It is a known fact that one of the hottest topics of discussion among Malaysians for past few months has been our Ringgit. Thanks to our current economic debacle, it helped raised our awareness of our economic situation. Despite the numerous propaganda engaged by our authorities assuring us of our economy’s resilience, it still failed to alleviate our suspicions. Cliché like high level of international reserves, current account surplus, solid domestic financial system and Ringgit reflecting our economic fundamentals were often used. Is it true that our economy is really that resilient and solid? This article aims to look into the current state of affairs of the Malaysian economy and also how it affects the Ringgit.

To begin with we shall look at the macro side of things. Unfortunately, all is not well with the current state of affairs in the world economy. A combination of falling oil and other commodity prices, strong dollar, stock market rout in China and record level of debts around the world has led the IMF to downgrade this year’s global economic growth to 3.2%. This represents the lowest growth rate since 2009. Slower growth means a smaller economic pie to share among all nations.

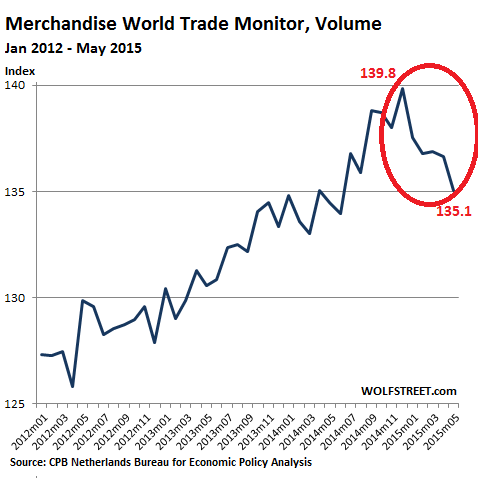

According to the CPB Netherlands Bureau of Economic Policy Analysis, the Merchandise World Trade Monitor index which covers the global import and export trade provides a good indication of the global economy. World Trade shrank 1.2% in May from the previous month. The index felled from 139.8 to 135.1 points or a 4.7 points drop. This is the sharpest and longest drop since the Global Financial Crisis in 2008. This can be shown graphically below.

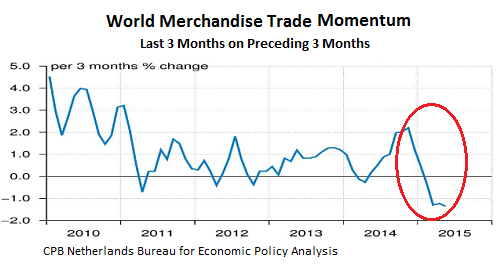

To lower the volatility of the monthly analysis, CPM has a 3 monthly Trade momentum index. According to them the World Trade momentum had dipped to below -1%. This represents the slowest pace since the last Global Financial Crisis in 2009. Here’s the graph.

It also reported that the decline was widespread, import and export volumes declined in most regions and countries and in both advanced and emerging economies.

Another indicator that shows the global economy is in bad shape is the performance of commodity prices. When commodity prices decline sharply, it means that either there is an over-supply or weakening demand. A good indicator is the S& P GSCI or Goldman Sachs Commodity Index. It comprises of 24 major commodities from all sectors and thus provided a good indication of the overall performance of the commodity space. Below is the latest S & P GSCI chart.

It can be seen from the chart above the index has crashed to its lowest point since the last Global Financial Crisis in 2008.

In view of this global economic malaise nations began to increase their competitiveness through competitive currency devaluation (beggar thy neighbor policy) to gain market share. The U.S started the ball rolling when it instituted the QE program in Jan 2009. As a result, the Federal Reserve balance sheet expanded and caused the dollar to decline. This helped to improve the terms of trade with its trading partners.

This led to other countries to join in the fray on competitive currency devaluation. Japan is next by devaluating its Yen to reflate its economy and so does Europe. As of July this year, there are more than 30 countries in one way or another joined the currency war. As a result this put an upward pressure on the Dollar and it has since appreciated more than 30%. The following USD index chart shows the movement of the USD since 2008.

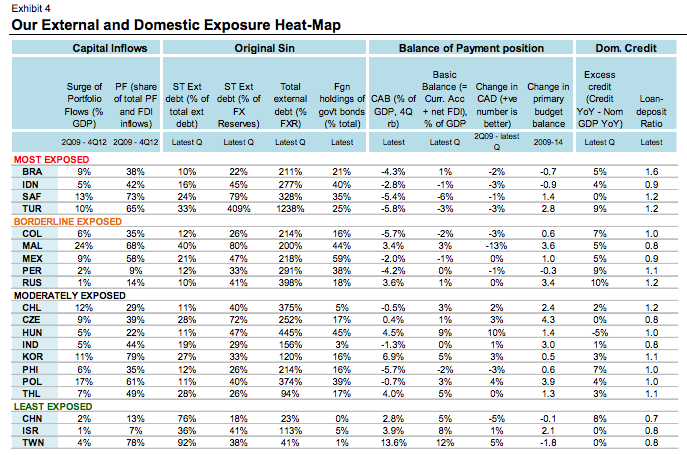

Malaysia can be considered as one of the most vulnerable economy that is susceptible to both internal and external exposure. This means our economy is elastic to sudden capital outflow which can cause detrimental damage to our economy. Below I present the External and Domestic Exposure Heat Map by Morgan Stanley.

As can be seen from above between 2nd Quarter of 2009 and 4th Quarter of 2012 Malaysia recorded the highest surge in Portfolio flows, 24% to be exact. On top of that out of the total FDI inflows between that timeframe 68% are of Portfolio inflows. That means most of them are short term capital inflow while the 32% went into long term investments such as building factories or expanding existing facilities. Short term capital inflows can turned outflow in a heartbeat whereas long term capital inflows are more difficult to reverse as their investments ‘are stuck on the ground’.

The second point to note is that 40% of our external debt is short term in nature meaning they can reverse flow at any moment.

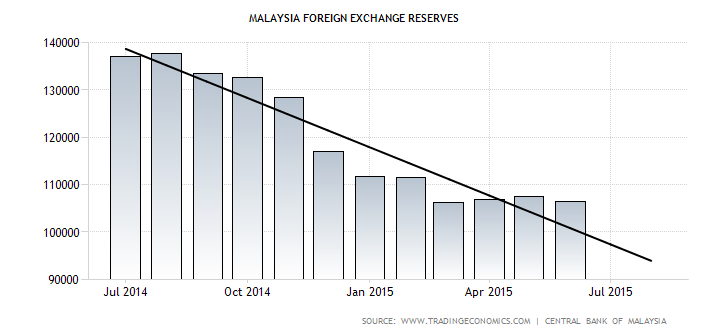

As of March this year our external debt ballooned to RM 768 billion from RM 744 billion in December 2014. Since our foreign exchange reserves have dropped to USD 96.7 billion in July the ratio of our External Debt/FX Reserve now exceeded 200%.

With 40% of our debt is short term in nature, thus it can be said that there are about RM 300 billion in short term debt that are vulnerable to reverse flow. The question is, say if only 50% (RM 150 billion) of the short term funds decided to rush for the exit can Bank Negara counter this move? What chance are we able to defend the Ringgit with just USD 96.7 billion left in the Foreign Exchange Reserves? Please do not forget that from the table above, our Short Term Debt/ FX Reserve stands at 80% which is the second highest after Turkey. Turkey is the biggest Emerging Market economy to succumb to the current financial crisis. The Turkish Lira has dropped to the all-time low to 2.81 against the USD amid political crisis in the country. It has dropped 60% against the USD since 2008. See the chart below.

The Turkish Central Bank has tried to direct intervene in the forex market but failed leaving its reserves with just $35 billion. Similar to Malaysia, Turkey also ran budget deficit for years and had to rely on external financing. Further devaluation meant it will be even harder for them to pay off their dollar debt.

The Turkish political crisis also led the government led by Mr Erdogan to implement erratic policies in order to tighten his grip on his opponents. This includes political pressure on the central bank to intervene and purging of prosecutors, judges and whistleblowers.

The third point to note from the table above is that foreign holding of Malaysian bonds stands at 44%. This is the third largest after Hungary and Mexico. Malaysia also has one of the largest LCY (Local Currency) bonds in Asia after Japan and Korea. It is close to 100% to GDP or about RM 1 trillion. Below is the breakdown.

Who are on the losing side when they invest in local currency bonds especially when the Ringgit is depreciating? Well foreign bond holders will be on the losing side. This is because when they exit the bond market they will be getting less USD when they convert their Ringgit to the USD. To ensure the bondholders do not exit at the same time, interest rates will have to rise as a form of compensation. The price of bonds is inversely related to the yield. When happens when foreign investors start selling? The price of bond will go down and the yield will go up. The nightmare every country has is a ‘bond run’. This happens when every bond holder starts rushing for the exit and this will cause a selloff in the bond market which in turn caused interest rates to rise substantially.

By now it is a known fact that our Ringgit has been on the downtrend since last year only recuperating some losses beginning of this year. However the slide begins again and it is likely that we have yet to see the worse. The following chart denotes the exchange rate between the USD and our Ringgit. As can be seen it is now fast approaching the 4.00 psychological level that was set back in 1998 during the Asian Financial Crisis.

USD/MYR chart

Bank Negara Malaysia has also been involved in the intervention of the Malaysian Ringgit through open market operations by selling the Dollar to prevent further slide of the Ringgit. What supposed to be an orderly or controlled devaluation of the Ringgit by Bank Negara became unmanageable especially after May this year. This also coincides with the onset of our political crisis. This can be shown by the sharp decline of our Foreign Exchange Reserves in the following chart.

Our Foreign Exchange Reserves peaked at $155 billion in August 2011 but has since been declining rapidly. In July 2015, our Foreign Reserves declined to $96.7 billion, a drop of $58 billion from the peak. We have been recording Balance of Payment surplus for the past many years and by right the excess Dollars should be added into the Foreign Exchange Reserves. Yet we are seeing dwindling reserves and one explanation is some of the reserves are being used for open market operations to support the Ringgit. This can be further supported by the expansi

on of Bank Negara’s Balance Sheet as shown below.

Wrapping Up

In wrapping up, from above we know that Malaysia is now one of the most vulnerable countries subjected to capital outflows. This is mainly due to our large exposure to short term debts. With Short Term Debt/ FX Reserve at 80% and Short Term Debt/ Total Debt at 40% and dwindling foreign reserves. In short, we are running on wafer thin safety margin. With Turkey, Russia and Brazil already admitted to defeat in the Currency war, Malaysia’s effort to prop up the Ringgit by selling the Dollar will end up a loser game. Brazil has since gone to the next level of protectionism by enlisting embargo and tariffs. If our political crisis is not solved within a shortest period of time, our economy, exchange rate and stock market will risk a rapid decline soon.

In tradespeak, this amounts to terminal velocity. Terminal velocity decline in any asset price is due to the animal spirits (ideas and feelings) among us. As a normal investor we are all prone to the loss aversion which is a psychological reaction to the market behavior. This refers to our tendency to avoid losses rather than acquiring gains. In normal conditions investors tend to buy when stock price increases and sell when stock price decreases. This will have the tendency to cause a price change in one direction. This will cause a feedback loop where selling begets selling which is also known as price-to-price feedback. This can cause a drastic drop in the asset price as it will lead to panic selling. Eventually it will cause a crash in the asset price. This can happen to our Ringgit when foreign investors start dumping our Bonds and Stocks as it is happening now.

65 comments:

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+1%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+1%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly

renewable leased bank instruments. We work directly with issuing bank lease providers, this Instrument can be monetized on your behalf for 100% funding: For further details contact us with the below information.

Contact Name: SILKE CHRISTA CERVENY

Email: inquiry.dcifinancial@gmail.com

skype : inquiry.dcifinancial

We offer fresh cut bank instrument for lease, such as BG, SBLC,Lease and Purchase Instruments can be obtained at minimal expense to the borrower compared to other banking options. This offer is opened to both individuals and corporate bodies.

DESCRIPTION OF INSTRUMENTS

1. Instrument: Funds backed Bank Guarantee(BG) ICC-600

2. Currency : USD/EURO

3. Age of Issue: Fresh Cut

4. Term: One year and One day

5. Contract Amount: United State Dollars/Euros (Buyers Face Value)

6. Price : Buy:32%+1, Lease: 4%+2

7. Subsequent tranches: To be mutually agreed between both parties

8. Issuing Bank: Top RATED world banks like HSBC, Barclays, ING Dutch Bank, Llyods e.t.c

9. Delivery Term: Pre advise MT199 or MT799 first. Followed By SWIFT MT760

10. Payment Term: MT799 & Settlement via MT103

11. Hard Copy: By Bank Bonded Courier

Interested Agents,Brokers, Investors and Individual proposing international project funding should contact us for directives.We will be glad to share our working procedures with you upon request

Name:Ardan Clooney

Email:brandfinance33@gmail.com

Are you looking for financing source such as Bank Guarantee (BG) and Standby Letter Of Credit (SBLC)?

I am a direct mandate to a Financial Institution who is also known as private lender specialized in the Lease of Bank / Financial Instruments in the form of Bank Guarantees (BG), Standby Letter of Credit (SBLC), Documentary Letter of Credit (DLC), Letter of Credit (LC), Performance Bonds (PB);

Whether you are new starting up, medium or large establishment that needs a financial solution to fund/get your project started or an established business looking for extra CAPITAL to expand your operations, our company renders all the credible and trusted bank guarantee providers who are willing to fund and give financing solutions that suits your specific business needs.

We help/assist you secure SBLC and bank guarantee (BG) for your trade and investment from world ranked Banks such as; HSBC, Barclays Deutsche Bank Frankfurt, and Any A rated Bank in Europe e.t.c

DESCRIPTION OF INSTRUMENT:

(1) Instrument: Bank Guarantee {BG} /StandBy Letter of Credit.{SBLC} (Appendix A).

(2) Total Face Value: Eur/USD 1M{Minimum} to Eur/USD 10B{Maximum}.

(3) Issuing Bank: HSBC Bank London, Credit Suisse and Deutsche Bank Frankfurt.

(4) Age: One Year and One Day.

(5) Leasing Price: 4% of Face Value plus 2% commission.

(6) Delivery: bank to bank SWIFT MT-799 and/or MT-760.

(7) Payment: MT103 (TT/WT).

(8) Hard Copy: Bonded Courier Service.

RWA ready to close leasing with any interested client in few banking days

We will be glad to share our working procedures with you upon request to help us proceed towards closing deals effectively.

For further inquiry contact

Email : Saban.financialbg@gmail.com

Skype : Saban.financialbg

A nice and informative post!

Umrah Packages

Finding a genuine provider of financial instrument is very challenging but we are certified Financial Instrument providers in United Kingdom. Presently, we only focus on BG/SBLC for Lease and Sale transactions. However, our Lease BG/SBLC is 6+2% and Sale at 40+2%. Should you find this interesting and acceptable? Kindly, contact us and we shall review and respond with draft Contract/MOU within 48hrs maximum. Please request for full procedure details if interested. For further inquiry contact: lewis mason Skype: lewis.mason10 Email:lewis3932@gmail.com

Are you looking for financing source like bank guarantee and sblc? Whether you are a new startup, medium or large establishment that needs a financial solution to fund/get your project off the ground or an established business looking for extra capital to expand your operations, our company renders all the credible and trusted bank guarantee provider who are willing to fund and give financing solutions that suits your specific business needs.

We help you secure bank guarantee for your trade and investment from world ranked Banks.

LEASING FEE = 4% + 2%: MINIMUM and MAXIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M-20B

PURCHASING PRICE = 32% + 2% MINIMUM and MAXIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M-20B

Please contact for advise with full details for our financial solution services.

Michael David.

Contact Mail : riversfinancegroupplc@gmail.com

We are Ireland based major/Direct providers of Fresh Cut BG, SBLC, POF, MTN, Bonds and CDs and this financial instruments are specifically for lease and sale.We are one of the leading Financial instrument providers with offices all over Europe.

we always deliver on time and precision as Set forth in the agreement. You are at liberty to engage our leased facilities into trade programs, project financing, Credit line enhancement, Corporate Loans (Business Start-up Loans or Business Expansion Loans), Equipment Procurement Loans (Industrial Equipment, Air crafts, Ships, etc.) as well as other financial instruments issued from AAA Rated bank such as HSBC Bank Hong Kong, HSBC Bank London, Deutsche Bank AG Frankfurt, Barclays Bank , Standard Chartered Bank and others on lease at the lowest available rates depending on the face value of the instrument needed, Our Terms and Conditions are reasonable.

DESCRIPTION OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG)/SBLC (Appendix A)

2. Total Face Value: 10M MIN to 50B MAX USD or Euro

3. Issuing Bank: HSBC, Deutsche Bank Frankfurt, UBS or any Top 25 .

4. Age: One Year, One Day

5. Leasing Price: 4+ 1%

6. Sale Price: 32+2%

7. Delivery by SWIFT .

8. Payment: MT103-23

9. Hard Copy: Bonded Courier within 7 banking days.

If you have need for Corporate loans, International project funding, etc. or if you have a client that requires funding for his project or business, We are also affiliated with lenders who specialize on funding against financial instruments, such as BG, SBLC, POF or MTN, we fund 100% of the face value of the financial instrument.

Inquiries from agents/ brokers/ intermediaries are also welcomed; do get back to us if you are interested in any of our services and for quality service.

Name : Robert O'Sullivan

E-mail : osullivanr225@gmail.com

Skype id : osullivanr225@gmail.com

Are you having one or two difficulties from other financial instrument lender? i want you to take a chance with us you will never regret your partnership with our firm.We can deliver Financial service/instruments(BG/SBLC/MTN/DLC/LC) at affordable price to our customers in other to derive maximum utility. We understand that finding the right company to provide financial instrument is not easy. We are certified financial company that delivers banking instrument for lease which we adhere to our terms and condition. Over 96% of our clients are satisfied with our work whether it is business or financial service.

Once transaction is in progress, we ensure we keep you posted on the progress of your paper. We also get you connected to the provider for personalized service. Instead of stressing yourself out looking for financial instrument or company why not let professional like us deliver financial instrument to you within the time frame required by you.

For further details contact us with the below information....

Clifford David

Email: optivofinanceplc@gmail.com

We can deliver financial service/instrument(BG/SBLC/MTN/DLC/LC) at affordable price to our customers in other to derive maximum utility. We understand that finding the right company to provide financial instrument is not easy. We are certified financial company that delivers banking instrument for lease which we adhere to our terms and condition.

Lease Fee : 3+2

Purchase Fee : 32+2

Over 96% of our clients are satisfied with our work whether it is business or financial service. Once transaction is in progress, we ensure we keep you posted on the progress of your paper. We also get you connected to the provider for personalized service. Instead of stressing yourself out looking for financial instrument or company why not let professional like us deliver financial instrument to you within the time frame required by you.

For further details contact us with the below information....

Clifford David

Email: optivofinanceplc@gmail.com

I am a direct Mandate to a genuinely renowned Investment Finance Company and providers offering Financial Instruments such as BG/SBLC/MTN/LC/DLC on Lease and Sale at the best rates and with the most feasible procedures. Instruments offered can be put in all forms of trade and can be monetized or discounted for direct funding. We offer certifiable and verifiable bank instruments via Swift Transmission from a genuine provider capable of taking up time bound transactions.

With our financial/bank instrument you can establish line of credit with your bank and/or secure loan for your projects in which our bank instrument will serve collateral in your bank to fund your project.

We deliver with time and precision as set forth in the agreement. Our terms and Conditions are reasonable and we work directly with issuing bank lease providers, this instrument can be monetized on your behalf for upto 100% funding. Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

All relevant business information will be provided upon request.

BROKERS ARE WELCOME & 100% PROTECTED!!!

Kindly contact for genuine inquiries and I can provide you with the needed information.

Contact : fred stones

Email: premiumfinanceserviceltd@gmail.com

Skype: fredforrealasurance403

We can deliver financial service/instrument(BG/SBLC/MTN/DLC/LC) at affordable price to our customers in other to derive maximum utility. We understand that finding the right company to provide financial instrument is not easy. We are certified financial company that delivers banking instrument for lease which we adhere to our terms and condition.

Lease Fee : 3+2

Purchase Fee : 32+2

Over 96% of our clients are satisfied with our work whether it is business or financial service. Once transaction is in progress, we ensure we keep you posted on the progress of your paper. We also get you connected to the provider for personalized service. Instead of stressing yourself out looking for financial instrument or company why not let professional like us deliver financial instrument to you within the time frame required by you.

For further details contact us with the below information....

Clifford David

Email: optivofinanceplc@gmail.com

Thanks for sharing this. wonderful bLog! its interesting. much gratitude to you for sharing..

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly

renewable leased bank instruments. We work directly with issuing bank lease providers, this Instrument can be monetized on your behalf for 100% funding: For further details contact us with the below information.

Contact name: Azra Ishaque

Email : lintel.financialservicesplc@gmail.com

Skype : lintel.financialservicesplc

We are project funder as well as financial lender. We have BG/SBLC specifically for BUY/LEASE at a leasing price of 4%+1% of face value top 25 AA rated Banks. We also secure funding to facilitate and enhance your business and projects. Also We are into the provision of short term and long term business/personal loans for both small and large scale business funds.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+1%

FOR PURCHASE OF BG/SBLC

PRICE = 32%+1%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Intermediaries/Consultants/Brokers are welcome to bring their clients with healthy commissions paid and are 100% protected.

We will be glad to share our working procedures/DOA with you upon request to help us proceed towards closing deals effectively.

For further inquiry contact Us Via :

Email:- inquiry.emeraldfinanceltd@gmail.com

Skype :- emeraldfinanceltd@gmail.com

My Brothers and Sister all over the world, I am Mrs Boo Wheat from Canada ; i was in need of loan some month ago. i needed a loan to open my restaurant and bar, when one of my long time business partner introduce me to this good and trustful loan lender DR PURVA PIUS that help me out with a loan, and is interest rate is very low , thank God today. I am now a successful business woman, and I became useful. In the life of others, I now hold a restaurant and bar. And about 30 workers, thank GOD for my life I am leaving well today a happy father with three kids, thanks to you DR PURVA PIUS Now I can take care of my lovely family, i can now pay my bill. I am now the bread winner of my family. If you are look for a trustful and reliable loan leader. You can Email him via,mail (urgentloan22@gmail.com) Please tell him Mrs Boo Wheat from Canada introduce you to him. THANKS

IQ FINANCE PLC provides a full financial planning service to both the commercial and domestic markets. At IQ FINANCE PLC we believe that financial planning is about two things: creating wealth and protecting wealth. These two objectives are at the heart of everything we do. And, as a member of IQ FINANCE Services, we give you a small-company service but with a large-company set up – the best of both worlds.

You are at liberty to engage our leased facilities into trade programs as well as in signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges and any other turnkey project(s) etc. Our terms and Conditions are reasonable.

Leasing Price : 4%+2%

Buying Price: 32%+2%

Contact us for more details on our terms and procedure of transaction.

WALSH SMITH, ROBERT

email : info.iqfinanceplc@gmail.com

skype: cpt_young1

Contact: Gary Snyder

Skype ID: readysteadyfinancesltd

Email: readysteadyfinancesltd@gmail.com

Tele: +447031912976

We offer certified and verifiable bank instruments through Swift Transmissions from original providers

capable of taking over time-bound transactions.

PARTICULAR INSTRUMENTS BANK

Instrument: Fully Cash / Bank Guarantee (Standard ICC format)

Age: Fresh Cut

Interest Rate: ZeroCoupon

Duration: One (1) year and One (1) day

Currency: USD / Euro

Menu Bank: WEB Top

Amount: As Suggested by Beneficiaries

Initial Deposit: Applies to Instrument Value Required

Invoice Price: Four (4%) Percent of Face Value minus Paid Initial Payment

Intermediate Fee: One Percent (1%) of the Face Value is paid by the Beneficiary

Tranche: As per the agreed tranche schedule

Shipping: Swift MT799 / MT760

Payment: Swift MT103 (Wire Transfer)

Dear Sir/Madam.

we provide leasing of instruments such as; Bank Guarantees (BGs), Medium Terms Notes (MTNs), Standby Letter of Credits (SBLCs), Letter of Credits (LC), Bank draft Project Finance and Funding. We also provide Bank account opening services with United States, United Kingdom, China, Hong Kong, Spain, Switzerland, Poland, Belgium, Hungary, Japan, Banks.

we will have your projects funded such as Real Estate Development, Aviation Service, Agriculture Finance, Petroleum Importation, Telecommunication, construction of Dams or Bridges and all kind of projects, we fund 100% of the face value of the financial instrument.

Currently, we are looking for brokers and financial consultants that will work with us as our agents and representative.

If in need of our services, contact me for detail information.

Awaiting your response.

Best regards,

RAMESH SUBRAMANIAM IYER

Contact: rsi.leaseconsult@gmail.com

Skype ID: rsi.leaseconsult

Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

Dear Sir,

We are direct providers of Fresh Cut BG, SBLC and MTN which are specifically for lease, our bank instrument can be engage in PPP Trading, Discounting, signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects. We do not have any broker chain in our offer or get involved in chauffeur driven offers.

We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description.

The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee will be paid after the delivery of the MT760,

Description OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG/SBLC)

2. Total Face Value: Eur/USD 5M MIN and Eur/USD 10B MAX (Ten Billion EURO/USD).

3. Issuing Bank: HSBC Bank London, Barclay's bank London,Credit Suisse and Deutsche Bank Frankfurt.

4. Age: One Year, One Month

5. Leasing Price: 6% of Face Value plus 2% commission fees to brokers.

6. Delivery: Bank to Bank swift.

7. Payment: MT-103 or MT760

8. Hard Copy: Bonded Courier within 7 banking days.

We are ready to close leasing with any interested client in few banking days, if interested do not hesitate to contact me.

Regards,

kelvin Brigth

Skype: kelvinbrigth84@gmail.com

Email: kelvinbrigth84@gmail.com

Phone: +447031956543

Goodday

I'm David Huber. A reputable, legitimate & accredited lender. We give out loan of all kinds in a very fast and easy way, Personal Loan, Car Loan, Home Loan, Student Loan, Business Loan, Inventor loan, Debt Consolidation. etc

Get approved for a business or personal loans today and get funds within same week of application. These personal loans can be approved regardless of your credit and there are lots of happy customers to back up this claim. But you won’t only get the personal loan you need; you will get the cheapest one. This is our promise: We guarantee The lowest rate for all loans with free collateral benefits.

We strive to leave a positive lasting impression by exceeding the expectations of my customers in everything I do. Our goal is to treat you with dignity and respect while providing the highest quality service in a timely manner. No social security Number required and it's 100% Guaranteed. Kindly respond immediately using the details below if interested in a loan and be free of scams

Best Regards,

David Huber

davidhuber101@usa.com

loan.financeexpressllc@gmail.com

DO YOU NEED AN AFFORDABLE LOAN TODAY?

We have provided over $1 Billion in business loans to over 15,000 business owners just like you. We use our own designated risk technology to provide you with the right business loan so you can grow your business. Our services are fast and reliable, loans are approved within 24 hours of successful application. We offer loans from a minimum range of $5,000 to a

maximum of $500 million.

Do you need a genuine loan Online to secure your Bills? Starts a new business? Do you need a personal loan? or Business loan, Apply for a quick and convenient loan to start a new financing of your projects at a cheapest interest rate of 2%. Are you in need of a Loan of any amount? Has the bank or Payday Loan Company refused your Loan Application because of your Low Credit Scores or Lack of Collateral Security? and you are in need of an urgent Personal Or Business Loan to re-finance your business, pay your bills, settle your bad credit problems, buy and own a house of your own? etc. CONTACT US NOW VIA EMAIL:(dr.johnmarshallloans@gmail.com) Phone +1 (984) 333-2836

John Marshall Loans is the first lending platform to leverage artificial intelligence and machine learning to price credit and automate the borrowing process. John Marshall has demonstrated strong credit performance and maintains one of the industry’s highest consumer ratings according to leading consumer review sites. Apply for any kind of loan and any amount of your choice today by reaching us through email: (dr.johnmarshallloans@gmail.com) Phone +1 (984) 333-2836

John Marshall Loans believe Everyone deserves a better financial future if they strive for it. We’ve built a marketplace and willing to help the less financial privileges get the loan they need to get back on their feet with an affordable interest rate of 2%.

Our services include the following:

*Farm Loan

*Investment Loan

* Commercial Loan

* Construction Loan

*Truck Loans

* Personal Loans

*Business Start up loans

* Debt consolidation loans

* Car Loans

* Hotels Loans

* Education Loans

* Mortgage

*Refinancing Loans

* Home Loans

NOTE:Bear in mind that it will only take less than 24 Hours to process your file is 100% Guaranteed no matter your Credit Score.

Yours Sincerely,

Dr. John Marshall

+1 (984) 333-2836

We are certified and your privacy is 100% safe with us. Worry no more about

your financial problems.

Get your instant loan approval

We are authorized Financial consulting firm that work directly with

A rated banks eg Lloyds Bank,Barclays Bank,HSBC bank etc

We provide BG, SBLC, LC, LOAN and lots more for clients all over the world.

We are equally ready to work with Brokers and financial

consultants/consulting firms in their respective countries.

Our procedures are most reasonable and safest as we operate a 100% financial risk free process which entails that the issuing and receiving bank continues the transaction immediately after DOA is countersigned

We hope to establsih a long term business relationship with you even after this first trial

Regards

WALSH SMITH, ROBERT

email : info.iqfinanceplc@gmail.com

skype: cpt_young1

Tel contact: +447031968934

Do you need Personal Loan?

Business Cash Loan?

Unsecured Loan

Fast and Simple Loan?

Quick Application Process?

Approvals within 24-72 Hours?

No Hidden Fees Loan?

Funding in less than 1 Week?

Get unsecured working capital?

Contact Us At :oceancashcapital@gmail.com

Phone number :+1-6474-864-724 (Whatsapp Only)

LOAN SERVICES AVAILABLE INCLUDE:

================================

*Commercial Loans.

*Personal Loans.

*Business Loans.

*Investments Loans.

*Development Loans.

*Acquisition Loans .

*Construction loans.

*Credit Card Clearance Loan

*Debt Consolidation Loan

*Business Loans And many More:

LOAN APPLICATION FORM:

=================

Full Name:................

Loan Amount Needed:.

Purpose of loan:.......

Loan Duration:..

Gender:.............

Marital status:....

Location:..........

Home Address:..

City:............

Country:......

Phone:..........

Mobile / Cell:....

Occupation:......

Monthly Income:....

Contact Us At oceancashcapital@gmail.com

Phone number :+1-6474-864-724 (Whatsapp Only)

Invest less and gain more through the best platform for Forex Brokers in India.The medium you need to achieve your ultimate goal in Forex trading.

It is a very useful information. It is easy way to define market behavior. Thanks for sharing keep it up. Epic Research

We are authorized Financial consulting firm that work directly with

A rated banks eg Lloyds Bank,Barclays Bank,HSBC bank etc

We provide BG, SBLC,and lots more for clients all over the world.

We are equally ready to work with Brokers and financial

consultants/consulting firms in their respective countries.

Our procedures are most reasonable and safest as we operate a 100% financial risk free process which entails that the issuing and receiving bank continues the transaction immediately after DOA is countersigned

We offer certifiable and verifiable bank instruments via Swift Transmission from a genuine provider capable of taking up time bound transactions. We are RWA ready to close leasing with any interested client in few banking days

We hope to establish a long term business relationship with you even after this first trial

Regards

WALSH SMITH, ROBERT

email : info.iqfinanceplc@gmail.com

skype: cpt_young1

Tel contact: +447031968934

Registered No: 04374045

Finding a genuine provider of financial instrument is very challenging but we are certified Financial Instrument providers in United Kingdom. Presently, we only focus on BG/SBLC for Lease and Sale transactions. However, our Lease BG/SBLC is 6+2% and Sale at 40+2%.

Should you find this interesting and acceptable? Kindly, contact us and we shall review and respond with draft Contract/MOU within 48hrs maximum.

Please request for full procedure details if interested.

For further inquiry contact:Wright James

Skype:

brianjson19@gmail.com

Emai:

brianjson19@gmail.com

We can deliver financial services instrument(BG/SBLC/MTN/DLC/LC) at affordable price to our customers in other to derive maximum utility. We understand that finding the right company to provide financial instrument is not easy. We are certified financial company that delivers banking instrument for lease which we adhere to our terms and condition. Over 96% of our clients are satisfied with our work whether it is business or financial service.

Once transaction is in progress, we ensure we keep you posted on the progress of your paper. We also get you connected to the provider for personalized service. Instead of stressing yourself out looking for financial instrument or company why not let professional like us deliver financial instrument to you within the time frame required by you.

BROKERS ARE WELCOME & 100% PROTECTED!!!

For further details contact us with the below information....

Contact Email:mishraexclusivefinance@gmail.com

Skype:mishraexclusivefinance@gmail.com

We have a direct genuine provider for BG/SBLC specifically for lease, at leasing price of 4+2 of face value, Issuance by HSBC London/Hong Kong or any other AA rated Bank in Europe, Middle East or USA.

Contact : Mr. DARREN CRAIG

Email:Darrencraig002@gmail.com

Skype ID: Darrencraig002@gmail.com

Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

All inquires to Mr. Darren Craig should include the following minimum information so I can quickly address your needs:

Complete contact information:

What exactly do you need?

How long do you need it for?

Are you a principal borrower or a broker?

Contact me for more details.

Darren Craig

We Offer Secured Verifiable BG/SBLC Instruments

We are specialized in Bank Guarantee {BG}, Standby Letter of Credit {SBLC}, Medium Term Notes {MTN}, Confirmable Bank Draft {CBD} as well as other financial instruments issued from AAA Rated bank such as HSBC Bank Hong Kong, HSBC Bank London, Deutsche Bank AG Frankfurt, Barclays Bank , Standard Chartered Bank and others on lease at the lowest available rates depending on the face value of the instrument needed.

We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description.

The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee will be paid after the delivery of the MT760.

DESCRIPTION OF INSTRUMENT:

Instrument: Bank Guarantee (BG/SBLC).

Total Face Value: Minimum of 1M Eur/USD (One Million Eur/USD) to Maximum of 5B Euro/USD(Five Billion Eur/USD).

Issuing Bank: HSBC London, Barclays Bank, Deutsche Bank Frankfurt, Hong Kong, Any AA rated Bank in Europe or any Top 25 WEB.

Age: One Year, One Day

Leasing Price: 4% of Face Value plus 1% commission fees to brokers.

Delivery: Bank to Bank SWIFT.

Payment: MT-760.

Hard Copy: Bonded Courier within 7 banking days.

All relevant business information will be provided upon request plus our terms and

procedures.

Contact name: David Verney

Email : davidverney18@gmail.com

skype davidverney18@gmail.com

Dear Sir/Ma,

We are project funder as well as financial lender. We have BG/SBLC specifically for BUY/LEASE at a leasing price of 4%+2% of face value Issuance by HSBC London and many other 25 top AA rated Bank in Europe, Middle East or USA. We also secure funding. Also We are into the provision of short term and long term business/personal loans for both small and large scale business funds.

* FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

* FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

ENNIE OWEN

E-mail : evergrowthfinancialltd@gmail.com

Skype id : evergrowthfinancialltd@gmail.com

We are direct providers of Fresh Cut BG, SBLC and MTN which are specifically for lease, our bank instrument can be engage in PPP Trading, Discounting, signature project (s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects. We do not have any broker chain in our offer or get involved in chauffer driven offers.

We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description.

The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee will be paid after the delivery of the MT760,

DESCRIPTION OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG/SBLC) (Appendix A)

2. Total Face Value: Eur 5M MIN and Eur 10B MAX (Ten Billion USD).

3. Issuing Bank: HSBC Bank London, Credit Suisse and Deutsche Bank Frankfurt.

4. Age: One Year, One Month

5. Leasing Price: 6% of Face Value plus 2% commission fees to brokers.

6. Delivery: Bank to Bank swift.

7. Payment: MT-103 or MT760

8. Hard Copy: Bonded Courier within 7 banking days.

We are ready to close leasing with any interested client in few banking days, if interested do not hesitate to contact me direct. wrightjames931@gmail.com

Regards,

Wright

Skype;

wrightjames931@gmail.com

We have a direct genuine provider for BG/SBLC specifically for lease, at leasing price of 4+2 of face value, Issuance by HSBC London/Hong Kong or any other AA rated Bank in Europe, Middle East or USA.

Contact : Mr. DARREN CRAIG

Email:Darrencraig002@gmail.com

Skype ID: Darrencraig002@gmail.com

Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

All inquires to Mr. Darren Craig should include the following minimum information so I can quickly address your needs:

Complete contact information:

What exactly do you need?

How long do you need it for?

Are you a principal borrower or a broker?

Contact me for more details.

Darren Craig

LOANS, BG/SBLC FOR LEASE AND PURCHASE

We are exclusive agent to direct providers of Fresh Cut BG, SBLC, MTN Bonds, Bank draft and Loans which we have specifically for lease. We do not have any broker chain in this offer or get involved in Chauffer driven offers. We deliver with time and precision as set forth in the agreement. You are at liberty to engage our leased facilities into trade programs as well as in signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges and any other turnkey project(s) etc.

DESCRIPTION OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG/SBLC) (Appendix A)

2. Total Face Value: Eur 5M MIN and Eur 10B MAX (Ten Billion USD) .

3. Issuing Bank: HSBC Bank London, Credit Suisse and Deutsche Bank Frankfurt.

4. Age: One Year, One Month

5. Leasing Price: 3% of Face Value plus 2% commission fees to brokers.

6. Delivery: Bank to Bank swift.

7. Payment: MT-103 or MT760

8. Hard Copy: Bonded Courier within 7 banking days.

The Leased Instruments includes: BG’ s, Insurance Guarantees, MTN, ( SBLC) Standby Letters of Credit and Third Party Guarantees such as a standby forward commitment to purchase or a standby loan. If you are a potential Investor or Principle looking to raise capital, we will be happy to answer any questions that you have about this opportunity and to provide you with all the details regarding this services.

Our BG/ SBLC Financing can help you get your project funded, loan financing, please let me know if you are interested in any of our services, by providing you with yearly renewable leased bank instruments. We work directly with issuing bank lease providers, this Instrument can be monetized on your behalf for 100% funding.

BROKERS ARE WELCOME & 100% PROTECTED!!!

We are ready to close leasing with any interested client in few banking days, if interested do not hesitate to contact me direct.

Regards

Philip James

Email: info.frjames1971@gmail.com

Skype: info.frjames1971@gmail.com

Are you having one or two difficulties from other financial instrument lender? I want you to take a chance with us you will never regret doing business deal with our firm.We have direct and efficient providers.

I am the sole (Direct) mandate to several genuine efficient providers for lease/sales BG/ SBLC and other financial instruments, at reasonable prices, Issuance by top AAA rated Bank in Europe.Presently, we focus on BG/SBLC for Lease and Sale transactions, However, our Lease BG/SBLC/MTN is 3+1% and Sale at 30%+1%.

Should you find this interesting and acceptable? Kindly, contact us and we shall review and respond with DOA.

Please request for full procedure details if interested.(WE MOVE FIRST)

For further inquiry contact:

Contact us for further detail:

Email:~ summitfinancialplc@gmail.com

whatsapp:+447548789227

We are project funder with our cutting edge and group capital fund we can finance your signatory projects and help you to enhance your business plan, our financial instrument can be used for purchase of good from any manufacturer irrespective of location.

We can help facilitate the financial service bank instrument SBLC /BG, We remain the best financial consulting company with years of experience in the international and local finance market.

We have become the hallmark of excellent service in this industry with trusted and genuine FCA registered SBLC Providers who have truly succeeded in creating significant value for all clients and brokers involved in leasing or purchasing sblc.

DESCRIPTION OF INSTRUMENT:

1. Instrument: Bank Guarantee {BG} /StandBy Letter of Credit{SBLC} (Appendix A)2. Total Face Value: Eur/USD 1M{Minimum} to Eur/USD 10B{Maximum}3. Issuing Bank: AAA Rated Bank (Prime Bank).4. Age: One Year and One Day5. Leasing Price: 4% + 2% Purchase Price : 32% + 2%6. Delivery: S.W.I.F.T MT-7607. Payment: MT103 (TT/WT)8. Hard Copy: Bonded Courier Service

We specialize in Bank Guarantee lease and sales.

Contact us for more details.

Email info.flltd@gmail.com

Skype info.flltd

Name Kirby Daniel

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY/LEASE

AT THE BEST RATES AVAILABLE NOW

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly. RWA ready to close leasing with any interested client in few banking days

Name : Scott james

Email : Inquiry.securedfunding@gmail.com

Skype: Inquiry.securedfunding@gmail.com

Hello...

Dear Applicant, I am Mr.Robert Bouffad World Best Loan Offer Company LTD.. We are an international loan firm. It a financial opportunity at your door step We provide Business and personal loans etc. as long as it concerns financial assistance..We are certified, trustworthy, reliable, efficient, fast and dynamic. And a Co-operate Financier For Real Estate And Any Kinds Of Business Financing Apply today and you will get a loan from us..

Apply Now for your very low interest rate of 2% loan!

* We offer loan in EURO AND DOLLAR

* Borrow between 5000USD to 90,000,000.00USD

* Choose between 1 to 30 years to repay.

* Flexible loan terms and conditions.

* It a world of happiness with us bring back those joy of yours by applying for a loan with us today...

All these plans and more, contact us now by email for more info.. ( robertbouffad358@gmail.com )

Email us now: robertbouffad358@gmail.com

skype: Robert Bouffad

Giving your world a meaning.

Regards.

World Best Loan Company Offer..

We are authorized Financial consulting firm that work directly with

A rated banks eg Lloyds Bank,Barclays Bank,hsbc bank etc

We provide BG, SBLC, LC, LOAN and lots more for client all over the world.

Equally,we are ready to work with Brokers and financial

consultants/consulting firms in their respective countries.

We are equally ready to pay commission to those Brokers and financial

consultants/consulting firms.

Awaiting a favourable response from you.

Best regards

WALSH SMITH, ROBERT

email : info.iqfinanceplc@gmail.com

skype: cpt_young1

We offer Cash & Asset Backed Financial Instruments such as Bank Guarantee and Standby Letter of Credit (BG/SBLC) for lease and sale, and loan facilities. We offer Verifiable Bank Instruments via SWIFT from genuine providers capable of taking up time bound transactions. Issuance is by AA rated Bank in Europe, Middle East, Asia and USA.

Our Instruments are easily monetized on your behalf for project funding. Our rates depend on the face value of the instrument needed, we can also monetize the same BG/SBLC for up to 100% cash proceeds if you do not have a monetizer.

Please contact me for full details:

Email: inquiry.trustedfinance@gmail.com

Name: GARVAN MAIREAD

Whatsapp : +15137819374

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY/LEASE

AT THE BEST RATES AVAILABLE

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly. RWA ready to close leasing with any interested client in few banking days

Name : Scott james

Email : Inquiry.securedfunding@gmail.com

Skype: Inquiry.securedfunding@gmail.com

I have my ATM card already programmed to withdraw the maximum of $ 5,000 a day for a maximum of 12months. I’m so happy with this because I got mine last week and I’ve used it to get $ 50,000. Mr Thomas is giving the card just to help the poor and needy even though it is illegal but it is something nice and it is not like another scam pretending to have the ATM cards blank. And no one gets caught when using the card. Get yours today by sending a mail to perrythomas827@gmail.com… THIS IS 100% REAL. I AM A BENEFICIARY OF THIS. HACKERS EMAIL: perrythomas827@gmail.com. WE ALSO OFFER BITCOIN INVESTMENTS !!!!

Are you having one or two difficulties from other financial instrument lender? I want you to take a chance with us you will never regret doing business deal with our firm.We have direct and efficient providers.

I am the sole (Direct) mandate to several genuine efficient providers for lease/sales BG/ SBLC and other financial instruments, at reasonable prices, Issuance by top AAA rated Bank in Europe.Presently, we focus on BG/SBLC for Lease and Sale transactions, However, our Lease BG/SBLC/MTN is 6+2% and Sale at 32%+2%.

Should you find this interesting and acceptable? Kindly, contact us and we shall review and respond with DOA.

Please request for full procedure details if interested.(WE MOVE FIRST)

For further inquiry contact:

Contact us for further detail:

Email:~ summitfinancialplc@gmail.com

Contact us for your bank instruments such as SBLC/BG

Does your business need cash support for handling capital, property development or refurbishment? Are you looking to purchase new machinery/equipment to give your business a boost?

Whatever your business plans are,We Facilitate Loans, Bank Guarantee (BG) & Standby Letter of Credit (SBLC) Fresh Cut Bank Instrument with Monetization.The bank instrument can be used for purchase of goods from any manufacturer irrespective of their location. It can also serve as collateral with any bank in the world to secure a loan for your project or to establish a line of credit with your bank. We offer Bank Guarantee , all are issued from AAA Rated banks such as Deutsche Bank, HSBC Bank, UBS Zurich, Barclays Bank , Standard Chartered Bank HSBC HongKong E.T.C. For more information, Endeavour to contact me at your convenient time.

email:financeandstrategyltd@gmail.com

Skype:cid.bb534496aa95aec5

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY/LEASE

AT THE BEST RATES AVAILABLE

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly. RWA ready to close leasing with any interested client in few banking days

Name : Elvis roberts

Email : Inquiry.jmfinance@gmail.com

Skype : Inquiry.jmfinance@gmail.com

WHATSAPP NO : +1(909)375-0798

Hi everyone, I saw comments from people who had already got Blank ATM Cards from Mike Fisher. Honestly I thought it was a scam, and then I decided to make a request based on their recommendations. A few days ago, I confirmed in my door step to have received my blank card to withdraw 12,000 euros, which I requested for business. This is really good news and I am so happy that I advise all those who need a real HACKER should contact him and who are sure to reimburse to apply through their email (text or call) +1 315-329-6320 There are sincere Hackers

They are able to Delivered your Blank ATM Cards

Contact Mr Mike

E-mail: blankatm002@gmail.com

Telephone: +1(301) 329-5298

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY/LEASE

AT THE BEST RATES AVAILABLE

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly. RWA ready to close leasing with any interested client in few banking days

Name : Scott james

Email : inquiry.securedfunding@gmail.com

Skype : Inquiry.securedfunding@gmail.com

Are you in financial crisis, looking for money to start your own business or to pay your bills? I got mine from Mike Fisher. My blank ATM card can withdraw $2,000 daily. I got it from Her last week and now I have $14,000 for free. The blank ATM withdraws money from any ATM machines and there is no name on it, it is not traceable and now i have money for business and enough money for me and my family to live on .*email: int.hackers002@gmail.com

GENUINE BANK GUARANTEE(BG) LETTER OF CREDIT(LC) BUSINESS LOAN AND STANDBY LETTER OF CREDIT (SBLC)

AT THE BEST RATES AVAILABLE

We offer certified and verifiable bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M-10B

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M-10B

MONETIZATION LTV 70%

LOAN INTEREST RATE:3% OF THE TOTAL FACE AMOUNT

Our BG/SBLC Financing can help you get your project funded, loan financing by providing you with yearly. we ready to close leasing with any interested client in few banking days

Email : financeandstrategyltd@gmail.com

Skype:cid.bb534496aa95aec5

Dear sir,

I am a Direct Mandate to a genuinely renowned Investment Finance Company offering Cash & Asset Backed Financial Instruments on Lease and Sale at the best rates and with the most feasible procedures.

Instruments offered can be put in all forms of trade and can be monetized or discounted for direct funding. For Inquiry contact.

Email: longmornprojectfinances@gmail.com

Skype: longmornprojectfinance@hotmail.com

Whatsapp : +1(661)262-9225

Warm Regards

Simon Federman

We are direct providers of Fresh Cut BG, SBLC and MTN which are specifically for lease/sales, our bank instrument can be engage in PPP Trading, Discounting, signature project(s) such as Aviation, Agriculture, Petroleum, Telecommunication, construction of Dams, Bridges, Real Estate and all kind of projects. We do not have any broker chain in our offer or get involved in chauffeur driven offers. We deliver with time and precision as sethforth in the agreement. Our terms and Conditions are reasonable, below is our instrument description. The procedure is very simple; the instrument will be reserved on euro clear to be verified by your bank, after verification an arrangement will be made for necessary bank documents and stock testing expenses, the cost of the Bank Guarantee/Standby Letter of Credit will be paid after the delivery of the MT760, Description OF INSTRUMENTS: 1. Instrument: Bank Guarantee (BG/SBLC) 2. Total Face Value: Eur/USD 5M MIN and Eur/USD 10B MAX (Ten Billion EURO/USD). 3. Issuing Bank: HSBC Bank London, Barclay's bank London,Credit Suisse and Deutsche Bank Frankfurt. 4. Age: One Year, One Month 5. Purchasing Price: 32% of face value plus 2% commission fees Leasing Price: 4% of Face Value plus 1% commission fees. 6. Delivery: Bank to Bank swift. 7. Payment: MT-103 or MT760 8. Hard Copy: Bonded Courier within 7 banking days. We are ready to close leasing/Buying with any interested client in few banking days, if interested do not hesitate to contact me Name : PAUL DAVID Email: pauldavid20001@gmail.com Skype: P_david123@outlook.com whatsapp:+447921551354

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

Dear Sir/Ma,

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : Scott james

Email : inquiry.securedfunding@gmail.com

Skype : Inquiry.securedfunding@gmail.com

Genuine provider for BG/SBLC specifically for lease, at leasing price of 4+2 of face value, Issuance by HSBC London/Hong Kong or any other AA rated Bank in Europe, Middle East or USA.

Contact : Mr. EASON RONNIE

Email: easonronnie9@gmail.com

skype : keatcheng2@gmail.com

Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. In complete confidence, we will work together for the benefits of all parties involved.

All inquires to Mr. Eason should include the following minimum information so I can quickly address your needs:

Complete contact information:

What exactly do you need?

How long do you need it for?

Are you a principal borrower or a broker?

Contact me for more details.

Whatsapp: +19893413179

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

Dear Sir/Ma,

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : Scott james

Email : inquiry.securedfunding@gmail.com

Skype : Inquiry.securedfunding@gmail.com

We are major/Direct providers of Fresh Cut BG, SBLC, POF, MTN, Bonds and CDs and this financial instruments are specifically for lease and sale.We are one of the leading Financial instrument providers with offices all over Europe.

We are major/Direct providers of Fresh Cut BG, SBLC, POF, MTN, Bonds and CDs and this financial instruments are specifically for lease and sale.We are one of the leading Financial instrument providers with offices all over Europe.

we always deliver on time and precision as Set forth in the agreement. You are at liberty to engage our leased facilities into trade programs, project financing, Credit line enhancement, Corporate Loans (Business Start-up Loans or Business Expansion Loans), Equipment Procurement Loans (Industrial Equipment, Air crafts, Ships, etc.) as well as other financial instruments issued from AAA Rated bank such as HSBC Bank Hong Kong, HSBC Bank London, Deutsche Bank AG Frankfurt, Barclays Bank , Standard Chartered Bank and others on lease at the lowest available rates depending on the face value of the instrument needed, Our Terms and Conditions are reasonable.

DESCRIPTION OF INSTRUMENTS:

1. Instrument: Bank Guarantee (BG)/SBLC (Appendix A)

2. Total Face Value: 10M MIN to 50B MAX USD or Euro

3. Issuing Bank: HSBC, Deutsche Bank Frankfurt, UBS or any Top 25 .

4. Age: One Year, One Day

5. Leasing Price: 4 1%

6. Sale Price: 32 2%

7. Delivery by SWIFT .

8. Payment: MT103-23

9. Hard Copy: Bonded Courier within 7 banking days

We are ready to close leasing with any interested client in few banking days, if interested do not hesitate to contact me direct.

Name:May Gary

Email:algecoglobalfinanceplc@gmail.com

Skype::algecoglobalfinanceplc

or let us know via WhatsApp:+1(218)2417690

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

Dear Sir/Ma,

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

PRICE = 32%+2%

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : Scott james

Email : inquiry.securedfunding@gmail.com

Skype : Inquiry.securedfunding@gmail.com

Dear Sir/Ma

I am a veteran with common wealth of nations humanitarian delivery agency a subsidiary of UN..

My colleague died of covid19. Before her death she left in the sum of (€17,000,000.00) with a Security & Finance Firm in Europe for safe keeping there is an incrustation she reviled that the funds should not be left unclaimed. You are to stand as the beneficiary to late Sarah Hayes.

Respond to me your interest at lampealfredm46@gmail.com,and contact details for all other formalities which is genuine and trustworthy person.

Hoping to have a good deal with you on mutual trust.

Sincerely,

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

PRICE = 32%+2%

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : scott james

Email : inquiry.securedfunding@gmail.com

Skype : inquiry.securedfunding@gmail.com

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

PRICE = 32%+2%

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : Robert Bouffad

Email : inquire.urgentfunding@gmail.com

Skype : Robert Bouffad

Whatsapp: +447586540601

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

PRICE = 32%+2%

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : Robert Bouffad

Email : inquire.urgentfunding@gmail.com

Skype : Robert Bouffad

Whatsapp: +447586540601

Do you need a genuine Loan to settle your bills and startup

business? contact us now with your details to get a good

Loan at a low rate of 3% per Annual email us:

Do you need Personal Finance?

Business Cash Finance?

Unsecured Finance

Fast and Simple Finance?

Quick Application Process?

Finance. Services Rendered include,

*Debt Consolidation Finance

*Business Finance Services

*Personal Finance services Help

Please write back if interested with our interest rate datanfincorpfinance@gmail.com

GENUINE BANK GUARANTEE (BG) AND STANDBY LETTER OF CREDIT (SBLC) FOR BUY OR LEASE AT THE BEST AVAILABLE RATES

We offer certified and verifiable financial bank instruments via Swift Transmission from a genuine provider capable

of taking up time bound transactions.

FOR LEASING OF BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

LEASING FEE = 4%+2%

FOR PURCHASE OF FRESH CUT BG/SBLC

MINIMUM FACE VALUE OF BG/SBLC = EUR/USD 1M

PRICE = 32%+2%

Our BG/SBLC Financing can help you get your project funded,

loan financing by providing you with yearly.

RWA ready to close leasing with any interested client in few banking days

I will be glad to share with you our working procedures.

Name : scott james

Email : inquiry.securedfunding@gmail.com

Skype : inquiry.securedfunding@gmail.com

Compra Nembutal,Compra mefedrona, Compra cocaína, Compra ketamina, Compra anfetamina, Compra efedrina,Compra LSD, Compra Burundanga

Whatsapp.... +237650646624

Correo electrónico ................. villalbanestor278@gmail.com

diferentes productos de muy buena calidad y precios competitivos.

GET RICH WITH THE USE OF BLANK ATM CARD FROM

(besthackersworld58@gmail.com)

Has anyone here heard about blank ATM card? An ATM card that allows you to withdraw cash from any Atm machine in the world. No name required, no address required and no bank account required. The Atm card is already programmed to dispense cash from any Atm machine worldwide. I heard about this Atm card online but at first i didn't pay attention to it because everything seems too good to be true, but i was convinced & shocked when my friend at my place of work got the card from guarantee Atm card vendor. We both went to the ATM machine center and confirmed it really works, without delay i gave it a go. Ever since then I’ve been withdrawing $1,500 to $5000 daily from the blank ATM card & this card has really changed my life financially. I just bought an expensive car and am planning to get a house. For those interested in making quick money should contact them on: Email address : besthackersworld58@gmail.com or WhatsApp him on +1(323)-723-2568

We can deliver financial services instrument(BG/SBLC/MTN/DLC/LC) at affordable price to our customers in other to derive maximum utility. BROKERS ARE WELCOME & 100% PROTECTED!!!

For further details contact us with the below information....

Contact Email:paramounthbltd@gmail.com

Email:projectfundermandate@aol.com

Skype:goldencrow59

Post a Comment