strategies.

No comments:

Post a Comment