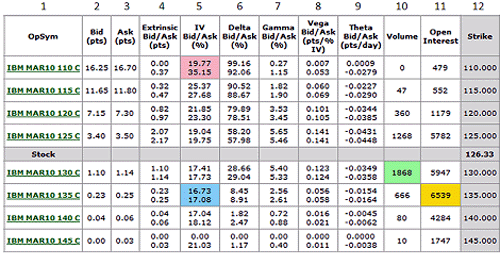

Again we shall use our earlier example for our illustration purposes and the following table shows a typical listing of an option data.

Below is a description of the above table;

1. Opsym Option Symbol

2. Bid buy price

3. Ask sell price

4. Extrinsic time premium to expiration

5. IV future volatility calculated by Black-Scholes Model

6. Delta see below

7. Gamma see below

8. Vega see below

9. Theta see below

10. Volume Volume Done

11. Open Int. Total amount of contracts that have been open but not offset

12. Strike Strike or Exercise Price

Five Factors affecting option pricing

Basically there are five factors that are affecting the options pricing and they are;

1. The current stock price and strike price

If you have purchase the below Call option, the amount of profit is determined by the amount in which the Stock price exceed the exercise price.

A normal Call option look like the following;

1 Microsoft Nov 300 Call – Premium 15

Terminology explained

a) 1

– number of contracts of 100 shares

b)

Microsoft – Underlying securities

c)

Nov – the expiry month

d)

300 – the exercise or strike price

e)

Call – type of options

f) 15 – denotes the premium paid by buyer to sellerSay if Microsoft is now trading at $320 then you will have a profit of $20 ($320-$300) x 100 shares, which is equivalent to $2000. Therefore, the Call option will be more valuable if the Stock price is increasing and less valuable if the Exercise price is increasing.

Put options behave exactly the opposite of Call options. If you have purchase the below Put option, the amount of profit is determined by the amount in which the Exercise price exceed the Stock Price. Buying Put options is like performing a ‘Short Selling’ of the underlying security. When you buy a put option at $145, to make a profit IBM share has to decline so that you can buy back at a cheaper price to cover your short position. The difference is the profit.

1 IBM Jun 145 Put – Premium 9

Terminology explained

- 1 – number of contracts of 100 shares

- IBM – Underlying securities

- Jun – the expiry month

- 145 – the exercise or strike price

- Put – type of options

- 9 – denotes the premium paid by buyer to seller

Say if the IBM share is now trading at $135 then you will have a profit of $10 ($145 - $135) x 100 shares, which is equivalent to $1000. Therefore, the Put option will be more valuable if the Stock price is decreasing and less valuable if the Exercise price is increasing because profit is equivalent to Exercise price – Stock Price.

The relationship between the Stock price and the Option price (premium), is measured by the Greek symbol Delta (Δ) . The Delta value indicates how much the Option price will move in response to a movement in the Stock price. If an option with a Delta value of 0.5, it indicates that a 1 cent movement in the Stock price will result in a ½ cent move in the Option price.

So, the higher the value of the Delta (Δ) , the closer will be the will be the movement of the Option price in relative to a change in the Stock price.

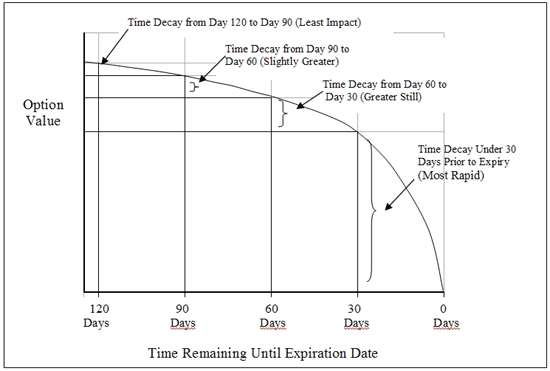

2. Time to Expiry Date (Time Decay)

As you can see from the above chart, the longer the time to expiry, the more valuable will be the option. Hence, an option with 120 days left to expiry will be more valuable than an option that has only 30 days to expiry. The holder of a 120 days to expiry option has more exercise opportunities than a holder of 30 days to maturity option.

Time decay is measured by the Greek symbol Theta (θ). The nearer to expiration date, the higher the Theta value and vice versa. The Theta value is an indication on how much a stock option’s value will lose by each day. A theta value of -0.02 indicates that the option will lose 2 cents per day.

So for the duration of a week, the option will lose a total of 14 cents because both Saturday and Sunday will also be included in the calculation even though there is no trading during those days.

The Volatility of a Stock is measured by the Standard Deviation of the return provided by the stock in a year and normally express in percentage terms. In other words the volatility of a stock price is a measure of how uncertain we are about the future movement of its price. As volatility increases the profit or loss of a particular stock also increases due to the wild swings of the stock price. How does this affect an options investor?

If a stock price increases, it will benefit the owner of a Call option while at the same time it will be detriment to the owner of a Put option.

Similarly, if a stock price decreases in its value, it will benefit the owner of a Put option and it will be detriment to the owner of a Call option.

The volatility of the Stock option can be measured with the Greek symbol Vega (υ).

If Vega is high then the stock option is very sensitive to changes to Volatility. Changes Vega value is determine by the changes in the volatility, which is expressed by every 1 percentage point. Suppose we have the following scenario;

If the volatility increases from 15% to 16% then the stock price should move up 20 cents which will then be $2.00 + 0.20 = $2.20. Vega value of options with long expiry date (>= 90 days) tends to be larger than options with shorter expiry date (<= 30 days) because the implied volatility for long expiry options tends to be lower and hence risk.

4. Interest Rates movements

Movement in interest rates affects the stock price and hence the options price as well. Whenever there is an increase in the interest rate, stock prices tend to fall. A fall in stock prices will have detrimental effect to Call options. Holders of Call options will certainly lose out because if the exercise price is lower than the stock price then they will suffer losses. Holder of Put options will stand to gain when stock price decreases because their exercise price will be higher than the stock price

Similarly a rise in the stock price will have the opposite effect.

This relationship between the sensitivity of the movement of interest rate and the stock price can be measured with the Greek symbol Rho (ρ). If an option has a Rho value of 0.15, then a 1 % increase in the interest rate will raise the price of the option by $0.15.

5. Cash Dividends, Stock Dividends and Stock Splits

When a corporation declares a dividend, it establishes a record date. This record date, will be used to record the owners of the stock on that date so that they will be entitled to the dividend. Since a normal transaction in the security industry requires 5 working days to complete, naturally the transaction need to be carried out 5 days before the record date. So, it is essential to establish that stocks had to be purchased 5 working days before the record date so as to qualify for the dividend and it is called the ‘ex-dividend date'.

Cash Dividends have the effect of reducing the price of the stock on the ex-date. The stock price will go down in relation to the amount of dividend declared. This will invariably have effect on the Option price.

For those who bought Call options, this will be bad news as the price of the option will also had to be calibrate downwards so as to reflect the changes in the stock price.

Whereas for those who bought Put options, then it will be good news to them as the decrease in the stock price will add up to their profits. Since by buying a Put option, you are hoping for the underlying stock price to go down.

Stock Dividends (or Bonus Issue) will greatly affect the terms of the options contract. Say if AAPL stock trading at $400 a share declares a Stock Dividend of 50%. What happened next is that each shareholder will receive extra 50 share for every 100 they owned. The amount of shares is also adjusted in this case from 100 shares to 150 due the extra 50 shares from the dividend. But then the price of the share will also need to be adjusted to reflect the additional new shares.

Hence the new price of the share will be $400/150, which is $266.67. This exercise, can be shown by the following.

1 AAPL Jan 400 Call before

Time decay is measured by the Greek symbol Theta (θ). The nearer to expiration date, the higher the Theta value and vice versa. The Theta value is an indication on how much a stock option’s value will lose by each day. A theta value of -0.02 indicates that the option will lose 2 cents per day.

So for the duration of a week, the option will lose a total of 14 cents because both Saturday and Sunday will also be included in the calculation even though there is no trading during those days.

3. Volatility of the Stock Price

The Volatility of a Stock is measured by the Standard Deviation of the return provided by the stock in a year and normally express in percentage terms. In other words the volatility of a stock price is a measure of how uncertain we are about the future movement of its price. As volatility increases the profit or loss of a particular stock also increases due to the wild swings of the stock price. How does this affect an options investor?

If a stock price increases, it will benefit the owner of a Call option while at the same time it will be detriment to the owner of a Put option.

Similarly, if a stock price decreases in its value, it will benefit the owner of a Put option and it will be detriment to the owner of a Call option.

The volatility of the Stock option can be measured with the Greek symbol Vega (υ).

If Vega is high then the stock option is very sensitive to changes to Volatility. Changes Vega value is determine by the changes in the volatility, which is expressed by every 1 percentage point. Suppose we have the following scenario;

- Vega value of 0.20

- Stock price at 2.00

- Volatility is at 15%

If the volatility increases from 15% to 16% then the stock price should move up 20 cents which will then be $2.00 + 0.20 = $2.20. Vega value of options with long expiry date (>= 90 days) tends to be larger than options with shorter expiry date (<= 30 days) because the implied volatility for long expiry options tends to be lower and hence risk.

4. Interest Rates movements

Movement in interest rates affects the stock price and hence the options price as well. Whenever there is an increase in the interest rate, stock prices tend to fall. A fall in stock prices will have detrimental effect to Call options. Holders of Call options will certainly lose out because if the exercise price is lower than the stock price then they will suffer losses. Holder of Put options will stand to gain when stock price decreases because their exercise price will be higher than the stock price

Similarly a rise in the stock price will have the opposite effect.

This relationship between the sensitivity of the movement of interest rate and the stock price can be measured with the Greek symbol Rho (ρ). If an option has a Rho value of 0.15, then a 1 % increase in the interest rate will raise the price of the option by $0.15.

5. Cash Dividends, Stock Dividends and Stock Splits

When a corporation declares a dividend, it establishes a record date. This record date, will be used to record the owners of the stock on that date so that they will be entitled to the dividend. Since a normal transaction in the security industry requires 5 working days to complete, naturally the transaction need to be carried out 5 days before the record date. So, it is essential to establish that stocks had to be purchased 5 working days before the record date so as to qualify for the dividend and it is called the ‘ex-dividend date'.

Cash Dividends have the effect of reducing the price of the stock on the ex-date. The stock price will go down in relation to the amount of dividend declared. This will invariably have effect on the Option price.

For those who bought Call options, this will be bad news as the price of the option will also had to be calibrate downwards so as to reflect the changes in the stock price.

Whereas for those who bought Put options, then it will be good news to them as the decrease in the stock price will add up to their profits. Since by buying a Put option, you are hoping for the underlying stock price to go down.

Stock Dividends (or Bonus Issue) will greatly affect the terms of the options contract. Say if AAPL stock trading at $400 a share declares a Stock Dividend of 50%. What happened next is that each shareholder will receive extra 50 share for every 100 they owned. The amount of shares is also adjusted in this case from 100 shares to 150 due the extra 50 shares from the dividend. But then the price of the share will also need to be adjusted to reflect the additional new shares.

Hence the new price of the share will be $400/150, which is $266.67. This exercise, can be shown by the following.

1 AAPL Jan 400 Call before

1.5 AAPL Jan 266.75 Call after

The .67 will be rounded to the nearest which is .75

Stock Splits will also works the same, with adjustment to the number of Shares and its price.

P/s : In Part 3, we will be addressing the issue on Options Trading Strategies

The .67 will be rounded to the nearest which is .75

Stock Splits will also works the same, with adjustment to the number of Shares and its price.

P/s : In Part 3, we will be addressing the issue on Options Trading Strategies

3 comments:

7 steps to health & the big diabetes lie is an excellent program, which is especially designed for the diabetes people who are all suffering in a long run in diabetes & 7 steps to health And The Big Diabetes Lie helps how to control your blood sugar level. 7 steps to health And The Big Diabetes Lie is a total natural home course which doesn’t require medication otherwise expensive equipment. Following properly tips and techniques included in 7 steps to health And The Big Diabetes Lie program will give you an important opportunity to be healthy pro the relax of your life. 7 steps to health And The Big Diabetes Lie program show Product Reviews some top secret on how to enhance the insulin level through natural methods, healthy meals & simple exercises.

Get the latest FOX technology news today: breaking news and analysis on computing, the web, blogs, games, gadgets, social media, broadband and more.

View entertainment news and videos for the latest movie, music, TV and celebrity headlines on entertainment news for today

Post a Comment