A hedge fund is a private investment fund open only to institutional and high net worth private investors. Due to the Non-public involvement in this scheme, they are not under the jurisdiction of the regulators and are much left to themselves . Hedge funds are not required to register and report to the Securities and Exchange Commission and are therefore often regarded as “secretive” or “unregulated.”

A fund of funds, is actually a hedge fund that invest in other hedge funds. Its portfolio does not consist of stocks, commodities, real estates or other investment vehicles but of other hedge funds.

It is akin to the Mutual Fund of Mutual Funds whereby this Mutual Fund selects and invests in mutual funds that outperforms.

The analysis below is based on the following assumptions.

- The bench mark is S&P with a growth averages 10% per annum

- Some data are from TASS, a hedge fund database

Inner workings of Hedge Funds

The term “hedge” does not necessary means that hedge funds are conservative or they mainly deploy hedging techniques in their investments. In fact, hedge funds use a wide array of strategies, and sometimes are not “hedged” against the market at all.

The beauty of hedge funds is that they can employ various strategies and they can invest in much more riskier investments than mutual funds. This may include real estate, art, derivatives, commodities, new startups, even website domain names. The hedge fund manager may use leverage, short selling and arbitrage in order to produce higher returns for investors.

Hedge fund managers also employ investment tools that can greatly increase returns. Unlike mutual funds, hedge funds can use short selling, invest in derivatives, leverage their portfolios, and hold highly concentrated positions - strategies that can amplify returns greatly.

Whenever there is a crash, there will be a group that did just fine because they are betting against the trend and that is for the market to crash. It seems that the strategy they employed known as ‘Market Neutral’ will always work in any market conditions. Market neutral strategy means long on good stocks and short on bad ones.

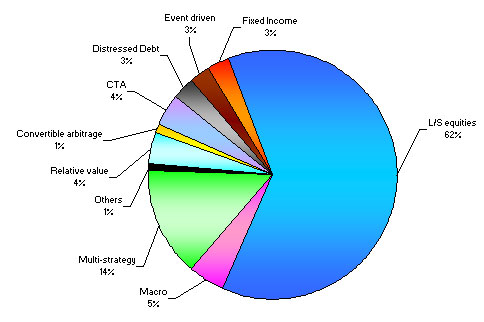

Other strategies that hedge funds use are Long/Short sector equity, Arbitrage, Emerging Markets, Merger and Acquisition arbitrage, Distress/Panic Sale Equities, Global Macro, Event Driven and many more.

When few of the many hedge funds make headlines on making a kill in the last crash, a lot of people believed that hedge funds offer better returns and everyone should be invested in hedge funds.

Law of Diminishing Returns on Funds

In reality performs much worse that most of us think. There are now more than 10,000 hedge funds managing more than $1.5 trillion. Unfortunately to invest in a hedge fund you need to have at least $1 million in liquid assets and the top notch hedge funds only concentrates on institutional investors who can easily invest $50 - $100 million.

However due to the ‘economies of scale’ in the funds, hedge funds found that the large amount of funds they hold also present a problem. The law of diminishing returns also applies to funds, the bigger your funds the less opportunity you will have. That means it will be harder for you to repeat your performance. A $1 billion fund is easier to achieve a 20% return than a $10 billion fund because a $10 billion fund needs to search for $10 billion opportunities. How many billion dollars opportunities are out there? This is what we call Diseconomies of scale in investment, whereby the bigger you are the harder for you to produce higher returns.

Hedge funds did worse that expected

Legendary hedge fund investor John Paulson was not sparred during the downturn last year. Paulson who had earlier make a name for himself, after generating returns of up to 600% by betting against mortgages in 2008 as the market crashed.Since 2010, some of Paulson's $30 billion funds have generated losses of more than 30% after waging some bad bets especially on Bank of America and Chinese company Sino Forest.

Lyxor, is Societe General’s managed account platform or Fund of Funds, had investment in about 100 hedge funds.

As of Oct. 2011, according CNNMoney, out of Lyxor’s group of 100 hedge funds only 25 had generated positive returns. Thirty funds lost more than 10% and nine funds, including Paulson's flagship Advantage fund, generated losses of more than 20%.That's worse than the S&P 500, which is only down about 8% from the start of the year.

More than 140 Asia-focused hedge funds shut down last year, due to the high market volatility, which dampened investor sentiment.

Credit Suisse said that by the end 2011, 67 per cent of global hedge funds were performing below their peak levels and 13 per cent have not earned a performance fee for four years or more.

Reasons for Bad performance

1) Too many of them.

Modern day hedge funds only started around circa 1995. During the 1990s, there are not many funds, so many of them actually make a killing in the market. Strategies that they employed like Long/Short sector specific like technology make a killing during and after the Dotcom bust. This is because they long before the crash and they short during the Crash. However, since then there are much more funds available. It is estimated that there are more than 10,000 funds are active now even though it is estimated that there are about 10% of the funds closed their doors every year. Each of them are employing almost the same strategy and hence the competition to produce higher returns has increased.

2) Non Disclosure of reporting

As we have mentioned earlier, due to the Non-public involvement in the industry, hedge funds are not required to report their performance or publish their results. Therefore, their reporting tends to suffer from data massaging and biasedness. According to a study by Professors Fung, Hsieh, Narayan and Ramadorai, the annual return of a hedge fund is about 14.4% net of fees. However, after adjusting for 2 biases namely ‘survivorship and incubation’ the percentage drop to about 10.5%. The question is what are these ‘Survivorship and Incubation’ biases?

Survivorship bias, which also occurred in Mutual Funds, is a situation where under performing or ‘dead wood’ funds are dropped from the evaluation process in the fund performance. So in other words only funds that perform favorably are included in the performance calculation.

Incubation bias is a situation where hedge funds starting new funds internally and only include funds that do well and exclude those that did badly from their performance reporting. It is similar to a large shopping center chain keeps opening new stores to boost their overall sales even though some are located just a couple of kilometers from each other. End result is cannibalizing of sales where old store sales are dropping while new stall sales are growing.

3) High cost or fees

No doubt most hedge funds have their own money invested in the funds as well and also staffed by some of the smartest fund managers around. They too are bogged down by the high cost of their remuneration. Their charges are best known as ‘two and twenty’. By this we mean that they charge 2% on their fees on assets (either they performed or not) and 20% commission on the profits they make. In order to make a 10% return on their investments, hedge funds need to garner in at least a 20% return to compensate for the fees, commissions, survivorship and incubation bias and taxes.

When you include fund of funds it is even worse. And Fund of funds, known to charge ‘one and ten’ on top of what the hedge funds make. So for a Fund of funds to produce a 10% return, the fund manager needs to generate a 25% return from his portfolio.

4) High risk undertaking

Due to their nature of non reporting, they tend to take higher risk appetite in their investment undertakings. Hedge funds returns are at best erratic. Unlike Mutual Funds, that need to report quarterly, their earnings tends be known fairly quickly. Hedge funds however are not required to report their earnings tend to take riskier ventures in the last quarter, if their 3 previous quarters performed less that expected.

| Quarters | Returns % |

| Qtr 1 2000 |

18%

|

| Qtr 2 2000 |

20%

|

| Qtr 3 2000 |

4%

|

| Qtr 4 2000 |

25%

|

| Qtr 1 2001 |

19%

|

| Qtr 2 2001 |

-10%

|

| Qtr 3 2001 |

26%

|

| Qtr 4 2001 |

25%

|

A normal hedge fund performance might look like the above, where certain quarters perform favorably well and certain quarter sucks. The variance can be from -10% to 26%. So when one of the quarters under performs, the hedge fund managers will have to take on bigger bets so as to make up for the losses. In the end you know how they end up.

Shareholders vote with their foot

Hedge fund managers are human too, so taking risk is part of their job. If they judge the market wrongly, all they need to do is to fold up and look for another job at other funds or better still just hang on to the fund and collect the 2% fees on assets in perpetuity.

So in the end, the risk is bigger for the investors than the hedge fund managers. If hedge funds consistently outperforms the benchmark, then reputable funds like Julian Robertson’s Tiger Fund, Soros’s Quantum Fund and Long Term Capital Management would not have suffer heavy losses and eventually had to fold up. A friend of mine who used to be in the hedge fund industry, told me that shareholders in hedge funds vote with their foot and not with their brains. Even though you have performed marvelously for the past years, that does not mean you will be immune to shareholders revolt. If your performance sucks this year, you will still be kicked out.

2 comments:

Great Post! Thank you such a great amount for sharing. MORE Modern Trade Reconciliation |Fixed Assets Audit | Customer Reconciliation

Thanks for sharing that valuable post. I really enjoy your post. I will be waiting for your another blog & i want more Duplicate Payment Audit | AP Vendor Helpdesk | Duplicate Invoice Audit

Post a Comment