“ Capital markets are designed for the benefit of the few “

The above quote cannot be better used to describe the ongoing fraud, lies, crony capitalism and cheating in the financial markets. Ever since the collapsed of MF Global, the level of public awareness on the ‘behind the scene’, manipulation and wheeling and dealing of brokers in businesses and politics have somehow heightened.

Hypothecation

Even though people are now more aware of what’s going on in the financial industry, the question is are they doing enough to protect their assets from being ‘hypothecated’, like in the case of MF Global.

Hypothecation is the practice where a borrower pledges collateral to secure a

debt. The borrower retains ownership of the collateral, but it is "hypothetically"

controlled by the creditor in that he has the right to seize possession if the

borrower defaults. A common example occurs when a consumer enters into a

mortgage agreement, in which the consumer's house becomes collateral until

the mortgage loan is paid off.

The detailed practice and rules regulating hypothecation vary depending on

context and on the jurisdiction where it takes place. In the US, the legal right for

the creditor to take ownership of the collateral if the debtor defaults is classified

as a lien.

Re-hypothecation is a practice that occurs principally in the financial markets,

where a bank or other broker-dealer reuses the collateral pledged by its clients

as collateral for its own borrowing or in a process call Churning.

The extent of brokers hypothecation can be viewed with the following chart.

It is always in the mind that financial markets and federally backed financial institution are always safe and sound. They will have to learn that for that matter both are unsafe because they are not backed by any tangible assets such as gold and silver. They are only backed by the nothing other than trust or the faith of the investors.

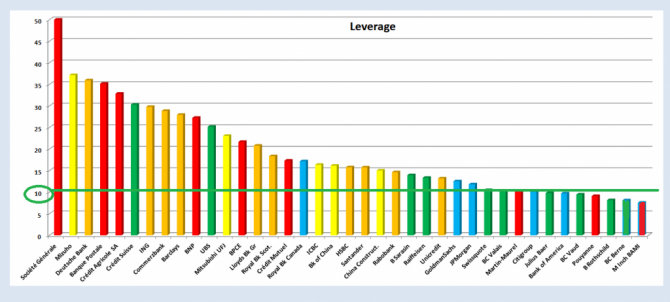

Both entities are highly leveraged and some of them until the hilt. Foe example when MF Global collapsed it is leveraged by the factor of 1 to 40, CME and LME are known to be leveraged up to 30 times, some European banks like Societe Generale , Deutsche Bank and Postale Bank are known to be leveraged up to 35 times. This can be shown in the following chart on leverage by Global Banks.

So what is the risk of leveraging up to 35 times? When there is a panic in the financial markets, bank runs will be the order of the day and this is why MF Global collapsed so fast in its final days. Customers after knowing about the irregularities that is going on, demanded refunds from their accounts and with inadequate cash to meet their demand, MF Global finally had to file for bankruptcy.

Fractional Reserve Banking

In the banking industry, the meaning of leveraging is also comparable to what we term ‘Fractional Reserve Banking’. What is Fractional Reserve Banking? In the banking industry there is a statutory requirement by the banks to adhere to and it is the percentage of deposits (normally 10%), which is also known as SDR or Statutory Deposit Ratio.

Say for example the bank receive a $100 deposit, it can lend out $90 after deducting $10 for the SDR. Then when the borrower of the $90 write a cheque to somebody who will later deposit the $90 back into the bank. When the bank receives the $90, it can then lend out 90% of it which is $81 and this process will go on until finally it will reach $1000 or ($100+$90+$81+….. = $1000). By the time it reaches $1000, the bank had already made more than 40 different loans from the original $100. So the leverage in this case is more than 1 to 10 ($100 to $1000) and can be best shown in the charts below.

| Number | Amount | Less 10% |

1

|

100

|

90

|

2

|

90

|

81

|

3

|

81

|

72.9

|

4

|

72.9

|

65.61

|

5

|

65.61

|

59.04

|

6

|

59.04

|

53.14

|

7

|

53.14

|

47.83

|

8

|

47.83

|

43.04

|

9

|

43.04

|

38.74

|

10

|

38.74

|

34.87

|

The problem with the banking industry is that sometimes it could be managed by teams of unprofessional people. The Federal Deposit Insurance Corporation in its findings, unveiled that many of the closings of financial institutions are due to mismanagement or illegal insider actions by its managers and directors.

Fractional Reserve Lending

Modern day banking has its roots which can be traced back to the 17th century goldsmith system of ‘Fractional Reserve Lending’. When people deposit their gold and silver coins in the vaults of the goldsmiths, they are given what they called the paper receipts. However over time the goldsmiths found out that only about 10-20% of the people come back to redeem their gold and silver coins at any one time.

So they begin to lend out 80-90% of the gold and silver coins out, with an interest at any time as long as they kept 10-20% of it as reserves in the vault, for those who will turn up to redeem. So eventually, they created many loans with many times the original actual amount of gold and silver. In other words they have ‘Hypothecate’ their customers gold and silver coins to the advantage of their own company.

Any differences between them?

In essence, the act of ‘HYPOTHECATION’ has somewhat been with us for the past 400 years. The question now is what is the difference between ‘Hypothecation’ by Prime Brokers, ‘FRACTIONAL RESERVE BANKING’ by modern banks and ‘FRACTIONAL RESERVE LENDING’ by 17th Century goldsmiths? The answer is ‘not much difference’ because they are engaging in the same act of hypothecating their customer’s assets.

The only difference between Fractional Reserve Banking and Hypothecation is that the Banks uses the customer’s loans to create new money each time it returned to the bank in the form of deposits. So in a way, if a bank follows the rules, their lending practice is much safer than hypothecation because if their loans get into trouble there is always a ‘Lender of Last Resort’ or the Central Bank to fall back into.

This is because the Central Bank will always function as a savior to commercial banks whenever they are in trouble and they will be ‘Bailout’ for sure. Moreover, they have what they call the deposits to be depleted before it gets to the critical level that needed a bailout.

Due to the fact that this function is being abused by most commercial banks and the end result is the creation of the many so called ‘Too Big To Fail’ banks.

How to protect ourselves?

So now the question is how can we protect ourselves from these unscrupulous operators? Brokerage abuses are far and plenty. Since the system is based on commission on sales system, brokers will not hesitate to use dirty tactics like churning (buying and selling of stocks in a customers account), high pressure sales of stocks recommended by their bosses or anything they think is of interest to you.

Unknown to many, sometimes companies coordinate with the brokers to promote their companies and often offer incentives for them to do the marketing. Brokers will encourage you and others to invest in their stocks without caring whether it fit your wants and needs. All the brokers care are their commissions and free trips if their sales quota are met.

Thomas Saler in his book ‘Lies your broker tells you’ on the subject of broker abuses, states the following,

“ People who believe in financial planning , who think their future can be secured through the valued advise of their trusted brokers are in for a rude awakening. Most brokers are not investment experts, they are super salespeople. Their goal is to sell and make commissions. To make money, aggressive brokers must snag clients whenever and wherever they can, using whatever means they have at their disposal. And those means included high risk trading, fraud, misrepresentation of investment strategies, illegal transfer of clients funds into a broker’s personal account, theft, forgery, unauthorized trading, falsification of documents and insider trading.”

Thomas Saler who is a former stockbroker and certainly knows what he is talking about.

How to avoid above problems?

- Check the integrity of your broker

- Does your broker call you every now and then?

- How is his track record in recommending stocks to you?

- Does he always pressure you to buy and use words like ‘This time is different’, ‘sure bet’, ‘cannot miss’, ‘now or never’, ‘it is going to fly’?

If

your broker have the above habits then it’s about time to dump him

because his advise is obviously not to the best of your advantage.

- Trade online and this will not only reduce the commissions you pay but also eliminate all the ill advise from your broker. If you do need the service of a full service broker for advise then it’s probably time for you to exit the market. This is because the stock market is not for everybody and to be in the market you need to educate yourself on both fundamental and technical aspect of the market. The learning curve will be slow but it is worth every penny of it.

- Check your monthly statements and make sure it tally with your own records If there is discrepancy then call up to broker to give an explanation.

- Never let your broker to be the dominant player. If you have a dishonest broker then he might be indulge in ‘Churning’ your accounts or sell your stocks and personally use the proceeds, pledge the stocks for his personal borrowing (hypothecation?) or leverage your stocks for his/her benefit.

What to do if you found irregularities?

- Call up the broker for a meeting to resolve the matter. Since brokers don’t like bad publicity, so the next best action will be to create more awareness.

- File your complain by writing or calling the exchange discipline committee.

- New York Stock Exchange, 11 Wall Street, New York, NY 10005

- American Stock Exchange, 86 Trinity Place, New York, NY 10006

- Any other local exchanges

3) The Securities and Exchange Commission

4) The Commodities Futures Trading Commission

System designed to protect Brokers

You had take action because brokers are not your friend. They win in every trade you make (buy or sell) through commissions and fees. You must understand that the Stock Market is not a Zero Sum Game as everyone perceived.

It is a Negative Sum Game due to leakages such as government tax, broker commissions and fees that are charged whenever you buy or sell shares. I mean who is going to pay for the salaries and commissions of brokers, employees of Stock Broking firms, the government and others who are either directly or indirectly linked to the industry.

Another thing is that the system is designed to protect the brokers at our expense. No matter how large the loss or the severity of the offence, the only option available to the investor is through arbitration which is supervised by the security industries. Whenever you allow an industry to police itself and if the winner of any case will be decided by fellow industry members, there are bound to be biased decisions.

Most Brokers agreement always prevents us from exercising our rights to sue. Pull your agreement with your broker and go to the section than mentions your right to sue. It states that no matter what happens you will not sue the Stock broking house or its representatives. In other words you have to play the game according to their rules whether you like it or not. Hence the stock market is not a level playing field and as I had quoted above, ‘Capital markets are designed for the benefit of the few’.

No comments:

Post a Comment