- Savings must be liquid or easily convertible to cash

Buying a piece of land does not qualify as savings, because it will take months to sell and convert it to cash. Similarly, by buying a house does not qualify it as savings, because due to the time lag or illiquid nature of the investment, it is either too long or difficult to get buyers before the sale can be to converted to cash. Also, by buying a house is also not safe as can be seen by the sub-prime crisis in the U.S. This will inevitably, lead us to conclude than an investment can only be considered safe when you are able to ‘get back the return OF your money instead of the return ON your money’.

- Savings had to be relatively safe

Investing in the commodities or futures market cannot be considered savings because it is too risky and your savings can be wipe out. Similarly, investing in the stock market cannot be considered as savings because it carries considerable amount of risk if you don’t have a plan.

Due to the high cost of living and the amount of materials goods that is available out there, it is now very difficult to save any money. After deducting our household expenses, monthly mortgages, credit cards payments, phone and utility bills, insurance and et al, we will be lucky to be able to scrape through without digging into our savings.

Another problem is instead of saving, most people spent most of their money on things that they can’t afford on credit cards and also purchase things that they don’t need. This is one of the reasons for the current credit crunch that is facing most countries around the world.

Different Savings Plan

A lot of people have the wrong misconception that savings cannot make you rich. But in reality it can make you rich and I will show you with the following tables.

Assumption : Salary and interest rates are fixed throughout the period

Table 1 : Savings of 5 % of Annual Income and 10 % return

| Salary | Monthly Savings | Value in 10 years | Value in 20 years | Value in 30 years |

20,000

|

83.33

|

17,069.79

|

63,278.21

|

188,366.46

|

30,000

|

125

|

25,605.62

|

94,921.11

|

282,560.98

|

40,000

|

166.67

|

34,140.49

|

126,560.20

|

376,744.21

|

50,000

|

208.33

|

42,675.35

|

158,199.30

|

470,927.43

|

| Source : | Mkvicka |

Table 2 : Savings of 10 % of Annual Income and 10 % return

| Salary | Monthly Savings | Value in 10 years | Value in 20 years | Value in 30 years |

20,000

|

166.66

|

34,139.46

|

126,566.41

|

376,732.91

|

30,000

|

250

|

51,211.24

|

189,842.21

|

565,121.97

|

40,000

|

333.33

|

68,280.97

|

253,120.41

|

753,488.42

|

50,000

|

416.66

|

85,350.71

|

316,398.61

|

941,854.87

|

| Source : | Mkvicka | |||

Power of Compounding

The above plan in Table 1, call for a savings of 5% of your annual income. Say if you are earning $40,000 per annum, 5% of it will be $2000. So your monthly contribution will be $2000/12, which is $166.67. This applies to the rest of the salaries. The above table shows that your savings can be generated into hugh amounts after 20 to 30 years.

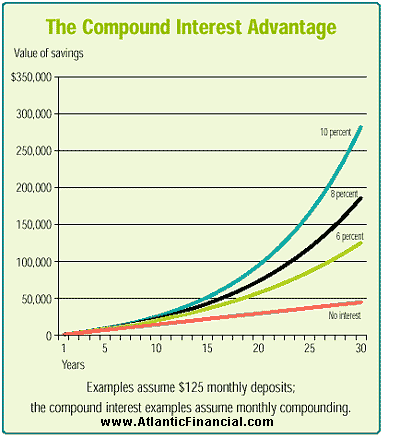

A savings of $166.67 per month can gross you the total amount of $125,560.20 and $376,744.21, respectively after a 20 and 30 years period. What happen if you double your savings from 5% to 10%?

Table 2 will show you the difference. A savings of $333.33 per month can gross you the total amount of $253,120.41 and $753,488.42, or double respectively after a 20 and 30 years period.

Remember those figures are based on a fixed income of $40,000 per annum. Due to the effect of inflation, salaries tend to go up over the years. What happen if the salary revised to $60,000 after 10 years. A 10% savings of $60,000 will be $6000/12 = $500 per month and the equation will certainly be different. In the end, your nest egg will be more than 1 million dollars. Who says savings cannot make you rich?

I am sure a lot of folks will be saying this will not work because our banks only pays 3-5% interest rates. Well even on a 5% interest rate, your compounding effect will also be sizeable if you save 10% of your annual income instead of stipulated 5%.

Another issue is that interest rates of 8-10% are achievable in emerging economies although you can hardly find such returns in developed economies nowadays. For example banks in Indonesia pays about 7-9% yield on term deposits and in Australia you probably be able to get about 7-8% returns. If you invest in money markets, you might be able to add another 1-2% more on your investments.

Banks in Singapore offers what they call the Foreign Currency accounts which caters for foreign investors and account secrecy will be assured. Ever since the increased scrutiny and pressure by the authorities in America on Swiss Banks to open up their customers portfolio, they had been an upsurge of funds flowing into Singapore. In fact private equity and wealth management is big business in Singapore. A report by the labour department reports that there will be a shortage of about 3000 private equity and wealth managers in Singapore this year.So, in a way in the next few years, Singapore will be the 'Switzerland of Asia'.

That is the beauty of what we call positive compounding of interest rates, which can be shown by the chart below. Another advantage about using the above Savings Plan to achieve your retirement plan is that you can start at any age. You can start when you are 30,40 or even 50 years old, the only difference is the duration of the plan. If you are 30 years old, then probably you might choose a 20-30 years plan and alternatively if you are 50 years old then probably you will go for the 10-20 years plan (if you can last that long).

However compounding can work both ways, meaning it can be positive and negative compounding. You will be amaze what negative compounding can do to your investments or portfolio. Understanding the drawback of negative compounding will help you in your selection of either mutual fund or dividend yield stocks for your retirement portfolio.

On our next posting, we will be addressing the issue on how negative compounding will affect your portfolio and investments. Stay tuned.

No comments:

Post a Comment